City of Louisville SALES TAX LICENSING DIVISION SALES

Auctions Automotive vehicles (resident)")

Medical & retail marijuana")

Prosthetic devices")

:")

Boulder County (SC).")

Boulder County (SC)")

Boulder County (SC)")

Boulder County")

RTD/ CD")

Boulder County")

RTD/")

- Slides: 79

City of Louisville SALES TAX & LICENSING DIVISION SALES & USE TAX SESSION

City Taxpayer Service Office www. louisvilleco. gov Penney Bolte – Tax Manager E-mail: penneyb@louisvilleco. gov Phone: (303) 335 -4514 Fax: (303) 335 -4529 Tammy Happoldt – Tax Auditor E-mail: thappoldt@louisvilleco. gov Phone: (303) 335 -4524 Fax: (303) 335 -4523 Beth Ried – Tax Auditor E-mail: bried@louisvilleco. gov Phone: (303) 335 -4570 Fax: (303) 335 -4511

Topics üTax rates üSales and use tax definitions üTaxable and exempt transactions üTransfer of Ownership üEconomic Nexus üCharging and collecting taxes üDetermining use tax liabilities üCalculation & remittance of taxes üOnline portal üRecordkeeping üEnforcement

Tax Rates Sales tax – 3. 65% Combined sales tax rate: 2. 9% State of CO 1. 1% RTD/CD 0. 985% Boulder County 3. 65% City of Louisville 8. 635% Total Use tax – 3. 65% Combined use tax rate: 2. 9% State of CO 1. 1% RTD/CD 3. 65% City of Louisville 7. 65% Total Consumer use tax is not due to Boulder County (except for building materials and motor vehicles)

Sales Tax - Definition When tangible personal property or taxable services as defined in the Louisville Municipal Code (LMC) are sold or provided to an end user, sales tax must be collected by the seller. Who is the end user? When a transaction takes place and the purchaser has no intent of re-selling the item(s), the purchaser is considered the end user.

Sales Tax Added to the Price Retailers must add the sales tax due to the taxable purchase price and show the tax as a separate and distinct item Exceptions: liquor by the drink & vending machine sales Every retailer must remit sales tax equal to the total taxable sales for the reporting period: Taxable sales are multiplied by the City tax rate, and tax remitted, even if the retailer did not collect as much tax as is owed.

Sales Tax is Transactional Sales and use tax are transactional taxes. Each time an item is sold or transferred to a different end user, the item is subject to tax. Let’s use a refrigerator as an example. . .

Sales Tax 1. When a new refrigerator is purchased from a retailer for $1, 500, the retailer must charge the purchaser sales tax on the $1, 500.

Sales Tax 1. When a new refrigerator is purchased from a retailer for $1, 500, the retailer must charge the purchaser sales tax on the $1, 500. 2. Two years later, the purchaser sells the refrigerator to a used appliance dealer for $750. The purchase by the used appliance dealer is a wholesale purchase for resale, no tax is due.

Sales Tax 1. When a new refrigerator is purchased from a retailer for $1, 500, the retailer must charge the purchaser sales tax on the $1, 500. 2. Two years later, the purchaser sells the refrigerator to a used appliance dealer for $750. The purchase by the used appliance dealer is a wholesale purchase for resale, and no tax is due. 3. When the appliance dealer sells the refrigerator to an automotive repair shop for $1, 000, he must charge and collect sales tax on the $1, 000.

Sales Tax 1. When a new refrigerator is purchased from a retailer for $1, 500, the retailer must charge the purchaser sales tax on the $1, 500. 2. Two years later, the purchaser sells the refrigerator to a used appliance dealer for $750. The purchase by the appliance dealer is a wholesale purchase for resale, and no tax is due. 3. When the appliance dealer sells the refrigerator to an automotive repair shop for $1, 000, he must charge and collect sales tax on the $1, 000. 4. The repair shop goes out of business and all the assets of the business are put up for sale at auction. The auction company sells the refrigerator for $250 to the highest bidder. The auction company must charge and collect sales tax on the $250.

