Measuring and Managing Translation and Transaction Exposure Chapter

(14) 108 30")

和霸菱銀行(Barings PLC)的破�,以及 Metallgesellschaft、Kidder Peabody、住友商事(Sumitomo)、瑞士聯合銀 行(Union Bank of Switzerland)和寶鹼(Procter & Gamble)所發生的巨額損失。 45")

3. Parties would share the currency")

- Slides: 70

Measuring and Managing Translation and Transaction Exposure Chapter 10 1

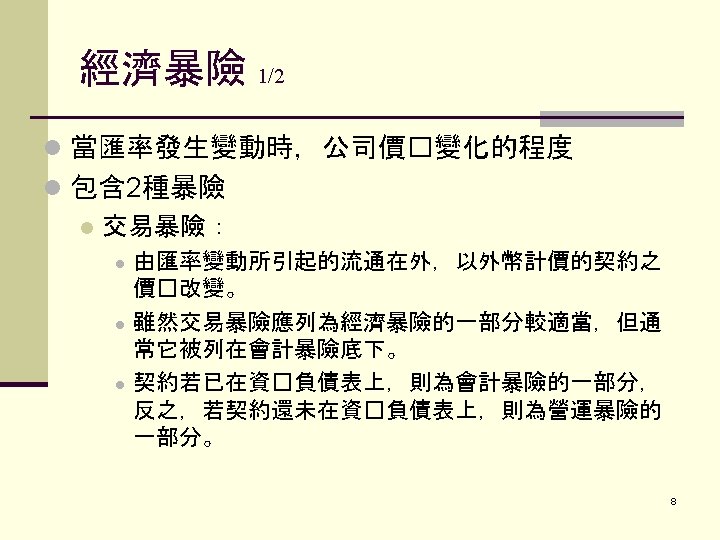

PART I. ALTERNATIVE MEASURES OF FOREIGN EXCHANGE EXPOSURE: Accounting and Economic Risk I. ALTERNATIVE MEASURES A. TYPES 1. Accounting Exposure: 會計暴險 arises when reporting and consolidating financial statements require conversion from subsidiary to parent currency. 2. Economic Exposure: 經濟暴險 arises because exchange rate changes alter the value of future revenues and costs. 3

Accounting Exposure B. Accounting Exposure = C. Transaction risk交易暴險+ Translation risk換算暴險 4

How Accounting Exposure Arises Translation Risk Japan Subsidiary Financials ¥ United States £ Headquarters’ £ Consolidated Financials Subsidiary Financials $ £ Subsidiary Financials € Germany 5

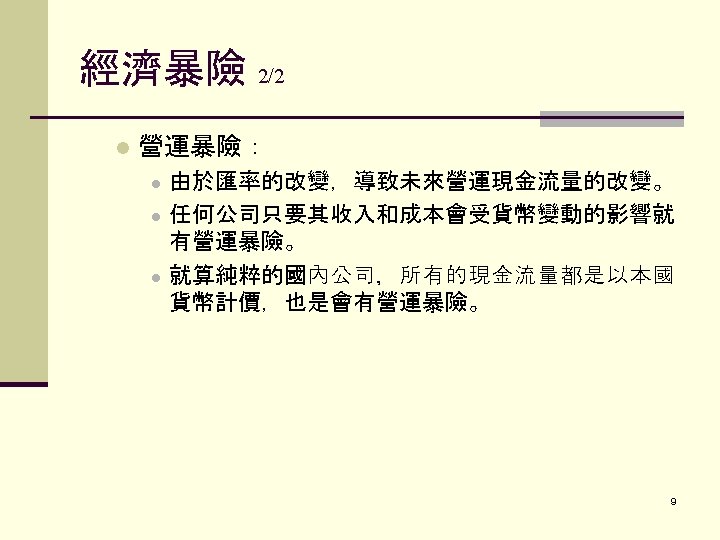

ALTERNATIVE MEASURES OF FOREIGN EXCHANGE EXPOSURE C. Economic Exposure = Transaction Exposure交易暴險+Operating Exposure營運暴險 Operating Exposure arises because exchange rate changes alter the value of future revenues and costs. 7

PART II. ALTERNATIVE CURRENCY TRANSLATION METHODS I. FOUR METHODS OF TRANSLATION A. Current/Noncurrent Method 1. 2. Current accounts use current exchange rate for conversion. Income statement accounts use average exchange rate for the period. 12

