MANAGING THE SALES TAX EXEMPTION CERTIFICATE BEST PRACTICES

MANAGING THE SALES TAX EXEMPTION CERTIFICATE: BEST PRACTICES AND LEGAL CONSIDERATIONS Thadd Curry Ariat International Thadd. Curry@Ariat. com Matthew Mac. Neil Avalara Certcapture Matthew. Macneil@Avalara. com Scott E. Blakeley, Esq. Blakeley LLP SEB@Blakeley. LLP. com

AGENDA The Sales Tax Process 2. Exemption Certificates 1. a. b. c. d. 3. Controlling Certificates a. b. c. 4. Nexus Managing the Sales Tax Exemption Certificate Process Types of Certificates and Forms Drop Shipments Common Problems Sales Tax Collection Consequences of Failing to Collect Sales Tax A Look Ahead

Overview • Responsibility for managing sales tax exemption certificates historically falls upon the credit team • State taxing authorities recognize the mismanagement of exemption certificates and see it as one of the easiest way to collect funds for the state. Other taxes 3. 9% Corporation net income taxes 5. 3% Total license taxes 6. 8% Total selective sales taxes 16. 6% General sales and gross receipts taxes 30. 5% Property taxes 1. 6% Individual income taxes 35. 3% When general sales tax and selective sales tax are combined, sales tax makes up 47% of total state revenue

Exemption Certificates Nexus • Collect sales taxes and certificates if you have Nexus in the state • What it takes to achieve Nexus in most states In most states, a “physical presence” usually creates nexus and can mean a number of things, including: • • Having an office Having an employee Having a warehouse Having an affiliate Storing inventory Drop shipping from a 3 rd party provider Temporarily doing physical business in a state (trade show, fair, etc. )

Exemption Certificates Managing the Sales Tax Exemption Certificate Process • Collection of certificates as part of the new account set-up process • Validation of certificate • Maintaining the certificates Collect Information Validate Exemption Status for easy retrieval • Monitoring expiration dates Monitor Expiration Dates Maintain for Retrieval