Taxable Transactions (Purchased, used, consumed, or delivered into the City) Auctions Automotive vehicles (resident) Charitable, U. S. Government, community organization sales Coin operated device sales (tangible personal property) Construction equipment, construction materials (purchased w/o a building permit), equipment rentals w/ operator service Cover charges (if included in price of food or drink) Digital product Food and drink Freight and delivery charges (when not separately stated) Gas and electric services Internet subscription services Labor (when not separately stated) Linen services Lodging Machinery Maintenance services agreements (case-by-case basis)

Taxable Transactions (Purchased, used, consumed, or delivered into the City) Medical & retail marijuana Medical supplies Prefabricated goods and materials (including labor) Preprinted newspaper supplements Rental or lease charges Security systems services Software programs (includes license fees) Software as a service Software maintenance agreements Storage space for tangible personal property (indoor or outdoor space) Tangible Personal Property (TPP) (personal property that can be seen, weighed, measured, felt, touched, stored, transported, exchanged) Telecommunication equipment & services Questions? ?

Tax-Exempt Transactions Charitable, U. S. Government, community organization purchases Cigarettes Coins Commercial packaging/shipping materials (conveyed to the purchaser & not returnable) Construction materials (if purchased with a building permit) Food purchased with food stamps Freight & delivery (when separately stated) Garage sales (max of 3 per year) Gas & electric services (industrial use) Internet access services Labor (when separately stated) Lodging (30 or more days) Maintenance service agreements (optional, when parts are properly taxed) Manufacturing inventory (for resale) Medical supplies (those deemed tax-exempt under LMC)

Tax-Exempt Transactions Motor fuel Newspapers Prescription drugs (for both humans & animals) Prosthetic devices (for both humans & animals) Membership fees Rental or lease inventory purchases (TPP) Sales to public utility or railroad Software program (custom, hourly) Software maintenance agreement (technical support) Special fuel Therapeutic devices Telecommunications services (toll free, carrier access, private communication) Wholesale/resales Questions? ?

Tax-Exempt Transactions How do you document a tax-exempt sale? Ø Tax-exempt organization sale: Exemption certificates issued by the Colorado Dept. of Revenue are required for charitable, government, non-profit organizations. (98 -******) Ø Wholesale: A Wholesales tax license is required. Items being purchased must be associated with the purchasers’ business. Verify tax exemption certificates and license numbers @ https: //www. colorado. gov/revenueonline The seller is responsible in determining if the exemption is valid. If invalid or tax license has expired, you are responsible for the tax.

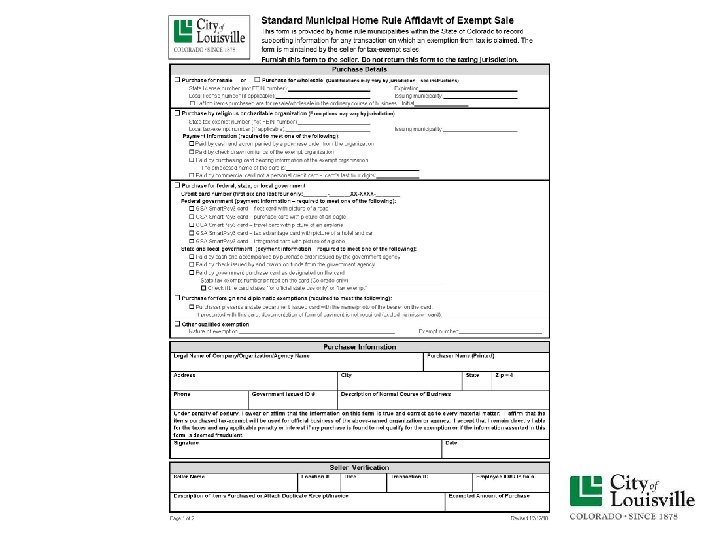

Tax-Exempt Transactions Acceptable payment methods for charitable, government, or non-profit organizations: Ø Purchases over $100 must be made using entity funds (Check or Credit Card only) Ø Local government purchases must be made with a purchase card (p-card) Ø State and Federal governments use multiple p-cards OR Ø Have the entity complete a Standard Municipal Home Rule Affidavit

Coupons / Gift Certificates / Trade Discounts Examples A grocery store offers a $10 off store coupon on the purchase of $50 worth of groceries. The coupon reduces the taxable purchase price to the customer and sales tax should be calculated on the reduced price.