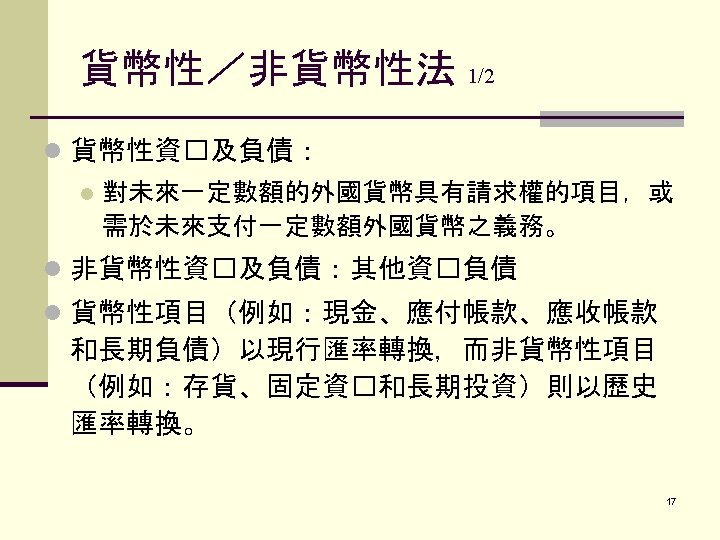

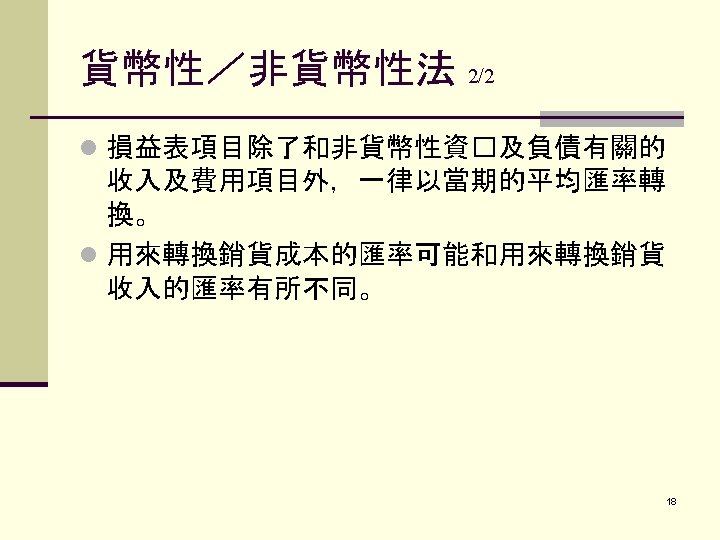

ALTERNATIVE CURRENCY TRANSLATION METHODS B. Monetary/Nonmonetary Method 貨幣性/非貨幣性法 1. Monetary accounts use current rate 2. Pertains to - Cash - Accounts receivable - Accounts payable - Long term debt 15

ALTERNATIVE CURRENCY TRANSLATION METHODS 3. 4. Nonmonetary accounts - Use historical rates - Pertains to Inventory Fixed assets Long term investments Income statement accounts - Use average exchange rate for the period. 16

