SALES TAX 101 THE PUZZLE YOU CANT FIGURE

$10. 00 $11. 00 $15. 00 •")

Athleticequipment and uniforms Automotive Bandequipment,")

- Slides: 31

SALES TAX 101: THE PUZZLE YOU CAN’T FIGURE OUT LET’S FIND THE ANSWER

REMEMBER…YOU ARE ALWAYS WORKING WITH OTHER AGENCIES • Comptroller of Public Accounts • Texas Secretary of State • Internal Revenue Service

DON’T PAY ‘STUPID TAX’!! Money paid by your organization simply because you “forgot” to fill out a form, send in a document or meet the deadline!!

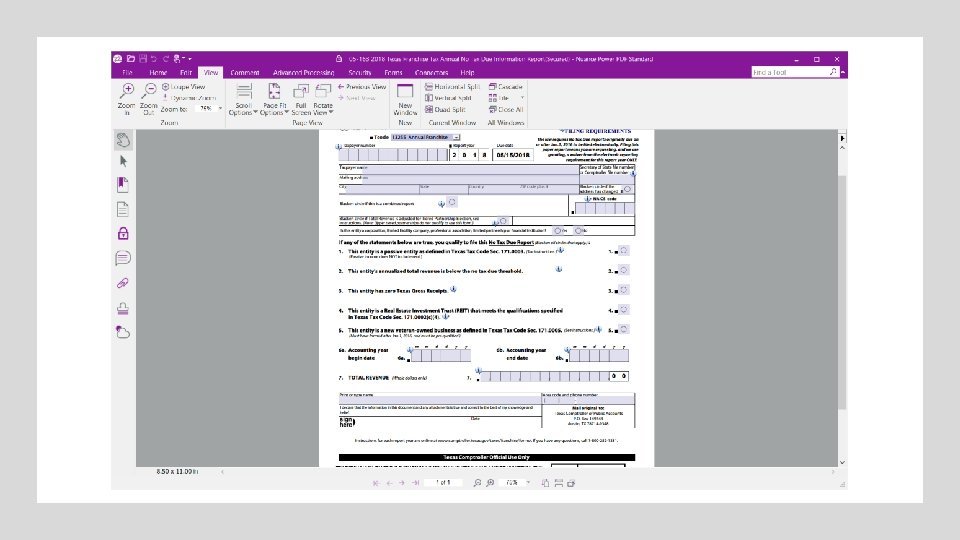

FRANCHISE TAX REPORTS • Levied annually by the state comptroller on all taxable entities doing business in the state. Each business in Texas must file an Annual Franchise Tax Report by May 15 th each year. • TX Corps, PCs, LLCs, PLLCs, and LLPs domestic and foreign: pay 1% of gross receipts over $1, 000. 00. (whose making that? ? )

FAILURE TO FILE THE FRANCHISE TAX REPORT BY MAY 15 TH WILL RESULT IN…. STUPID TAX!! $50. 00 LATE FEE

AP 204 Application for Exemption-Tells the OR…. LET’S NOT FILL IT OUT AT ALL? ? ? Comptroller’s office that you are a non-profit organization and are exempt from completing this form. Must submit AP 204 and your IRS Determination Letter Verify with the Comptroller that they have received the information