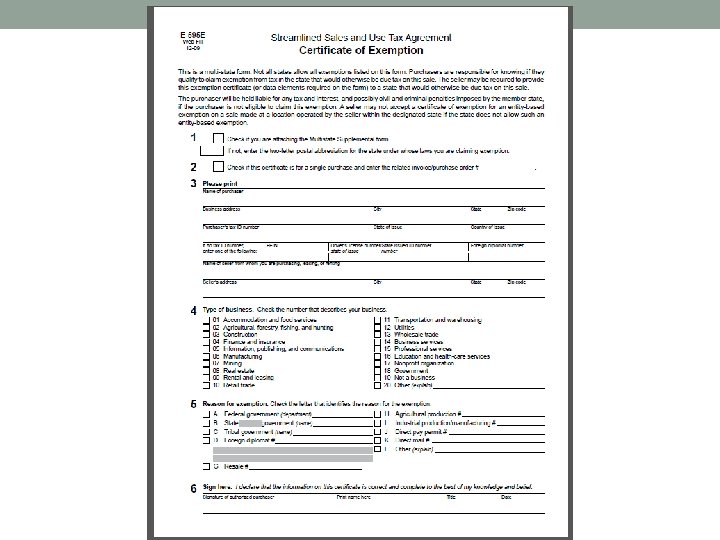

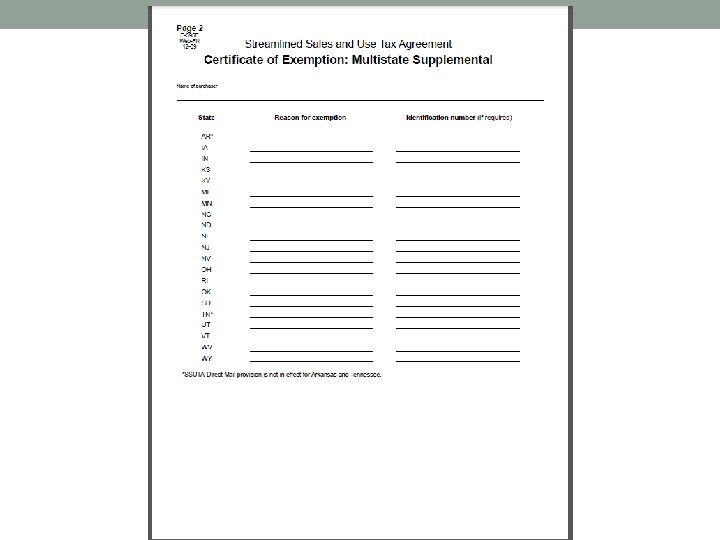

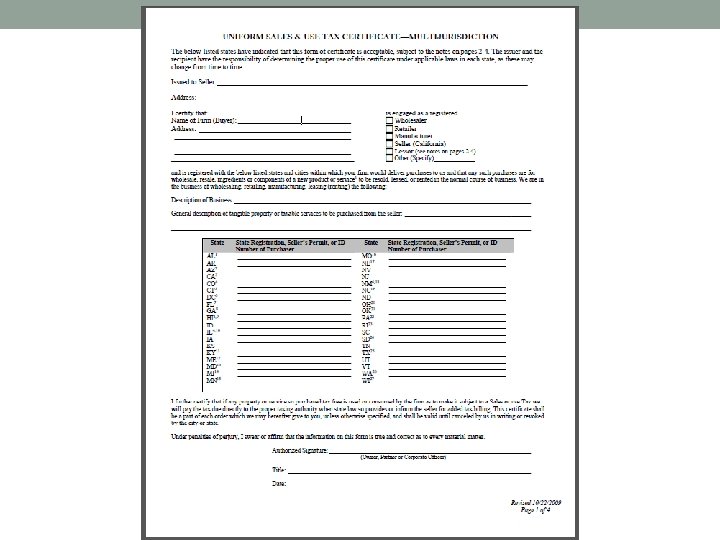

Exemption Certificates Considerations for Valid Exemption Certificate Sales Tax Registration number Buyer and Seller Name Signature and Date Reason for exemption

Exemption Certificates Resale Certificates • Merchandise intended for resale • Tangible personal property purchase to lease or rent • Taxable service performed on tangible personal property in resale inventory Direct Pay Permits • Purchases by Governments and Non-profits • SST Form • MTC Form • State Issued Form

Exemption Certificates: Drop Shipments Consideration of Sales Tax in Drop Shipments NEXUS • Is the Seller registered to collect tax in the destination state? • Is the Buyer able to provide an exemption certificate in the destination state? Seller price Seller/Buyer Order Customer Delivery Supplier price Supplier Resale Certificate

Drop Shipment Most Common Alabama Arizona Colorado Georgia Idaho Illinois ** Indiana Iowa Kansas Kentucky Maine Michigan Minnesota Missouri Nebraska New Jersey New Mexico New York North Carolina North Dakota Ohio Pennsylvania Rhode Island South Carolina South Dakota Texas Utah Vermont Virginia Washington Wyoming Nevada as of 10/1/2007 Wisconsin as of 10/1/2009 West Virginia as of 12/31/2007 ** Illinois – a resale # can be obtain without establishing nexus and/or a written statement that Buyer has no nexus should be sufficient. http: //12. 43. 67. 2/commission/jcar/adm incode/086001300 B 02250 R. html

Drop Shipment Not So Common Pass-through – Customer could issue resale/ exemption certificate to Supplier via Seller. Resale/Exemption Certificate NEXUS Seller price Seller/Buyer Order Customer Delivery Supplier price Supplier Resale Certificate + Customer Certificate

Drop Shipment Pass-through States that fall under this category: California Massachusetts Mississippi Tennessee Nevada prior to 10/1/2007* Wisconsin prior to 10/1/2009 * If no certificate is received, tax will be calculated accordingly: Seller price Supplier price California + 10% markup of supplier price! Massachusetts Wisconsin prior to 10/1/2009 * * Nevada Note - http: //tax. state. nv. us/documents/27026_TAX%20 NOTES. pdf * Wisconsin Note - http: //www. revenue. wi. gov/taxpro/news/100119. html

