Seller Financing and Notes in The DoddFrank Era

OR three (3) properties in")

- Slides: 36

Seller Financing and Notes in The Dodd-Frank Era Stop Discounting Real Estate! Sell Fast with Unlimited Benefits and Maximum Sales Prices

Investor Presentation Phone: 480 -831 -5067 support@pinnacle-investments. com

The Bank of YOU! Be The Bank! The Bank Wins!

The Seller Finance Step by Step Process Agree on Terms & Sign Papers Buyer, Seller Agrees on Seller Financing Hire Pinnacle Investments Move into new Home Everyone Wins Seller Sells note for cash Make Monthly payments to Seller

Point of maximum risk in investment Euphoria Denial Excitement Optimism Fear Panic Hope Optimism Despondency Source: Westcourt Funds Depression Point of maximum opportunity

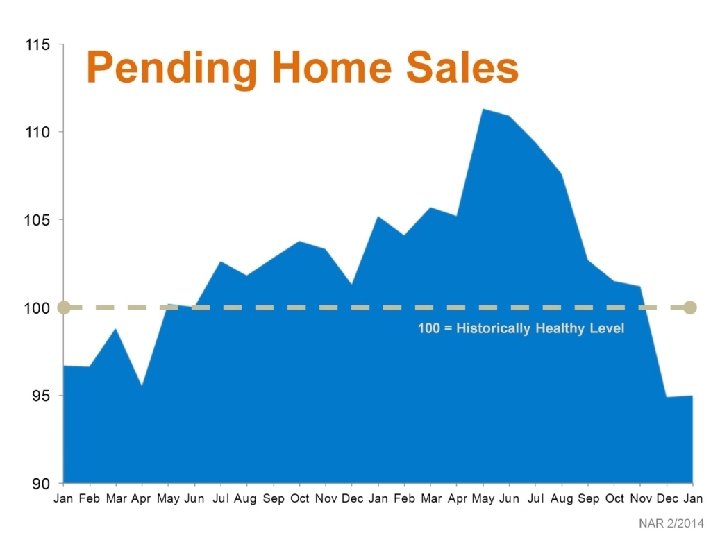

4 million renters want to buy. Can they? Diana Olick | @diana_olick Thursday, 13 Mar 2014 | 9: 03 AM ET CNBC. com Zillow : More Than 4 Million First-Time Buyers Want to Enter the Housing Market in 2014, Buoyed by Strong U. S. Housing Confidence 03/20/2014 | 11: 55 am US/Eastern Recommend: 0 Millions of renters say they really want to buy a home this year By Les Christie. March 13, 2014 4: 54 AM • More Than 4 Million First-Time Buyers Want to Enter the Housing Market in 2014, Buoyed by Strong U. S. Housing Confidence Homeownership Aspirations Among Current Renters Highest in Markets Hard-Hit by Housing Recession, According to Inaugural Zillow Housing Confidence Index

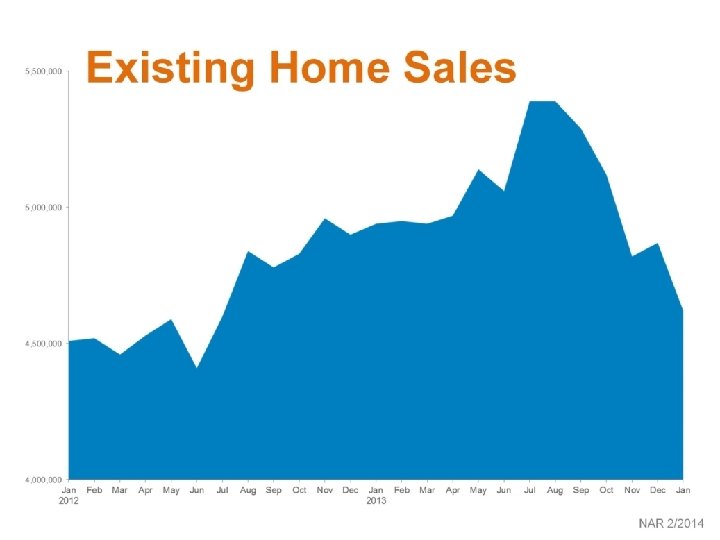

Americans Shut Out of Home Market Threaten Recovery: Mortgages By Prashant Gopal and John Gittelsohn Mar 5, 2014 7: 08 AM PT Demand for Mortgages Plummets, But It’s Not a Winter Storm, It’s More of an Ice Age Say Hello to the Lenders Recession March 7, 2014 Mortgage

Solution Always is Seller Financing • Seller Becomes the Bank • Money Exchanges Hands - Down Payment • Buyer Signs Promissory Note and Security Instrument • Remaining balance is carried as a loan

Seller Financing History 1970’s and 1980’s Seller Financed Transactions Dominated Market Seller Carry Market Cooled With Continued lower interest rates over 30 years and easy loans.