SALES TAX

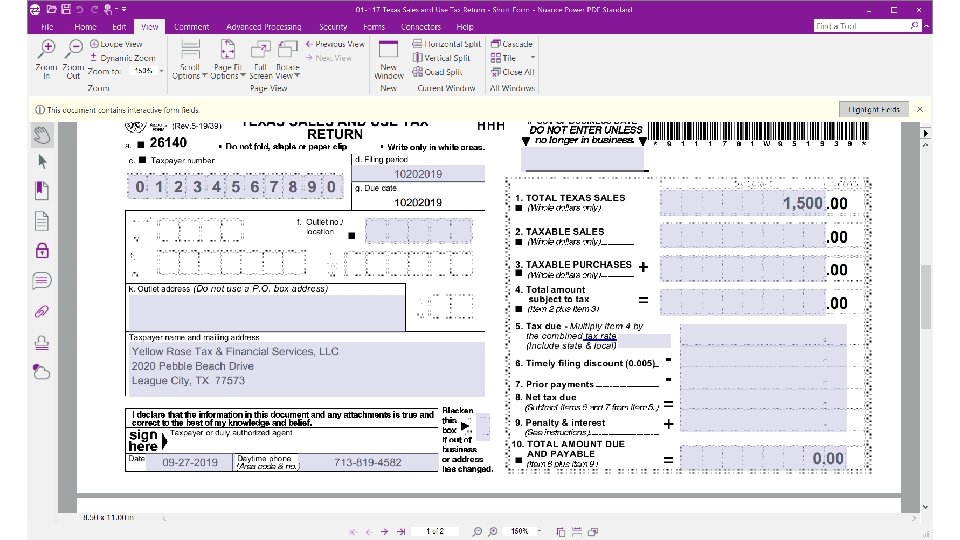

SALES TAX PERMIT You must obtain a Texas sales and use tax permit if you are engaged in business in Texas or you sell taxable services in Texas This is an eleven digit number (this is not your EIN) It will take approx. 2 -4 weeks to receive your permit once the Comptroller has received your signed application

SOME BASIC SALES TAX INFO: You may not necessarily ‘owe’ sales tax, but you MUST file a sales tax report. This is simply a ZERO TAX DUE REPORT. The Comptroller will automatically assign you as a ‘quarterly’ filer. However, request to be an ‘annual’ filer. This is done only once a year in January. You have TWO tax free days!! When calculating this, you must notate this in your meeting minutes.

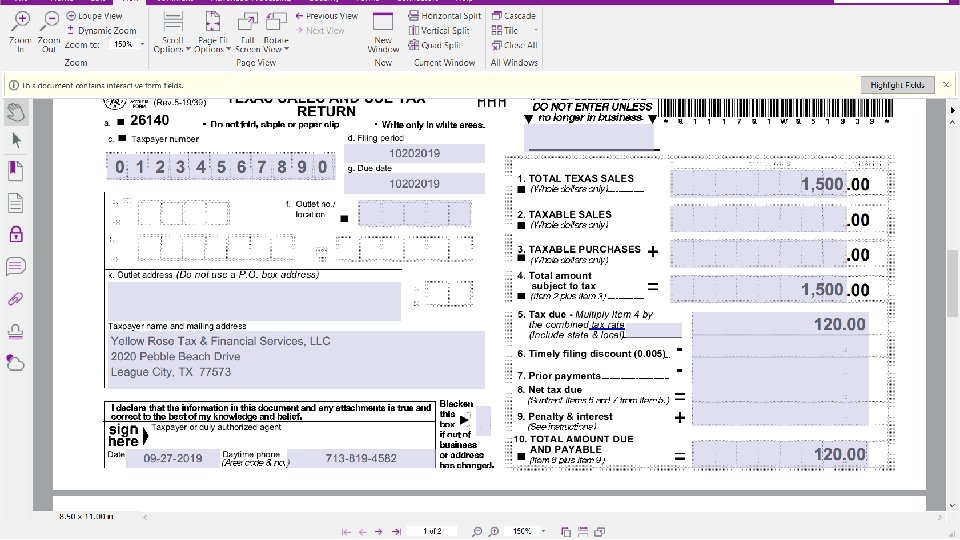

T-SHIRT FUNDRAISER (PURCHASED FROM VENDOR $10. 00) $10. 00 $11. 00 $15. 00 • At cost for the parents and the kids at $10. 00 • Increase price to take into consideration the tax that will need to be paid (8%)$11. 00 • Increase price as a ‘true fundraiser’ to include taxes and make money for organization. $15. 00 $10. 00 $11. 00 $15. 00

You can file manually: through the mail NOW YOU ARE READY TO FILE YOUR SALES TAX REPORT You can set up a Web. File account and file on-line: this is much easier. However, there a few things you will need to have ‘in hand’ to Web. File. RT number Financial information Note (to file franchise tax by Web. File, you will need an ‘XT’ number)

You should receive a ‘reminder’ to file your sales RT NUMBER tax in the mail. The RT number is in the upper left -hand corner

WEBFILE Pay your file/pay taxes File franchise tax report Request tax clearance letter Request duplicate Permit Review previous payments Update user ID

TAXABLE VS NON-TAXABLE ITEMS This can be very confusing especially when it comes to food and catalog sales, so we will see if we can break it down!!