Drop Shipment First On Board • Sale occurred outside the nexus State • Inventory shipped from outside the State • Supplier can accept seller certificate NEXUS Seller price Seller/Buyer Order Supplier Warehouse Customer Delivery Supplier price Supplier Resale Certificate

Drop Shipment – First On Board States that fall under this category: Seller’s certificate of exemption can be accepted. Connecticut Florida Louisiana West Virginia prior to 12/31/2007** Arkansas ** Oklahoma ** ** West Virginia Note – West Virginia became a full member of SST 10/1/05. The regulations changed 12/31/07 to accept the drop shipment rules from SST. http: //www. legis. state. wv. us/WVCODE/Code. cfm? chap=11&art=15 B#15 B ** Arkansas Note – Arkansas became a full member of SST 1/1/08, the regulations are conflicting. In SST, Arkansas should accept the resale certificate regardless of FOB, but the regulations still state that documentation should be retained to prove origin. http: //www. sos. arkansas. gov/elections_pdfs/register/nov-dec_06/006. 05. 06 -005. pdf ** Oklahoma Note – Oklahoma became a full member of SST 10/1/05, the regulations are conflicting. In SST, Oklahoma should accept the resale certificate regardless of FOB, but the regulations were just amended in February, 2010 to include the language. http: //www. oar. state. ok. us/register/Volume-27_Issue-10. htm#a 30978

Drop Shipment Taxable • Taxable transaction NEXUS Seller price Seller/Buyer Order Customer Delivery Supplier price Supplier Tax due to supplier

Drop Shipment Taxable District of Columbia Hawaii Maryland • Maryland - http: //www. dsd. state. md. us/comarhtml/03/03. 06. 01. 14. htm http: //business. marylandtaxes. com/news/taxtips/business/bustip 04. asp • Hawaii – http: //suiteswaikiki. com/Suites. Waikiki/Resources/GET. pdf • District of Columbia http: //weblinks. westlaw. com/result/default. aspx? cite=UUID%28 N 2266 D 14095%2 DE 311 DB 9 BCF 9%2 DD AC 28345 A 2 A%29&db=1000869&findtype=VQ&fn=%5 Ftop&ifm=Not. Set&pbc=4 BF 3 FCBE&rlt=CLID%5 F FQRLT 8063617416166&rp=%2 FSearch%2 Fdefault%2 Ewl&rs=WEBL 10%2 E 06&service=Find&spa=DC C%2 D 1000&sr=TC&vr=2%2 E 0

/Billing Software • Is the customer")

Exemption Certificates - Automation • Enterprise Resource Planning (ERP)/Billing Software • Is the customer exempt • What states are they exempt in • What are the start AND end dates for the exemptions • Third Party software for exemption management • Track expirations • Mass mailing tools • Form library • Remember to link to Tax Decision Software

Controlling Certificates: Common Problems • Audit Trends and Regulations • Rejection of certificates • Contractors

Sales Tax Collection Once the vendor has nexus and the purchaser does not have a valid exemption certificate, the vendor must begin its collection process • Problems with collection • Preventative measures • Collection shouldn’t be a burden on seller if done right

Consequences of Failing to Collect Sales Tax When Vendor Does Not Have A Valid Exemption Certificate • YOU will be responsible for paying any taxes that are nor supported by an exemption certificate • YOU will pay all late fees and penalties the states finds are due • Your company may lose its privilege to do business within the state • The buyer will almost never pay you back for these charges

3 Things to Improve Your Process 1. Document exempt buyers as part of the new customer on-boarding process. 2. Set a policy to review form expirations on a regular basis. 3. Enforce a policy of taxation if no exemption forms are present.

Exemption Certificates: A Look Ahead • Less exemptions allowed, wider tax base in exchange for lower tax rates • Nexus standards being challenged • Economic Nexus based on total sales in a state • National standard for audit and exemption forms under next generation of streamlined sales tax • Shorter life span on exemption forms (WA, LA, AL, GA)

")

Exemption Certificates: A Look Ahead Future of Sales tax Tax collection (or exemption collection) will eventually be required by all companies on all sales. Short term, only the companies with over $100, 000 in sales in a state will be required to comply. Eventually everyone will be required to file and be subject to audit.

- Slides: 25