Coupons / Gift Certificates / Trade Discounts Examples A grocery store offers a $10 off store coupon on the purchase of $50 worth of groceries. The coupon reduces the taxable purchase price to the customer and sales tax should be calculated on the reduced price. A soft drink manufacturer publishes clip-out coupons in an area newspaper offering $1. 00 off the purchase of their product. Sales tax should be charged to the customer on the full original price of the item, and the $1. 00 discount is subtracted after tax.

Coupons / Gift Certificates / Trade Discounts Examples A grocery store offers a $10 off store coupon on the purchase of $50 worth of groceries. The coupon reduces the taxable purchase price to the customer and sales tax should be calculated on the reduced price. A soft drink manufacturer publishes clip-out coupons in an area newspaper offering $1. 00 off the purchase of their product. Sales tax should be charged to the customer on the full original price of the item, and the $1. 00 discount is subtracted after tax. A book seller buys and sells books. Customers bring in used books and receive a trade-in credit to be used towards future purchases. Sales tax should be calculated and remitted on the sales price after applying the credit.

Coupons / Gift Certificates / Trade Discounts Examples A coffee shop utilizes loyalty punch cards. A customer buys a latte and receives one punch on their card. Sales tax should be calculated and remitted on the full price of the latte. The same customer buys a latte the following week and has a full punch card to present for payment. No sales tax is charged on the latte.

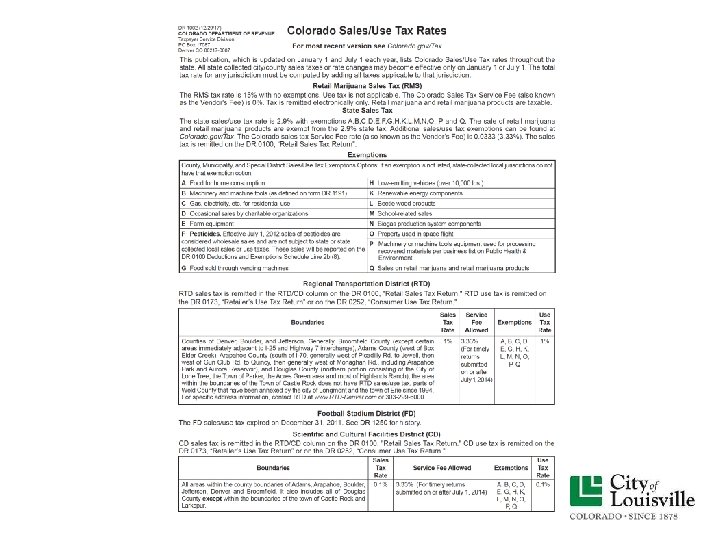

Home Rule and State Collected Cities / Counties Home Rule Cities / Counties (HR): The ability to exercise local control of individual governments. A home rule charter allows cities/counties to collect and enforce local sales and use taxes. State Collected Cities / Counties (SC): Statutory cities, towns, and counties are limited to exercising powers that are granted by the state and are subject to provisions and limitations imposed by the state. DRP 1002 State of Colorado – Sales Tax Rate Publication

In-Person Sales Items are taxed based on the seller’s location. The buyer is standing in the store and will be taking the items with them. All jurisdictions are shared with the seller. The sales tax rate of the seller is charged.

Transfer of Ownership Transfer of ownership is determined based on the location where title passes from the seller to the purchaser Ø If the purchaser picks up the items at the seller’s location, transfer of ownership has occurred at the seller’s location (in-person sale) Ø If the purchaser pays for shipping of the items to their location, transfer of ownership has occurred at the seller’s location (in-person sale) Ø If the seller ships or delivers the items to the purchaser’s location, transfer of ownership has occurred at the purchaser’s location (out of City sale)

Shipping / Delivery Outside the City Items shipped or delivered outside of the City are exempt from City sales tax when all of the following conditions are met: Ø The sales are to those who reside or do business outside the City and articles shipped or delivered are used outside the City. Ø The articles purchased are shipped to the purchaser outside the City by common, contract or commercial carrier, by mail, or by the seller’s vehicle, but at all times at the seller’s expense. Ø The seller retains full ownership and liability for all articles being shipped or delivered to the destination outside the City. **Items delivered are subject to another jurisdiction’s tax rate**

South Dakota v. Wayfair Inc. The Supreme Court Decision Ø Overturned Quill v. North Dakota (1992) - Physical Nexus Ø Out-of-state retailers may be required to collect sales tax even if they have no physical nexus in a state or city - Economic Nexus Ø Sales tax is now based on the physical location of the purchaser Ø Some sellers already voluntarily collect and remit sales tax on the full tax rate for the purchaser’s location.