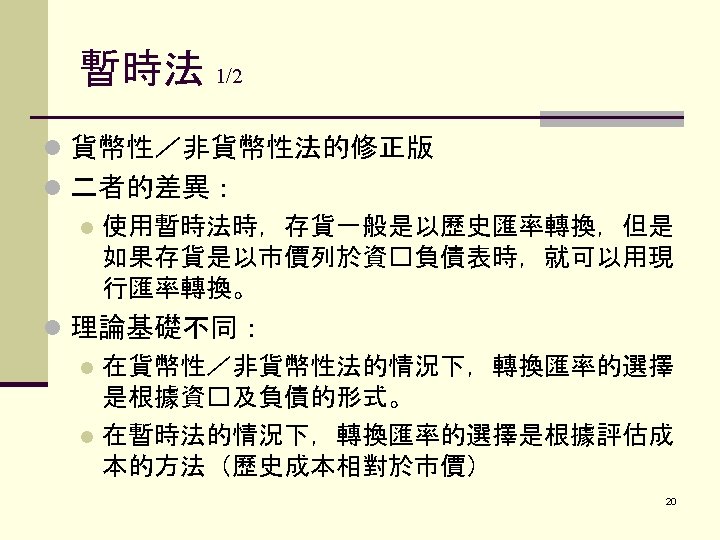

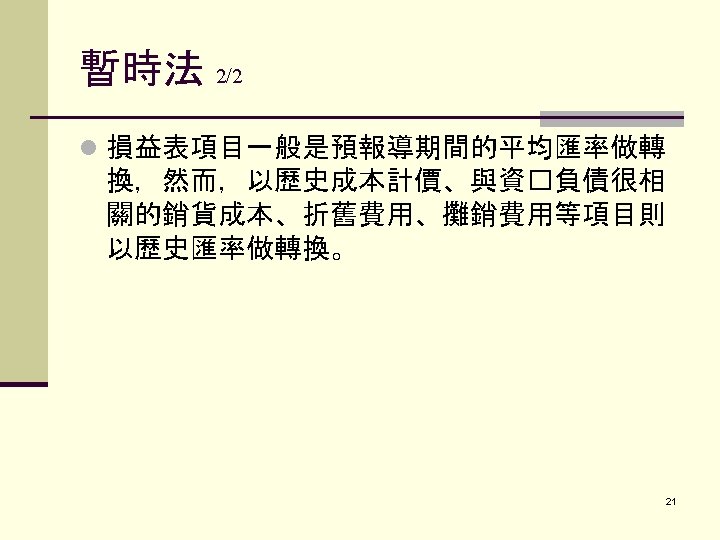

ALTERNATIVE CURRENCY TRANSLATION METHODS C. Temporal Method暫時法 1. Similar to monetary/nonmonetary method. 2. Use current method for inventory. 19

ALTERNATIVE CURRENCY TRANSLATION METHODS D. Current Rate Method現行匯率法 all statements use current exchange rate for conversions. 22

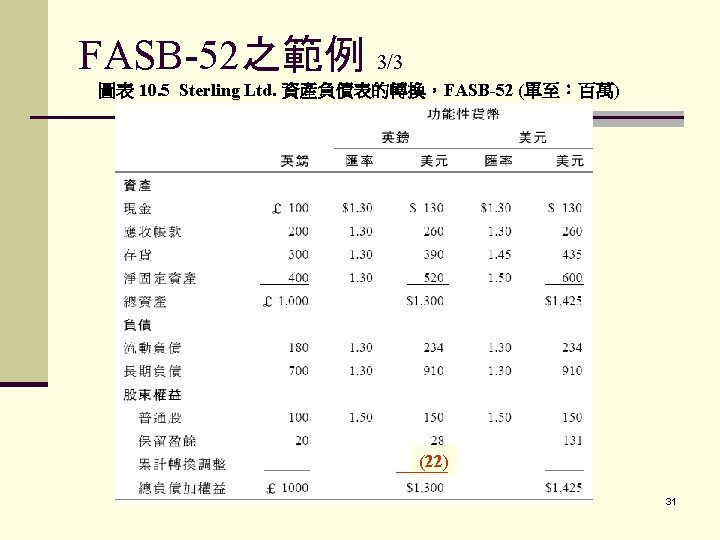

FASB-52之範例 2/3 圖表 10. 4 Sterling Ltd. 損益表的轉換,FASB-52 (單位:百萬) (14) 108 30

PART VI. ACCOUNTING PRACTICE AND ECONOMIC REALITY I. Accounting v. Economic Exposure measurement of exchange rate risk indicates major difference exists. A. Accounting exposure reflects past decisions of the firm. B. Economic exposure 1. Focuses on future impact of exchange rate changes. 2. Not all future cash flows appear on the firm’s balance sheet. 34

Sample Problem Suppose on January 1, American Golf’s French subsidiary showed: Current assets of FF 1 million; Current liabilities of FF 300, 000; Total assets = FF 2. 5 million; Total liabilities = FF 900, 000 Exchange rate on Jan 1 = $. 1270 on Dec 31= $. 1180 35

Sample Problem Under FASB-52, what is the exposure if the franc is the functional currency? - All assets and liabilities translated at current rate. At beginning of the year: FF 2, 500, 000 -FF 900, 000 = FF 1, 600, 000 x $. 1270 = $203, 200 At the end of the year: 1, 600, 000 x $. 1180 = $188, 800 36

Sample Problem This involves a translation loss for American Golf of: $203, 200 – 188, 800 = $14, 400 37

PART TWO Managing Translation and Transaction Exposure 38

PART III. DESIGNING A HEDGING STRATEGY設計避險策略 I. DESIGNING A HEDGING STRATEGY A. Strategies: a management objective B. Hedging’s basic objective: reduce/eliminate volatility of earnings as a result of exchange rate changes. 39

