Financialisation of food opportunities or risks Myriam Vander

è Between 5 m $ to 500")

n Investment funds offered by banks and")

n Commodity exchange traded funds")

n Hegde funds n Pension funds e. g. PPGM (NL)")

")

n 200")

")

Price Chg % Market Capitalisation")

- Slides: 35

Financialisation of food: opportunities or risks? Myriam Vander Stichele, Senior Researcher SOMO (Centre for Research of Multinational Corporations) 5 November 2013 “Debating development”, University of Antwerp

OVERVIEW n Aim: show some particular interconnections between the food and financial sectors n Focus on : – farm land investments – food price speculation by financial players n Discussion on effects and what to do

WHAT IS FINANCIALISATION? n Strong interconnections food sector - financial sector n Objectives of financial profits & financial markets decisive for activities & strategies in the food chain, increasingly more than sustainable food production n Financial actors (banks, investment managers, institutional investors, etc. ) influence the food chain more than farmers and consumers n Risks? The Human Right to food vs. access to food based on prices, investments and financial players’ structures

INVESTMENT IN FARM LAND

Investment in farm land: when ‘land grab’? n Direct investment: e. g. by agribusinesses to produce farm products > needs! n Direct landgrab : – Abusive & Illegal buying of land by agribusinesses to produce for exports – When local farmers and customary users are dislocated without consent or compensation e. g. breach of human rights n Indirect investments and landgrab: e. g. – Put money into a local agro industrial complex, set up storage and crushing units, for export (farmers who deliver are locked into producing s for export) – Ownership versus rent, e. g. 99 year lease – Via domestic subsidiaries or shell companies, or go into a joint venture

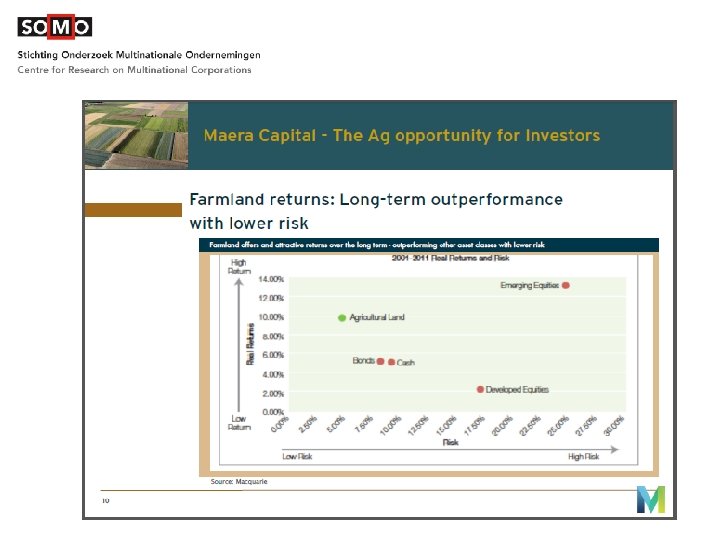

Financial players buy or renting land (1) è Between 5 m $ to 500 m $ n Investment managing companies e. g for pension funds (even more than 1 bn$), for wealthy families, for institutional investors such as universities, etc. n Hedge Funds: capital from institutional investors, agribusinesses, + borrrowing (up to 10 x capital) n Private Equity funds and venture capital funds e. g. Emergent African Agricultural Land Fund (since 2007): “target: returns of 20% per annum over seven years”

Financial players buy or renting land (2) n Investment funds offered by banks and investment management companies (e. g. for institutional investors to invest min. 1 m $) e. g. DWS Global Agricultural Land & Opportunities Fund Ltd (DWSGALO), issued by Deutsche Bank, incorporated in the Cayman Islands. n Asset management by insurance companies n Exchange traded funds (ETFs): shares can be bought by individuals on the stock exchange n Investment funds created specifically to purchase farm land to turn it to profitable production n Sovereign wealth funds

What strategies ? n Advertised as providing high returns (10%, even up to 35% vs. investment climate of low returns): marketing ! n High amounts of capital invested to buy or lease land n Profits : – not only from production – also from increase in land value n New investment strategy: ensure good production by investing in farms & land of good farmers who get a part of the profits