Economic Nexus For out of state retailers, the State of Colorado has set the Economic Nexus thresholds of: $100, 000+ in sales or 200+ transactions per calendar year June 1, 2019: All Colorado retailers must collect and remit Colorado sales tax based on the physical location of the purchaser, combined with the jurisdiction collection type: (SC) STATE COLLECTED (City/County) (HR) HOME RULE (City/County)

Taxing Example-Physical Nexus In-State SALE shipped to Superior from Louisville RTD/ CD 1. 1% Louisville (HR) State of Colorado 2. 9% Boulder County (SC). 985% Town of Superior (SC)

Taxing Example-Economic Nexus In-State SALE shipped to Superior from Louisville (HR) Boulder County (SC). 985% RTD/ CD 1. 1% State of Colorado 2. 9% Town of Superior (SC) 3. 46%

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Superior RTD/ CD 1. 1% Louisville (HR) Boulder County (SC). 985% State of Colorado 2. 9% Town of Superior (SC)

Taxing Example-Economic Nexus In-State SALE shipped to Longmont from Louisville RTD/ CD 1. 1% Louisville (HR) Boulder County (SC). 985% State of Colorado 2. 9% Longmont (HR)

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Longmont RTD/ CD 1. 1% Louisville (HR) Boulder County (SC). 985% State of Colorado 2. 9% Longmont (HR)

Taxing Example-Economic Nexus In-State SALE shipped to Denver from Louisville (HR) Boulder County (SC) RTD/ CD State of Colorado Denver (HR) Denver County (HR)

Taxing Example-Economic Nexus In-State SALE shipped to Denver from Louisville (HR) Boulder County (SC) RTD/ CD 1. 1% State of Colorado 2. 9% Denver (HR) Denver County (HR)

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Denver Louisville (HR) Boulder County (SC) RTD/ CD State of Colorado Denver (HR) Denver County (HR)

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Denver Louisville (HR) RTD/ CD 1. 1% State of Colorado 2. 9% Boulder County (SC). 985% Denver (HR) Denver County (HR)

Taxing Example-Economic Nexus In-State SALE shipped to Ft. Collins from Louisville RTD/ CD Ft. Collins State of Colorado Boulder County Larimer County

Taxing Example-Economic Nexus In-State SALE shipped to Ft. Collins from Louisville (HR) Boulder County (SC) RTD/ CD State of Colorado 2. 9% Ft. Collins (HR) Larimer County (SC). 8%

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Ft. Collins Louisville RTD/ CD State of Colorado Boulder County Ft. Collins Larimer County

Taxing Example-Economic Nexus In-State PURCHASE shipped to Louisville from Ft. Collins Louisville (HR) RTD/ CD 1. 1% Ft. Collins (HR) State of Colorado 2. 9% Boulder County (SC). 985% Larimer County (SC)

Economic Nexus-Out of State Sales Both Physical Nexus and Economic Nexus determine whether a Colorado business making sales into another state is liable for collecting sales tax Research individual state guidelines and remittance thresholds @ www. streamlinedsalestax. org

Sales Tax Summary Ø Where does transfer of ownership take place: • In-Person • Shipped • Delivered Ø Sales tax rate is determined by: • Economic Nexus • Physical Nexus • Jurisdiction collection type (Home Rule / State Collected) Ø You can be audited by another city for non-payment of sales tax Ø If your company delivers goods outside the City, retain a copy of the signed delivery receipts When would you charge sales tax on items shipped outside the City?

