Personal Financial Management Seminar Office of Frank M

: Enjoy Refreshments!")

")

You are a targeted group. Your")

1 -888 -382 -1222 Who can still")

¢ Loan is yours even though you may")

")

¢ Payday loans, cash advance loans. ¢ Interest")

- Slides: 76

Personal Financial Management Seminar Office of Frank M. Pees Company Name Standing Chapter. Company 13 Trustee URL Address Debtor Education

Personal Financial Management ¢ Meets post-filing financial education requirement. ¢ Must show ID and sign-in and sign-out to receive certificate. ¢ Certificate will be emailed to your attorney. ¢ Attorney must file certificate with court. ¢ Seminars 2, 3, and 4 are voluntary.

Agenda for Seminars ¢ Seminar 1 – Financial Management - Monthly ¢ Seminar 2 – Basics of Budgeting – February, August ¢ Seminar – April, October ¢ Seminar – 3 – Buyer Beware 4 – Credit Re-establishment June, December

Materials ¢ Green – Folder Right side l Forms to complete l Personal Financial Choices workbook – Left side l Handouts ¢ Extra for Lessons 3 – 5 in workbook packet of forms/exercises for spouses in joint cases

Class Goals Setting goals and Creating a Plan Money Management/Budgeting (Break) : Enjoy Refreshments! Buyer Beware Restoring Your Credit Wise Use of Credit

Journey To Financial Success What does financial success mean to you? ¢ Enough money to take care of your needs. ¢ Enough money to pay for reasonable wants. ¢ Enough money to save for your goals.

Values ¢ What is really important to you? ¢ Activity 1 ---- Page 1 -2 List 5 things you want to do in your lifetime.

Philosophy of Money What Does Money Mean to You? ¢ Financial Security ¢ Bills ¢ College Education for Children ¢ Boat ¢ Home Improvements ¢ Gas/fuel ¢ Good Job

Money Messages ¢ What positive or negative messages about money did you hear from the important people in your life as you were growing up? ¢ What did they say about money----making it, spending it, saving it, etc? What did you “hear between the lines” about money? ¢ Their attitudes about money have influenced your attitudes and spending habits. ¢

Emotions and Money ¢ Anger ¢ Guilt ¢ Envy ¢ Depression ¢ Joy ¢ Loneliness and Boredom

Communication Timing is everything – choose a good time & talk about finances on a regular basis ¢ Make sure you know what you want to say before you start ¢ Let each person talk & Listen carefully: ”If you’re too busy talking, you’re not busy listening” ¢ Avoid jumping to conclusions or playing the blame game ¢ Focus on one topic at a time ¢

Exercises to Help Communicate About Money MONEY AND GOALS QUESTIONNAIRE ¢ Lesson 1, Page 1 -6 ¢ Answer the first 4 questions. PERSONALITY TYPES ¢ Page 1 -7

A Financial Plan Will Assist You In: ¢ learning how finances work in your life. ¢ making good decisions about money. ¢ making you aware of where your money is going. ¢ keeping good records of spending. ¢ improving communication with others.

A Financial Plan Will Assist You In: ¢ showing where to cut spending. ¢ providing way to save for specific items ¢ measuring your progress. ¢ living within your income. ¢ spending money without feeling guilty.

Four Steps in Planning Process Page 1 -10 Assess Needs 1. 2. Set Goals 3. Make A Plan 4. Take Action

Step 1 - Wants v. Needs VS

Step 2 - Set S. M. A. R. T. Goals Specific – clearly identify the goal. ¢ Measurable – have a yardstick ¢ for measuring outcome. ¢ Attainable – choose a realistic and reasonable goal. ¢ Relevant – must be important to you & consistent with other life plans. ¢ Time-related – set a definite date.

Step 3: Make a Plan Goal: Purchase a new lawn mower next June. 1. 2. 3. 4. Decide how much to spend. Research which model to buy. Compare prices at stores or online. Determine how much to save each week or month.

Step 4: Take Action 1. Bring my own coffee to work. (No Starbucks. ) 2. Use coupons at grocery store. 3. Set aside $XX. XX from each paycheck.

Realistic Goal with Action Steps Activity #8 – Page 1 -14 in workbook Write a goal – written goals are more likely to be achieved – Write a date by which you will accomplish it – List the steps you need to take to achieve your goal –

Skills needed to achieve goals ¢ 1 ¢ 2 ¢ 3 ¢ 4 ¢ 5 ¢ 6 ¢ 7 Focus – reminders or pictures Visualize achieving goal Set Priorities Manage Time Wisely Evaluate Progress Adjust Goals - if necessary Celebrate Success!

Keep On Keeping On. Persistence Usually Wins! Company Name Company URL Address

Lesson 2 $ Managing your Money $ Aka Budgeting

Components of a Budget Earning money Tracking money Categorizing expenses Subtracting expenses from income Analyzing and trimming expenses Saving money

Know Your Monthly Income Gross income – what you actually earn Net income – what’s left over after deductions for taxes, insurance, Chapter 13 payment, child support, etc. (what you actually get to spend)

Net Monthly Income Page 2 -2

Types of Expenses Examples Fixed Mortgage, Rent, Chapter 13 Payments, Support Variable Clothing, Food, Gas for auto, Utilities Periodic or Insurance (house, car) Unexpected Property/Income Taxes

GETTING STARTED Activity #2 in Lesson 2, page 2 -3 How much do you think you spend?