What challenges and risks? n Promises of high profits as primary objective (10%, even up to 35%) What if land becomes too expensive for local farmers? n Income and profits are not constant but depend on nature etc. What happens when profits are low and investors withdraw quickly? n How much do investors know or care about acquired land? Who is responsible if abusive land grabbing, HR & sustainability problems? n Too little information (transparency not sufficiently regulated): – sometimes based in tax havens or secrecy jurisdictions, – activities via subsidiaries – management for actual farming is being outsourced n Some investment companies also speculate on food prices

FINANCIAL FOOD PRICE SPECULATION

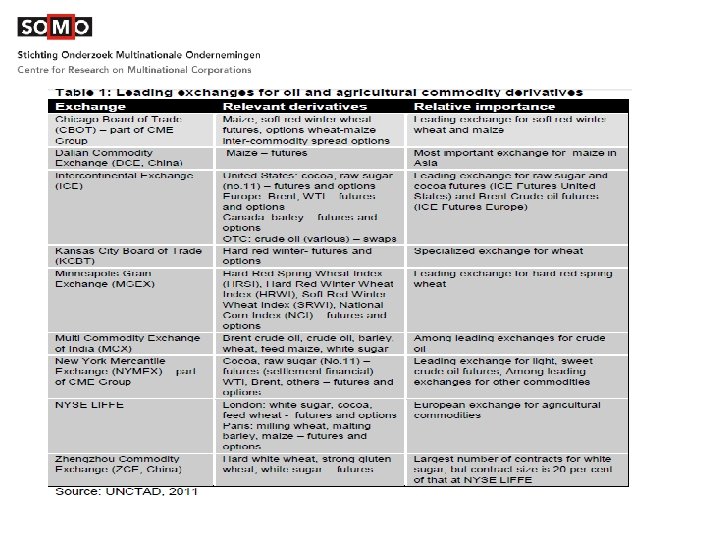

Using existing commodity futures and derivatives markets…

… for something else … diversifier for their portfolios. They also provide a hedge against inflation and political and business cycle risks. Also, what has “most investors view commodities as a caught the eye of most investors in recent years has been the double digit returns and the outperformance [of commodities] over equities and bonds. ” (Source: Senior fixed income specialist at Rabobank International, juni 2006) è“Speculation” vs. “hedging” food prices: regulatory definitions

Financial products n Commodity index funds (mixed/single «baskets» ) n Commodity exchange traded funds (ETFs) incl. « synthetic » n ETNs etc. : certificates n ( « Double » ) long/short turbo’s n OTC commodity derivatives/swaps: trading+hedging n New trends: – actively managed index funds, – new commodities in «basket» , – high frequency trading

Actors in financial markets and in politics n Investment banks e. g. the top five banks involved in food speculation – Barclays, Deutsche Bank, Goldman Sachs, JP Morgan and Morgan Stanley est. $3. 2 bn/EUR 2. 4 bn in 2010 -2012 n Banks e. g. in Belgium: BNP Paribas Fortis, Deutsche Bank (also: Axa, Belfius, ING, ABN Amro): offering 28 funds & commodity financial products, total sum invested in agricultural commodity derivatives ca. 950 m EUR Ø Profit making business: Ø fees for design, trading, counterparty, lending, clearing, advise, … Ø Over-the-counter derivatives market Ø Some trading on own account

Financial market actors (2) n Hegde funds n Pension funds e. g. PPGM (NL) part of EUR 9 bn ‘invested’ in ‘commodities’ n Institutional investors n Individual investors n High frequency traders n Agribusinesses speculating & hedging

Actors in financial markets and in politics : risks Acting based on financial (market) considerations and less based on knowledge of agricultural markets More money going into speculative financial instruments than in direct financing of farmers Ø Lobby for less regulation (1999/2000, 2009 -2013) e. g. ISDA prosecuting US financial regulators to weaken new laws (2012) Complexity and impact not clear to public & politics

Increasing capital flowing to speculative financial commodity products

Increasing food prices and food riots (2008) n 200

Fundamentals? n

Increasing number of speculative players Marktaandeel hedgers en speculators op de graan futures markt in Chicago (bron: Better Markets, CFTC)

Impact : Increasing volatility

Role of speculative players!? n No role, according to some banks & academics, commodity exchanges e. g. “no proof can be found” vs n Playing a role in volatility and price spikes according to some academici, UN Special Rapporteur on the Right to Food, G-20, NGOs, end-users, … e. g. n Paul Polman (CEO Unilever): “Speculation is pushing up food prices and threatening society's long-term interests. ” n George Soros, (fund manager): “Speculators create the bubble (…) which is especially true for commodities. It is like hoarding food in the midst of a famine, only to make a profit “ n FAO, IMF, World Bank, OECD e. a. , (May 2011) “While analysts argue about whether financial speculation has been a major factor, most agree that increased participation by non-commercial actors such as index funds, swap dealers and money managers in financial markets probably acted to amplify short term price swings and could have contributed to the formation of price bubbles in some situations. ” n Padraig Walshe (chair European farmers’ association Copa-Cogeca): “Prices should reflect the economic reality, not the excesses of speculators. The market should be regulated. ”

Commodity prices move in same way as other financial assets: no diversification?