Topics üAuto Use Tax üBuilding Use Tax üInitial Use Tax üConsumer Use Tax üTaxable Services üSamples, Demonstrations, Displays üGiveaways üUnlawfully Imposed Tax

What is Use Tax ? Use tax was adopted by the State of Colorado to help ensure that cities having limited retail establishments would be able to generate revenue by taxing the “use” of goods in addition to the “sale” of goods Use tax is based on the location of the “use” of the item Use tax is a complement to sales tax, it is not an additional tax When a vendor has not charged sales tax, the purchaser must pay use tax. Use tax does not apply to inventory actually sold in the normal course of business Use tax due to the City is reduced by the amount of sales or use tax legally paid to another jurisdiction up to the City’s tax rate

Auto Use Tax / Building Use Tax Auto Use Tax When the full sales tax rate is not paid at the time of purchase, use tax is due. The Boulder County Clerk is authorized by the City to collect the Louisville portion of the use tax prior to, or at the time, of registration Building Use Tax Use tax is collected in full prior to the issuance of a building permit for all construction/building projects taxed under the LMC. The Louisville Building Department, as designee for the Finance Director, is responsible to collect such tax as part of the building permit process

Initial Use Tax Initial use tax is a one-time tax that may be owed to the City of Louisville on the assets, equipment, and supplies purchased or brought into the City in order to operate a new business Ø Does not apply to inventory items or to raw materials manufactured into a finished product for resale Ø When an in-City transfer of ownership includes assets as part of a lump sum transaction, use tax due is based on the fair market value of the property, or the book value established by the purchaser for depreciation purposes ØApplies to all purchases made within 3 years of moving to or starting a business in the City

Taxable Services Ø Some services taxed under the LMC include telecommunications, gas & electric services, security monitoring, and linen services Ø In general, service providers are not required to collect Louisville sales tax (ex: accounting, legal, planning, design services) Ø Service providers are consumers, not retailers, of the tangible personal property (TPP) used in rendering their services

Taxable Services To determine if a transaction involves the sale of TPP or the performance of a service with an incidental transfer of TPP, the City examines the transaction from the purchaser’s perspective: “What does the purchaser want? ” If a service is performed in the production of TPP and the essence of the transaction is the acquisition of the TPP produced, the transaction is taxable If the essence of the transaction is the acquisition of a service, the transaction is not taxable, even if some amount of TPP is transferred to the purchaser If a retailer has not charged the service provider sales tax, the service provider must remit consumer use tax

Use Tax Due? All Louisville businesses must pay sales or use tax on purchases of tangible personal property (TPP) or taxable services that are not purchased for resale, or which are not specifically exempted per the Louisville Municipal Code How do I determine what sales tax rate was paid? How do I calculate use tax due?

Calculate How Much Use Tax is Owed: Out of State Purchase-Shipped Printing Palace Santa Fe, NM Invoice 52694 1000 Business Cards 5000 Letterhead $75. 00 120. 00 Subtotal $195. 00 Shipping/Handling 15. 00 Total $210. 00 Note: Louisville does not tax shipping when separately stated. No sales tax was charged/paid. City of Louisville use tax of 3. 65% is due on the subtotal: ($195. 00 x. 0365 = $7. 12) Seller does not meet Colorado economic nexus threshold

Calculate How Much Use Tax is Owed: Out of State Purchase-Shipped Sample Company – Provo, UT 1000 Business Cards $75. 00 5000 Letterhead 120. 00 Subtotal $195. 00 Shipping/Handling 15. 00 Tax 10. 47 Total $220. 47 Note: The State taxes shipping and freight charges To determine tax rate charged, divide the tax by subtotal (plus S/H): ($10. 47/$210. 00 =. 04985) State (2. 9), RTD/CD (1. 1), Boulder County (. 985) = 4. 985% City of Louisville use tax of 3. 65% is due on the subtotal: ($195. 00 x. 0365 = $7. 12) Seller meets Colorado economic nexus threshold