DESIGNING A HEDGING STRATEGY C. Hedging exchange rate risk 1. Incurs a cost 2. Should be evaluated as a purchase of insurance. 40

DESIGNING A HEDGING STRATEGY D. Centralization is key 41

風險管理失敗案例 1/3 包括橘郡(Orange County)和霸菱銀行(Barings PLC)的破�,以及 Metallgesellschaft、Kidder Peabody、住友商事(Sumitomo)、瑞士聯合銀 行(Union Bank of Switzerland)和寶鹼(Procter & Gamble)所發生的巨額損失。 45

PART II. MANAGING TRANSACTION EXPOSURE管理交易暴險 I. METHODS OF HEDGING A. B. C. D. E. F. G. Risk shifting風險移轉 Currency risk sharing貨幣風險分擔 Currency collars Cross-hedging Exposure netting Forward market hedge Foreign currency options 54

MANAGING TRANSACTION EXPOSURE A. RISK SHIFTING 1. Home currency invoicing 2. Zero sum game 3. Common in global business 4. Firm will invoice exports in strong currency, import in weak currency 5. Drawback: it is not possible with informed customers or suppliers. 55

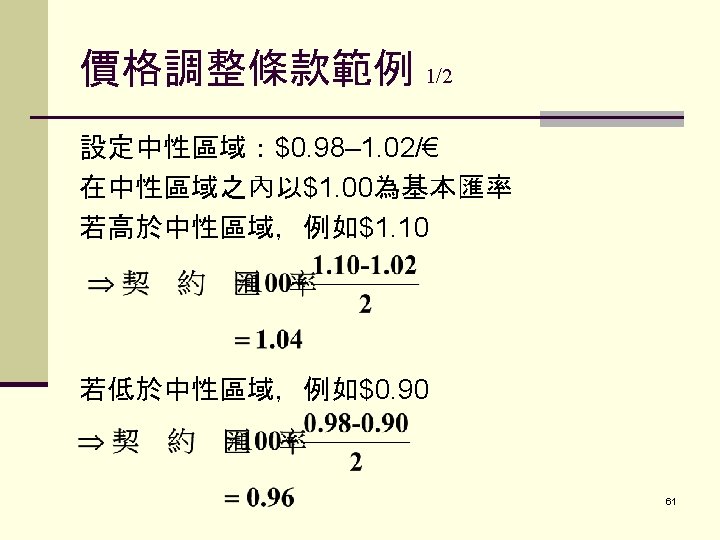

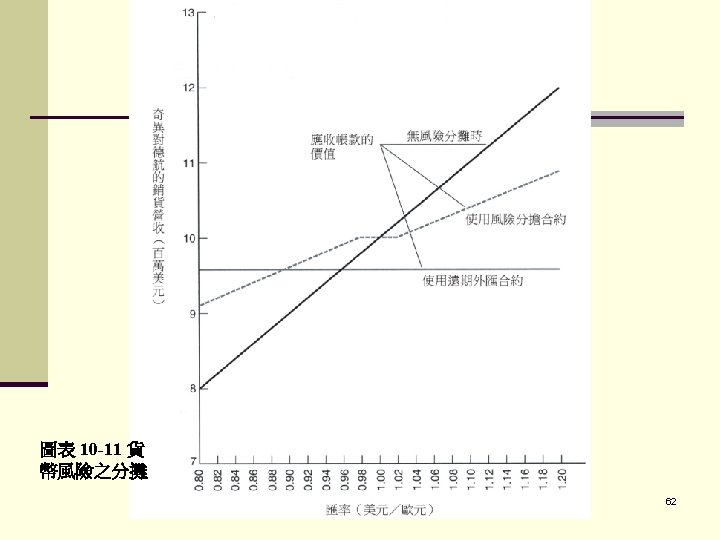

MANAGING TRANSACTION EXPOSURE B. CURRENCY RISK SHARING 1. Developing a customized hedge contract. 2. The contract typically takes the form of a Price Adjustment Clause, whereby a base price is adjusted to reflect certain exchange rate changes. 56

The Zone Take no actions $1. 50/£ $1. 60/£ Take no action 57

MANAGING TRANSACTION EXPOSURE B. CURRENCY RISK SHARING (con’t) 3. Parties would share the currency risk beyond a neutral zone of exchange rate changes. 4. The neutral zone represents the currency range in which risk is not shared. 58