Risks for developing countries n « Chicago » is an important price benchmark world wide n Importing countries: volatile and sometimes too high prices (also for food aid) n High prices = less (diversified) food intake, hunger in food importing countries (cities), general food price increase n Volatile prices: = producers unclear what to produce, wrong decisions/production = higher heding costs n Index funds can also increase/make volatile the price of inputs (oil: transport, fertilizers))

OTHER FINANCING INSTRUMENTS OF THE FOOD CHAIN

Financing the food chain & challenges Large companies (e. g. seed companies, agribusiness, retailers) access to: n Bank loans n Structured (trade) finance n Mergers & acquisitions (M&A) Ever larger companies vs. Small farmers, SMEs up to small retailers: little or expensive access to loans and financial services (e. g. DB in NL) Farmers dependent on financial services of commodity conglomerates (e. g. Cargill = a division is ‘swap dealer’)

Financial markets instruments & risks n Stock market and trading shares Focus on shareholder value, benchmarking, etc. n Mutual funds e. g. DWS Invest Global Agribusiness DS 5 (total assets: US$ 2, 477. 29; in 2013 so far: return of 8. 66% and 14% in 2012; sinception the fund has delivered a total growth of 31. 7%, and delivered. The fund’s 3 top holdings are; Mosaic [FERTILIZERphosphate] Co; Bunge Ltd [AGRI PRODUCTION AND TRADE]; and Potash Corporation [FERTILIZER] Larger corporations are able to use the pressure of buyer power for lower prices by smaller players in the food chain vs. sustainable agriculture

Example on Monsanto's website (d. d. 1 November 2013) Price Chg % Market Capitalisation Monsanto Company 105. 15 0. 26% 55. 29 B Syngenta AG (ADR) 80. 13 -0. 77% 36. 76 B The Dow Chemical. . . 38. 95 -1. 32% 47. 24 B E I Du Pont De Ne. . . 61. 09 -0. 18% 56. 58 B 123. 50 -0. 96% 102. 13 B 1. 48 1. 37% 36. 87 M 58. 79 0. 12% 3. 64 B 103. 54 -0. 35% 95. 10 B 1. 72 -1. 77% 39. 78 M FMC Corp 72. 82 0. 08% 9. 71 B Marrone Bio Innov. . . 16. 70 -3. 91% 316. 97 M Company name Bayer AG (ADR) Ceres Inc Scotts Miracle-Gr. . . BASF SE (ADR) Origin Agritech Ltd.

WHAT CAN BE DONE ?

n n n Regulation > political will > awareness raising Better data collection and publication (e. g. AMIS, Mi. FID) More research and academic debate Strategic commodity stocks Application of precautionary principle & Human Right to affordable food n Corporate Social Responsibility by financial industry, including on lobbying behaviour ! n Creation of regional and national exchanges in developing countries n Other price benchmarking and prince insurance mechanisms

Regulation at EU level: diffuse legislation !? !? n n n n Mi. FID II / Mi. FIR’’: position limits! MAR/MAD-II EMIR CRD-IV / CRR and other bank reforms UCITS VII? PRIPs Benchmarking/indices Related legislation: – Competition policy – FTAs and TISA, – … n Regulation to stop excessive lobbying !

Awareness raising: public and political debates

Thank you and more to read n http: //somo. nl/dossiers-en/sectors/financial/eu-financial-reforms n http: //www. makefinancework. org/home-english/food-speculation/ n http: //www. grain. org/article/entries/4479 -grain-releases-data-setwith-over-400 -global-land-grabs n ttp: //www. grain. org/article/entries/4655 -land-ceilings-reining-in-land -grabbers-or-dumbing-down-the-debate n http: //www. wdm. org. uk/food-speculation n http: //www. makefinancework. org/ (food speculation)