ACF 101 102 Introductory Financial Accounting Introductory Financial

for the Securities and Exchange")

and internally (previous")

- Slides: 18

ACF 101 -102 Introductory Financial Accounting Introductory Financial Statement Analysis LECTURE 18

Learning Outcome Appraise financial performance and the position of an organisation through the calculation and review of a number of basic ratios and various methods of analysis.

Topics Company information Financial ratios review

Locate and use sources of information about company performance….

Financial statement analysis focuses on techniques used by analysts external to the organization (although managers use many of the same methods). These analysts rely on publicly available information that a company releases on developments such as personnel changes, dividend changes, issuance or retirement of debt, acquisition or sale of assets or business units, new products, new orders, changes in production plans, and financial results

A major source of such information is the annual report, which usually contains the following: a. Income statement b. Balance sheet c. Statement of cash flows d. Statement of stockholders' equity

e. Footnotes to the financial statements f. A summary of accounting principles used g. Management's discussion and analysis of the financial results

h. The auditor's report i. Comparative financial data for a series of years j. Narrative information about the company k. Management’s report on its responsibility for the financial statements

Companies also prepare reports (10 -K and 10 -Q) for the Securities and Exchange Commission. Both annual reports and SEC reports are issued well after the events being reported have occurred. More timely information is often available from company press releases and articles in the business press.

Services such as Value Line, Standard and Poor’s, and Moody's Investors Services also can provide information. Stockbrokers prepare company analyses for their clients, and private investment services and newsletters supply information to their subscribers. They may ask for a set of projected financial statements or other estimates of predicted results called pro forma statements.

Objectives of Financial Statement Analysis Investors and creditors use financial statement analysis to predict the amount of expected returns and assess the risks associated with those returns.

Because creditors generally have specific fixed amounts to be received and have the first claim on assets, they are most concerned with assessing the following: a. Short-term liquidity—an organization's ability to meet current payments as they become due b. Long-term solvency—the ability to generate enough cash to repay long-term debts as they mature c. Profitability

Equity investors are more concerned with the following: a. Profitability b. Dividends c. Future security prices

Financial statement analysis is useful because past performance is often a good indicator of future performance, and current position is the base on which future performance must be built.

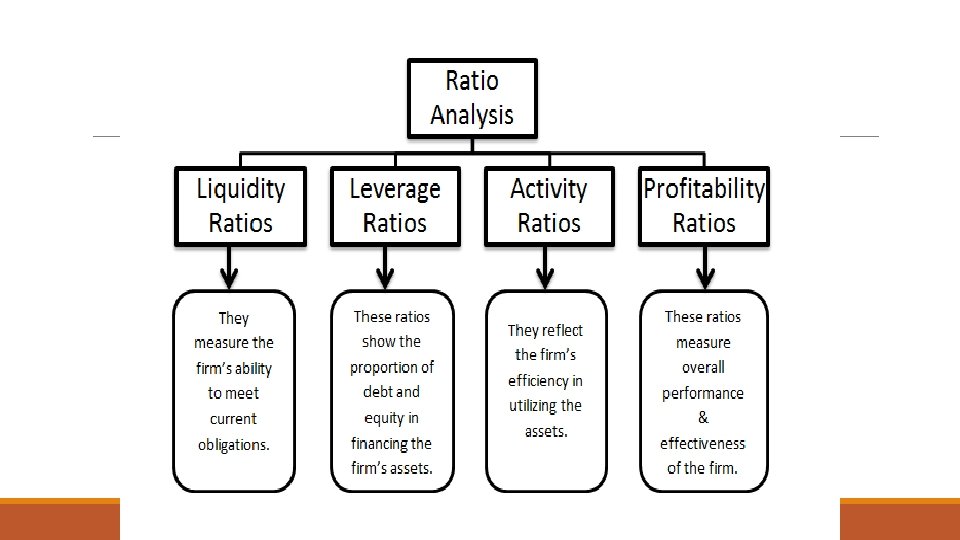

Ratios: Calculate ratios to reflect: profitability, liquidity, efficiency, gearing, investment;

Ratios: Comparison of these ratios both externally (other companies, industry standards) and internally (previous periods); interpretation of results