Calculate How Much Use Tax is Owed: In-State Purchase-Shipped Computer Source – Denver, CO Invoice #475 1 Laptop Discount Subtotal $1, 450. 00 -200. 00 $1, 250. 00 Shipping 20. 00 Tax 63. 31 Total $1, 333. 31 Note: The State taxes shipping and freight charges To determine tax rate charged, divide the tax by subtotal (plus S/H) ($63. 31 / $1, 270. 00 =. 04985) State (2. 9) RTD/CD (1. 1) Boulder County (. 985) = 4. 985% City of Louisville use tax of 3. 65% is due on the subtotal: ($1, 250. 00 x. 0365 = $45. 63)

Calculate How Much Use Tax is Owed: In-Person Purchase Sample Company – Longmont, CO 1 Laptop Discount Subtotal $1, 450. 00 -200. 00 $1, 250. 00 Shipping (Cust pick-up) Tax No Charge 106. 44 Total $1, 356. 44 To determine tax rate charged, divide the tax by the subtotal: (106. 44 / 1, 250. 00 =. 08515) . 08515 - . 029 State =. 05615 - . 011 RTD/CD =. 04515 -. 00985 Boulder County = . 0353 - . 0365 City of Louisville -. 0012 No use tax is due Note: Point-of-sale is Longmont

Calculate How Much Use Tax is Owed: In-Person Purchase Precision Tool – Dacono, CO Invoice 2001 To determine tax rate charged divide the tax by the subtotal: ($876. 15 / $29, 205. 00 =. 03) CNC Metal Lathe W 28 -750 $29, 205. 00 Subtotal $29, 205. 00 Shipping/Freight (Customer pick-up) No Charge Tax 876. 15 Total $30, 081. 15 Note: Point-of-sale is Dacono • City of Dacono: -tax rate = 3%. -manu. equipment exempt -not in the RTD District Difference between City of Louisville 3. 65% and City of Dacono 3% is due on the subtotal: ($29, 205. 00 x. 0065 = $189. 83)

Calculate How Much Use Tax Is Owed: In-Person Purchase / Mixed Invoice Costco - Superior, CO Invoice 10256 1 – Printer $185. 00 3 – Cases Water 10. 50 1 – 5 lbs Coffee 30. 00 Subtotal (Customer pick-up) Tax Total $242. 52 $17. 02/225. 50 =. 0754 = 7. 54%? ? -Printer is taxable for all jurisdictions -State exempts food for home consumption $185. 00 x 8. 445% = $15. 62 $225. 50 $40. 50 x 3. 46% = 1. 40 No Charge $ 17. 02 . 0346 (Rounds to. 035) -. 0365 City of Louisville . 0019 No use tax is due Note: Point-of-sale is Superior

Calculate How Much Use Tax Is Owed: Unlawfully Imposed Tax Furniture Factory-Commerce City, CO Invoice 688 5 Sit-Stand Desks $2, 500. 00 1 Conference Table 750. 00 Subtotal $3, 250. 00 Shipping/Freight $200. 00 Tax 319. 12 Total $ 3, 769. 12 To determine the tax rate charged divide the tax by the subtotal (plus S/H): $319. 12 / $3, 450 = (9. 25%) State 2. 9 RTD/CD 1. 1 Adams County . 75 Commerce City 4. 5 9. 25% Should have collected: State, RTD/CD, Bldr Cnty Only (4. 985%) ($3, 450 x. 04985 = $171. 98) City of Louisville use tax of 3. 65% is due on the subtotal: $3, 250. 00 x. 0365 = $118. 63 Note: The State taxes Shipping/Freight

Samples / Demos / Displays For a sample, demo, or display unit to be tax-exempt, the retailer or wholesaler cannot make any use, other than incidental use, of the item prior to resale. When a retailer or wholesaler’s use of an inventory item is more than incidental, then the use becomes a taxable transaction, separate and distinct from the retailer’s subsequent taxable retail sale of the item to the end customer.

Samples / Demos / Displays Example Louisville Peak Sports is a sporting goods manufacturer located in the City. The marketing manager regularly ships out samples of their products to potential clients. Would the samples be subject to use tax?

Samples / Demos / Displays Example Louisville Peak Sports is a sporting goods manufacturer located in the City. The marketing manager regularly ships out samples of their products to potential clients. Would the samples be subject to use tax? Yes, the samples being used for marketing purposes are subject to use tax to the business on the cost of the sample units.