TAXABLE Agenda books Agricultural sales Artistic (CDs, tapes, videos) Athleticequipment and uniforms Automotive Bandequipment, supplies, patches, badges, uniforms Booksworkbooks, vocabulary, library Brochure items Calculators Calendars Candles

TAXABLE Car-painting, , pin striping Decals Flowers-roses, carnations, arrangements Clothingschool, club, class Directoriesstudent, faculty Computersupplies, mouse pads Cosmetology products sold to customers Cups-glass, plastic, paper Draftingsupplies Family and Consumer Sciencesupplies Fees-copies, printing, laminating

TAXABLE Greeting cards Locks-sales and rentals Musical supplies, recorders, reeds Handicafts Horticulture items Hygiene supplies ID cards-when they are sold to the entire student body Lumber Magazinessubscriptions less than 6 months Magazines when sold individually Merchandise, tangible personal property

TAXABLE Parts-career & tech Plants-holiday greenery and poinsettias Rings and other school jewelry Parts-upholstery Printing feecomputer PE-uniforms, supplies Rental-equipment of any kind Pennants Pictures-school, group (if school is the seller) Rentals-towels Repairs to tangible personal property (i. e. computer, house remodeling)

TAXABLE Rummage and garage sales Science-science kits, boards, supplies Safety supplies School publication – athletic programs, posters, brochures School store-all items (except food) Spirit items Stadium seats Stationery, note pads, etc. produce in the classroom or vocational class Supplies-any sold to students Transcripts Uniforms-any type to include PE, dance team, drill team, cheer, athletic and club shirts

TAXABLE Vending-Pencils an other non edible supplies when the school services the machince Wood Yard signs Woodworking craftsentire sale to include parts and labor

Admission-athletics, dance performances, drama and musical performances Admission-summer camps, clinics, workshops Admissions-banquet fees, prom NONTAXABLE homecoming Admission-tournament fees, academic competition fees Cosmetology services (products sold to customer are taxable) Deposits (lockers, etc) Discount Entertainment cards and books Facility rentals for school groups

Food items sold during fundraisers, including at a PTA/PTO carnival Labor-automotive, upholstery classes (parts are taxable) NONTAXABLE Magazine subscriptions greater than six months Parking permits Services-car wash, cleaning Student Club Memberships

Catalogs or Internet sales: DON’T GET LOST IN THE “GRAY AREA” OF TAXABLE AND NON TAXABLE A seller who uses catalogs or the Internet to sell goods is treated the same as any other seller of taxable items. If you purchase merchandise through a catalog or the Internet from a seller located in Texas, you owe Texas sales tax on the purchase. If you purchase merchandise through a catalog or the Internet from a seller located outside of Texas and use the taxable item in Texas, then you owe Texas use tax on the purchase. An out-of-state mail-order company or an Internet company may hold a Texas Sales and Use tax permit and collect Texas tax. If the out-ofstate seller does not have a Texas permit or does not collect Texas use tax, the use tax is due and payable by the purchaser.

DON’T GET LOST IN THE “GRAY AREA” OF TAXABLE AND NON -TAXABLE Candy is ALWAYS TAXABLE. Let’s get an understanding of what is considered "candy". Basically, if you went to HEB, Kroger or Randalls, you will be taxed on a Snicker bar. However, you will not be taxed on popcorn in a bag. BUT. . if you purchased cracker jacks (that is the only thing I can think of in a small box) that is considered candy and you are taxed.

Nontaxable Food Products DON’T GET LOST IN THE “GRAY AREA” OF TAXABLE AND NON TAXABLE Boxes of fresh fruit Frozen cookie dough, pizza kits (pizza only--not tools) Mixes to be prepared at home (e. g. , soup, dessert, bread, dip, pancake) Meat sticks, cheese spreads & balls Bottled sauce, salsa, jelly, syrup

DON’T GET LOST IN THE “GRAY AREA” OF TAXABLE AND NON TAXABLE All volunteer nonprofits may hold taxfree food sale if: Not professionally catered Not held in a restaurant or hotel Not in competition with a retailer Food prepared by group’s members Alcoholic beverage sales are taxable

CHRISTIE V. ERICKSON Yellow Rose Tax & Financial Service, LLC Email: Christie. Erickson@yahoo. com Website: www. yellowrosetaxfinancial. com Mobile: 713 -819 -4582 Fax: 713 -583 -9664