Seller Financing Today Tenuous Financial Markets Ever Tightening Number of Qualifying Buyer Pool Slipshod Appraisals Increases Flexibility Of Transactions Increase Yield Over Traditional Investments Avoidance of capital gains taxes

Regulatory Issue SAFE Act - 2008 Requires licensing for consumer credit transactions Licensee is mortgage loan originator Must register through Federal mortgage licensing system Sellers offering seller financing “may” need to be licensed Real estate brokers arranging a loan/ negotiating terms need a license

Dodd Frank Financial Reform Act - 2010 Disclosures required for sellers/brokers involved in certain seller financed deals Amends TILA to require disclosures for seller financed transactions Sellers have to meet very strict guidelines to be exempt from disclosure requirements Brokers have the same standards for exemption as the SAFE Act but must be careful with compensation

Exemptions SELLER FINANCE CONSUMER EXEMPTIONS UNDER DFA: One (1) OR three (3) properties in any 12 month period WHEN: (1)The seller is a natural person. (3) or, Corporation, LLC, partnership, trust, estate, etc. (1, 3) The seller did not construct the property (1, 3) The financing has a fixed rate and does not adjust for the first 5 years and No negative amortization (3) The borrower has a reasonable Ability To Repay the loan (3) No Balloon Payment ALL OTHER SCENARIOS REQUIRE A SFC MLO

Seller Financing Future Large Growing Market for Buyers With Less Than Perfect Credit After The Foreclosure Crisis Market Share Increases In Rising Interest Rate Environments Perfect For Properties Not Qualifying For Institutional Financing Retiring sellers need steady reliable income