Samples / Demos / Displays Example Louisville Peak Sports also operates a retail store in the City. The business displays various items on the sales floor that customers can try out. Are the displayed items subject to use tax?

Samples / Demos / Displays Example Louisville Peak Sports also operates a retail store in the City. The business displays various items on the sales floor that customers can try out. Are the displayed items subject to use tax? Yes, and if some of the displayed items are eventually sold, either at the full retail price or a reduced price, the transaction is subject to sales tax.

Samples / Demos / Displays Example Louisville Peak Sports has a research & development team that creates new products. Raw materials such as fabric, metal, screws, etc. are pulled from inventory and prototypes are then manufactured for further testing. Are the prototypes subject to use tax?

Samples / Demos / Displays Example Louisville Peak Sports has a research & development team that creates new products. Raw materials such as fabric, metal, screws, etc. are pulled from inventory and prototypes are then manufactured for further testing. Are the prototypes subject to use tax? Yes, any materials used in creating the prototype are subject to use tax, regardless of whether or not the item goes into full production. If the prototype is eventually sold, the transaction is subject to sales tax.

Giveaways Example Louisville Peak Sports regularly attends trade shows and events. T-shirts are pulled from inventory and taken to the event location to sell. A few are worn by employees. What is the tax consequence in this scenario?

Example Giveaways Louisville Peak Sports regularly attends trade shows and events. T-shirts are pulled from inventory and taken to the event location to sell. A few are worn by employees. What is the tax consequence in this scenario? The T-shirts worn by the employees are subject to use tax where they were removed from inventory. Any T-shirts sold are sales taxable at the point of sale (in-person purchase). Any unsold, unaltered merchandise returned to inventory is not use taxable.

Giveaways Example A coffee shop annually hosts a customer appreciation day. Everyone who comes in on that day is entitled to a free coffee.

Giveaways Example A coffee shop annually hosts a customer appreciation day. Everyone who comes in on that day is entitled to a free coffee. Use tax must be paid by the coffee shop on all product given away.

Use Tax Calculation Tool City staff can not act as your accountants. If you or your accountant already have processes in place, please continue to use them. Introduction to Excel worksheet that can be used as an aid to help you determine your use tax liability. Mixed purchase invoices cannot be calculated with the use tax worksheet. Note: State and RTD/CD use tax may also be due.

Use Tax Calculation Tool City staff can not act as your accountants. If you or your accountant already have processes in place, please continue to use them! Introduction to Excel worksheet that can be used as an aid to help you determine your use tax liability. Mixed purchase invoices cannot be calculated with the use tax worksheet. Note: State and RTD/CD use tax may also be due.

Review of Sample Tax Return Louisville Peak Sports – Monthly Summary Information Ø Gross Sales & Service: $188, 792 Sales (excluding sales tax collected) Ø Sales to Other Licensed Dealers: $42, 000 Ø Sales Shipped Out of City: $19, 731 Ø Sales to Government or Charitable Organizations: $475 Ø Amount of City of Louisville Tax Collected: $4, 625 Ø Use Taxable Purchases: $6, 370

On-Line Business Tax Manager You can: ØUse the self-calculating tax return ØRemit a zero return ØFile and pay taxes via e-check or CC ØRenew your City license ØUpdate your business contact information ØView your payment history

Recordkeeping All tax returns are due on the 20 th day of the month following your filing period and must be postmarked (by the USPS) or dropped off on or before the due date Maintain copies of all exemption certificates or resale licenses, along with any other support documentation Keep all signed delivery receipts Note: 3 Year retention period for documents

Penalties / Interest / Enforcement Penalties = 10% of tax due / $15 minimum Interest = 1% per month Collection & Enforcement Assessment (fee $25) Lien (fee $40) County Certification Municipal Court Summons Distraint Warrant / Seizure

Questions? ? Taxable and Exempt Transactions Sales Tax Transfer of Ownership Economic Nexus Shipping/Delivery Charging/Collecting Use Tax Auto, Building, Initial Use Tax Samples, Demonstrations, Displays Giveaways Unlawfully Imposed Tax Calculation & Remittance of Taxes Self-Calculating Worksheet Online Portal

Thank you for Attending Today! Please take a few minutes to fill out the evaluation form, your feedback is greatly appreciated!