MANAGING TRANSACTION EXPOSURE C. CURRENCY COLLARS 1. Contract - bought to protect against currency moves outside the neutral zone. 2. Firm would convert its foreign currency denominated receivable at the zone forward rate. 63

MANAGING TRANSACTION EXPOSURE D. CROSS-HEDGING 1. Often forward contracts not available in a certain currency. 2. Solution: a cross-hedge - a forward contract in a related currency. 3. Correlation between 2 currencies is critical to success of this hedge. 64

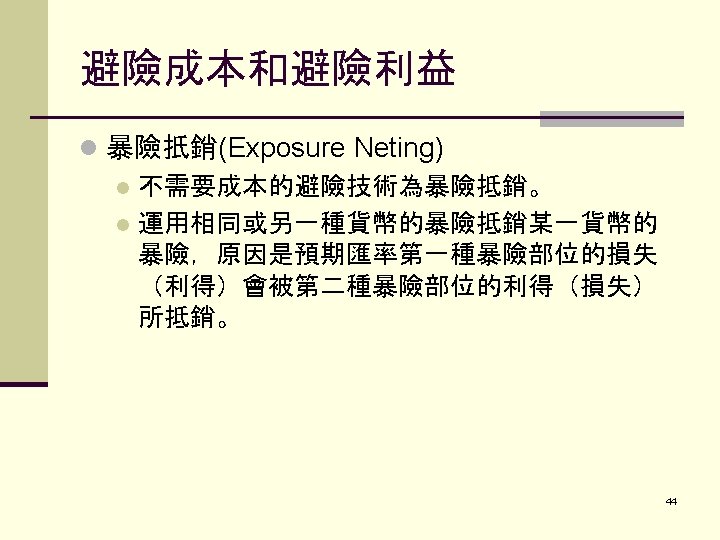

MANAGING TRANSACTION EXPOSURE E. EXPOSURE NETTING 1. Protection can be gained by selecting currencies that minimize exposure 2. Netting: MNC chooses currencies that are not perfectly positively correlated. 3. Exposure in one currency can be offset by the exposure in another. 65

PART III. MANAGING TRANSLATION EXPOSURE A. Choices faced by the MNC: 1. Adjusting fund flows: Altering either the amounts or the currencies of the planned cash flows of the parent or its subsidiaries to reduce the firm’s local currency accounting exposure. 66

MANAGING TRANSLATION EXPOSURE 2. Forward contracts Reducing a firm’s translation exposure by creating an offsetting asset or liability in the foreign currency. 67

MANAGING TRANSLATION EXPOSURE 3. Exposure netting a. Offsetting exposures in one currency with exposures in the same or another currency b. Gains and losses on the two currency positions will offset each other. 68

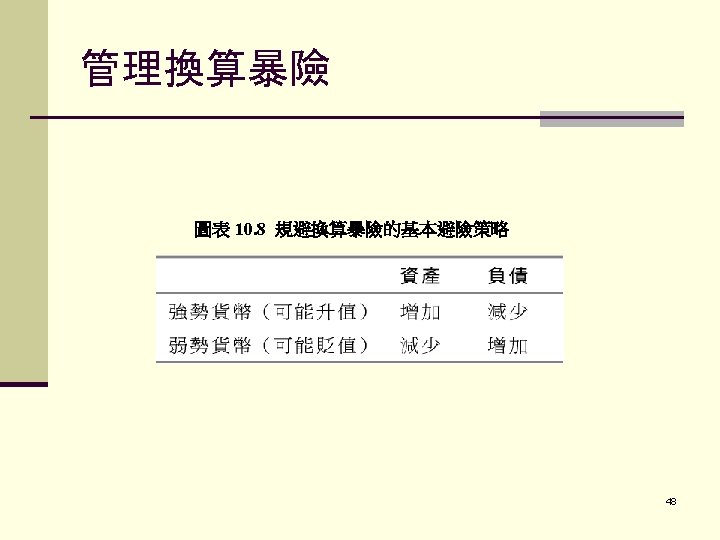

Managing Translation Exposure B. Basic hedging strategy for reducing translation exposure: 1. 2. 3. 4. Increasing hard-currency (likely to appreciate) assets. Decreasing soft-currency (likely to depreciate) assets. Decreasing hard-currency liabilities. Increasing soft-currency liabilities. 69

MANAGING TRANSLATION EXPOSURE How to increase soft-currency liabilities n n n Reduce the level of cash, Tighten credit terms to decrease accounts receivable, Increase LC borrowing, Delay accounts payable, and Sell the weak currency forward. 70