Secondary Planning for CRTs A presentation for Omaha

• Term")

How do we measure charitable optimization? 2) If a charitable client")

997 -4717 Email: David. Murray@Sterling-Foundations. com Fax: (800) 878 -")

- Slides: 27

Secondary Planning for CRTs A presentation for Omaha Estate Planning Council Tuesday February 16 th 2016 Presented by: Dave Murray, Managing Director, Sterling Foundation Management Evan Unzelman, President, Sterling Foundation Management

What’s New? • Secondary Planning for CRTs • Charitable Optimization (sneak peak) • Term NIMCRUTs with LP/LLC Structure ü Sterling Research Report #1510

Sterling Foundation Management • Longest serving national foundation administrator in the U. S. • Non-competitive ü Don’t provide tax, legal or financial advice ü Don’t manage or custody assets ü Support legal, financial, and tax advisors • Charitable consulting • Secondary planning for CRTs

Charitable Remainder Trusts – the Pros • Powerful tax-planning vehicles ü ü Defers capital gain Generates an up-front income tax deduction Diversifies a concentrated position Creates an income stream

Charitable Remainder Trusts – the Cons • Irrevocable • Usually span decades of clients’ lives • Combination can lead to a misalignment between client’s situation and the CRT

Options Available • Gift income interest ü Gives the entire trust to charity today • Terminate CRT ü Less common because of sale option • Sell CRT Income Interest* ü Maximizes present value of income stream to client • CRT Rollover* ü Enables client to make strategic changes regarding CRT

The Importance of CRT Reviews • CRT income interests are capital assets ü Rev. Rul. 72 -243, 1972 -1 C. B. 233 ü PLRs (e. g. , PLR 2007390041) • Yet they are rarely reviewed like other capital assets ü Clients left in the dark (“my CRT is a lifetime lockup”) • Goal of review ü Ensure client is aware of available options ü Assess client’s fit with CRT

CRT Income Interest Sale • Client receives more money than keeping CRT • Client receives more money than terminating CRT • 14 years, hundreds of transactions ü Sale has gone mainstream

Why Sell? • Change in personal circumstance • Divorce • Death of spouse • Change in financial situation • Need for liquidity • Trust not meeting expectations ü NIMCRUT

Composite Example After-Tax Proceeds No Action 1 Terminate 2 Sell Interest 3 $ 804, 183 $ 696, 850 $ 920, 000 • Financial benefit of sale ü vs. No Action: $115, 817 or 14% ü vs. Terminate: $223, 150 or 32% Does not include trustee, administration or similar fees. Prepared using advisor/client assumptions. Does not include fees associated with termination. Calculated via charitableplanning. com. 3 Includes all associated fees. 1 2

CRT Rollover • Aligns CRT with client’s current situation ü Named Beneficiaries ü New Spouse, Children ü Type of CRT • SCRUT to NIMCRUT ü Income deferral ü Build wealth tax-free for children/younger spouses • NIMCRUT to SCRUT ü Frustration with NIMCRUT ü Larger and more reliable income stream • Client also garners immediate income tax deduction

Case Study: SCRUT to NIMCRUT/Add Children • Situation ü 63 -year-old widow; surviving beneficiary of 5% SCRUT ü Didn’t need income; tax-adverse ü Focus is transferring maximum wealth to daughters • Solution ü Roll to NIMCRUT, structured for deferral • • • Mom defers income during remaining lifetime Trust goes tax-free for 19 years (mom’s life expectancy) At mom’s death, daughters collect income for their remaining lifetimes

Case Study: SCRUT to NIMCRUT/Add Children

Case Study: SCRUT to SCRUT/Add Children • Situation ü Husband wife; 72 - and 71 -year-old ü Joint income beneficiaries of Standard CRUT ü Looking to benefit two sons during clients’ lifetimes • Solution ü Roll to new Standard CRUT • • • Two sons are immediate income beneficiaries 20 -year term Max payout (~15%)