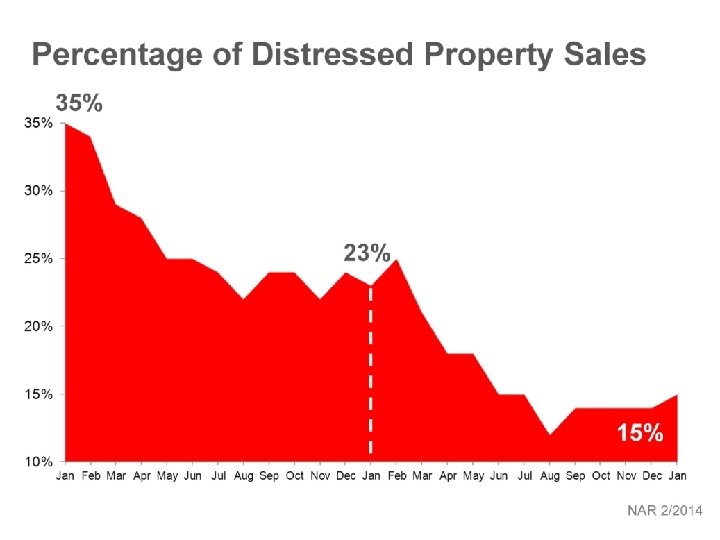

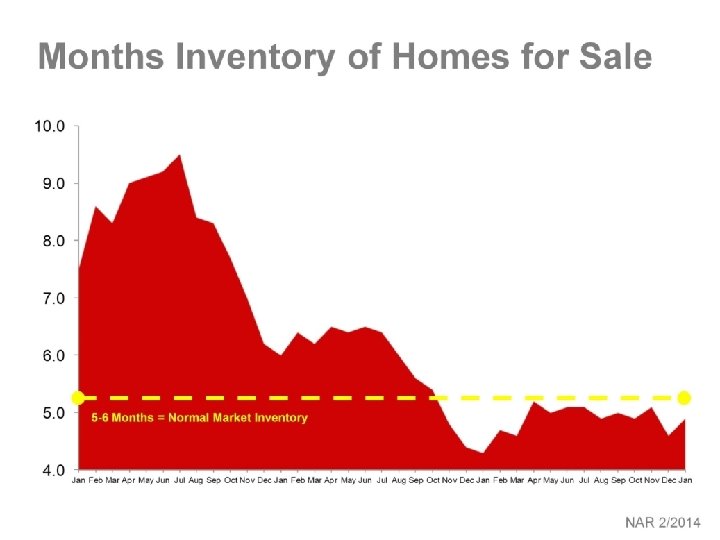

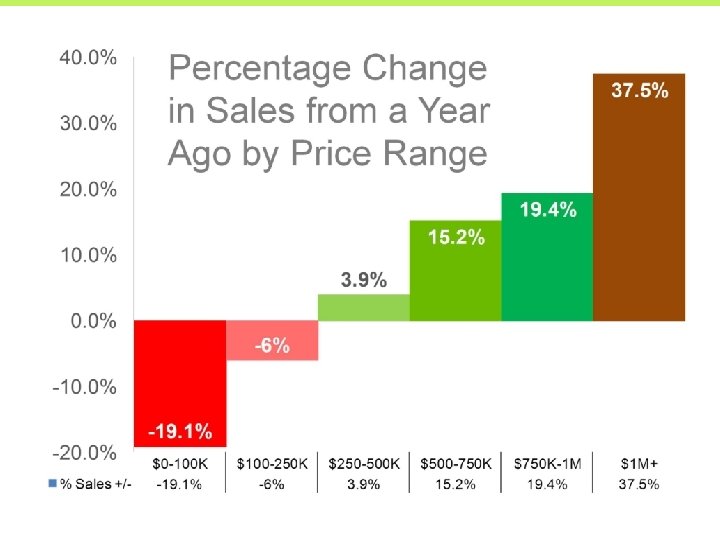

2010 California Transactions 2010 Sales Traditional ~230, 000 Seller Financed ~8, 200 REO ~80, 000 Short Sale ~100, 000 Data from 2010 NAR: Number of Seller Finance Transactions have already more tripled in less than 3 Years

Seller Financing Myths Only desperate people carry notes Only bad properties require seller financing “I need all cash at the closing so I can’t carry the loan” Only unqualified buyers want seller financing

Seller Financing Underwriting Require A Down Payment Check Credit Assure Regulatory Compliance Possibly Require A Personal Guarantee Document Pay History

Sellers Benefits Include Seller saves on closing costs, repair credits and fees Parties negotiate interest rate, repayment schedule, and other conditions of the loan Defers Keep capital gains taxes equity at work at interest rates higher than the bank is paying and more than historical appreciation rates

Seller Benefits Continued If the buyer stops paying, the Seller keeps everything and gets the property back If seller or heirs need money, they can sell all or part of the note for cash Fast Sale and Maximize the sales price by offering terms Adds liquidity to properties that don’t qualify for bank financing The property could be sold “as is” so there would be no need for repairs

Seller Financing Strategies 1. 2. 3. 4. 5. 6. 7. 8. AITD (Also Referred to as a “Wrap”) Title Holding Trust Stand Alone Second Land Contract Lease Option Lease Purchase Contract for Deed Purchase Subject To

Sample Note $420, 000 Purchase Price / Owner Occupied SFR 80% Note $336, 000 Face Amount 8. 22% Note Rate

Why? This Makes Sense For Borrower • The up front FHA insurance is 1. 75% • Loan origination is 1 -2% • Down payment is 3. 5% • That is a 6. 25 -7. 25 minimum investment in down payment on an FHA loan • On top of that there's a 1. 35% add to the rate over the life of the loan. • So if interest rates are 4. 5% the effective rate on • FHA will be 5. 85%

A Creative Solution Equals A Better, Safer, Smarter Sale: $2519. 94 in Monthly Income $139, 196. 40 in Total Income Over 60 Months Potential $40, 000+ Increase in Sales Price Potential Savings of $12, 000+ Property Repairs/ or Credits Potential Savings of $12, 000+ in Buyer Closing Cost Credits Potential Savings of 33. 33% in Capital Gains Taxes No More Taxes, Tenants, Termites or Toilets

Most Current Seller Financed Investor Deal

Repair Estimate for Bathroom Tiles: $1, 600 New roof: $16, 000 Dumpsters: $2, 500 Kitchen: $10, 000 Demo: $2, 000 Bathrooms: $12, 500 Doors: $1, 850 Ext Paint: $5, 500 Contingency: $4, 000 Stucco: $17, 000 Total: $97, 300 Landscaping: $3, 500 Int Paint: $6, 500 Int Texture: $4, 600 Elec Panel: $2, 500 Carpet: $3, 900 Wood Flooring: $3, 400

Maybe a Wholesale Deal on “Steroids” Consumer buyer offer $437, 500 / 30% down $306, 250 @8% 30/5 Listed Price $350, 000 Investor offer accepted by estate@ $350, 000

Buy and Hold or Flip: That is The Question New investor $350, 000 Flips to $437, 500 buyer 30% down Note for $306, 250 & $218, 750 in the deal Payment $2247. 15 60 month IRR 17. 40% Net $222, 320 12 Month IRR 44. 77% Net $114, 464 Sell the note 3 months 3 Month IRR 152. 59% @12% yield and make $84, 491

The Bank of YOU! Be The Bank! The Bank Wins!

The Seller Finance Step by Step Process Agree on Terms & Sign Papers Buyer, Seller Agrees on Seller Financing Hire Pinnacle Investments Move into new Home Everyone Wins Seller Sells note for cash Make Monthly payments to Seller