Case Study: SCRUT to SCRUT/Add Children

Case Study: NIMCRUT to SCRUT/Add Spouse • Situation ü 73 -year-old male ü Sole surviving income beneficiary of 7% NIMCRUT ü Remarried, younger spouse • Solution ü Roll to SCRUT • Creates reliable income stream ü Add wife as contingent income beneficiary • Creates income stream for younger spouse

Case Study: NIMCRUT to SCRUT/Add Spouse

Many Possibilities

What is Charitable Optimization? • Creating the highest after-tax net worth outcome for the client, • Using charitable tools, • Given the client’s attitude toward charitable giving, • Both during life and upon death, • And given the client’s assets and investments.

Research Project 1) How do we measure charitable optimization? 2) If a charitable client is not charitably optimized, what can be done? 3) What savings can be garnered by doing it?

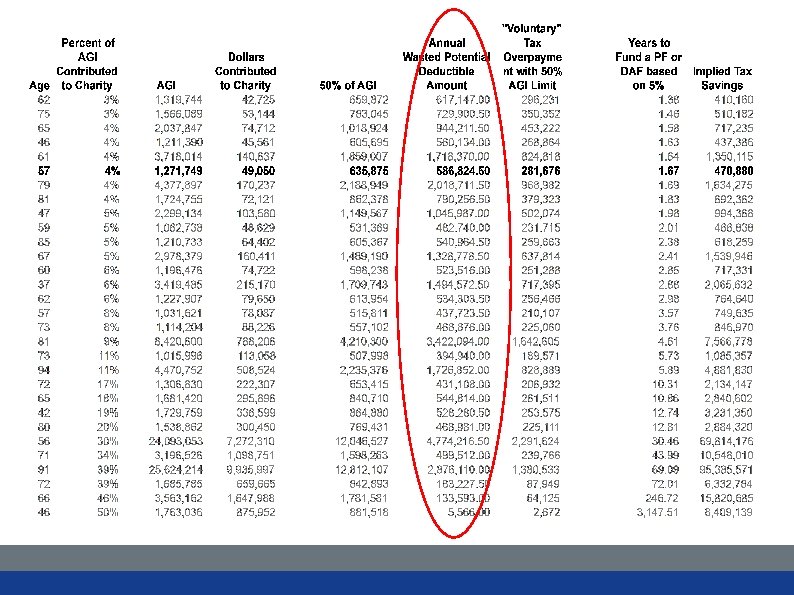

What is Charitable Optimization? 60% gave < 2% of AGI 40% gave 3% to 50%

The 40% • May be missing opportunity to optimize • Bring forward deductions on charitable contributions they’ll make anyway • Could use DAF or Private Foundation • Average benefit to client in our sample: $493, 000

Sterling Research Report #1510 • General theme ü 20 -year term NIMCRUT funded with interest in LP/LLC ü Goals: tax deferral, tax deduction, diversification • Today ü Many are approaching the end of their term ü Some have not performed as expected • Sterling’s conclusion (available at booth) ü Problem not in the design, but in the failure of markets to perform as expected

Getting to know Sterling • Read our bestselling book ü Free copies for lunch attendees • Read our articles ü Available by request • Visit our website ü www. Sterling. Foundations. com

Contact Information Direct: (703) 997 -4717 Email: David. Murray@Sterling-Foundations. com Fax: (800) 878 - 8147 Direct: (703) 793 -9265 Email: Evan. Unzelman@Sterling-Foundations. com Fax: (800) 878 - 8147

Disclaimer Sterling Foundation Management, LLC does not provide tax, legal, investment or insurance advice, and nothing in the preceding presentation should be construed as such. Any information or analysis provided is believed to be accurate but is not guaranteed or warranted. For more information, please contact: Sterling Foundation Management, LLC 12030 Sunrise Valley Dr. Suite 450 Reston, VA 20191 (703) 437 -9720 (703) 935 -4883