Track your spending Write down everything you spend every day for one month Do you know where your money actually goes?

Where does your money go? Write down every time money is spent, even on the smallest things.

Weekly Tracking Track weekly expenses Do this for 4 weeks Page 2 -6

Monthly Totals Page 2 -7 Total weekly expenses to get monthly totals

Create a personal spending plan page 2 -10 The first step is to see where you are so you can begin to make plans to get where you want to be.

Analyze and Trim Expenses Pack lunch for work or school Cancel extra cable services Use the public library for DVDs & magazines Food banks Dollar stores, secondhand clothing shops Use coupons and look for specials Plan meals weekly or monthly & build menus from what’s on special

Saving Your Money As soon as you receive your payment termination letter at the end of your case, start saving 5% - 10% of each & every paycheck from each & every wage-earner. Start a savings habit that continues for the rest of your working life. Pay yourself first. Use direct deposit if possible.

But, remember, as the country music singer says: Children spell LOVE: T-I-M-E It’s the time we spend with family & friends that matters most.

“It’s good to have money and the things that money can buy, but it’s good too, to make sure you haven’t lost the things that money can’t buy. ” George Horace Lorimer Editor, Saturday Evening Post 1899 -1937

Lesson 3 – Buyer Beware In the last 15 years a tremendous amount of research has gone into how to get people to buy. Targeted groups The Trustees’ Education Network included this chapter to help people protect their hard-earned money.

Marketing Tactics Ever go to the store for a loaf of bread and spend $30. 00? According to the experts Between 20% and 70% of all purchases are impulse or unplanned purchases Marketing experts have researched ways to increase unplanned purchases through: Color Atmosphere--- texture, sound and smell Advertising techniques

Color--- Influences Purchases Red ---Raises the blood pressure. Creates the feeling of excitement. It may cause us to be less rational. --Used in signs, brand labels and sale signs. Blue ---Send the message of trust and loyalty. --Used by many insurance companies, banks, medications or any product they want you to trust. Green ---Associated with money, wealth and nature. --Used by banks, investment firms, and companies associated with the outdoors. Black and Silver ---Used to sell luxury items. --Cars, computers and cell phones What do these background colors say?

Researchers have determined which colors appeal to what kind of person. http: //blog. kissmetrics. com/color-psychology/

Atmosphere Transition Zone---Just as you enter the store This zone is designed to separate us from the hustle and bustle of our lives. Makes us feel good and prepare us for the store’s promotions. If we are happy we will buy more. • Grocery stores use flowers and fresh bread. • There appealing smells there too. • Clothing stores use displays of enticing garments. Usually on the right side. • Research has gone into the type of music the store plays. • Uncarpeted isles in department stores are meant to lead you past certain merchandise. • Some department stores are using smell to increase the likelihood you will buy. • Food courts in malls and coffee and snacks in book stores are meant to get you to stay longer. The longer you stay, the more you will buy.

What are some of the advertising tricks that irritate you?

Advertising. Techniques Page 3 -2 and 3 -4 have more examples • Peer Approval----Implies if you do not use this product you will not be popular. • High Pressure---One day only. Quantities are limited. • Watch for Weasel Words---Words that practically nullify the claim they are supposed to be making. • "Leaves dishes virtually spotless. " Do you want your dishes almost clean? • “____ fights bad breath. " It fights it, but doesn’t stop it. • Bait and Switch---Store advertises something at a low price to get you in and then they try to get you to buy higher priced item. • Buy one and get one free ---The word free rings with people. However, would you buy the first one if the second wasn’t free? • Suggestive Selling ---More than we used to experience.

What hints can you give to avoid impulse buying.

Tricks to Avoid Impulse Buying • Smart shopping begins at home. Make a list. Stick to your list. See Sample Shopping List • • This saves on those $30. 00 loaves of bread. “Sleep on” major purchases. (Google complaints about products before you buy or check consumer reports. ) • Know your store. Go to the items you need and don’t browse. • Don’t use a cart or use the smallest one you can find. • If you use a cart, review your cart for items you might want to put back before you get in line. (Think about whether or not you really need the item. ) • Check the advertisements before you go. Try to build your week’s menu based on what is on sale.

Watch out for loss leaders— These items are sold at or below cost. The stores try to get you in the store hoping you will buy something else. hidden costs--Shipping and handling or batteries not included. deceptive packaging--Packages with more than one item grouped together. Sometimes they cost more than single ones. Same sized container, but one is 10 ounces and the other is 12. (We don’t buy 1 pound bags of chips or ½ gallons of ice cream any more. ) Comparison shop. (Many stores will price similar items-- one in pounds and one in ounces. They make it hard to compare —Take your calculator. )

Remember Impulse spending--- Leaves you further away from your goals. Ask yourself first: Is there something else I need to spend this money on? Have I already spent too much money on things like this? How disappointed will I be if I don’t buy this today?

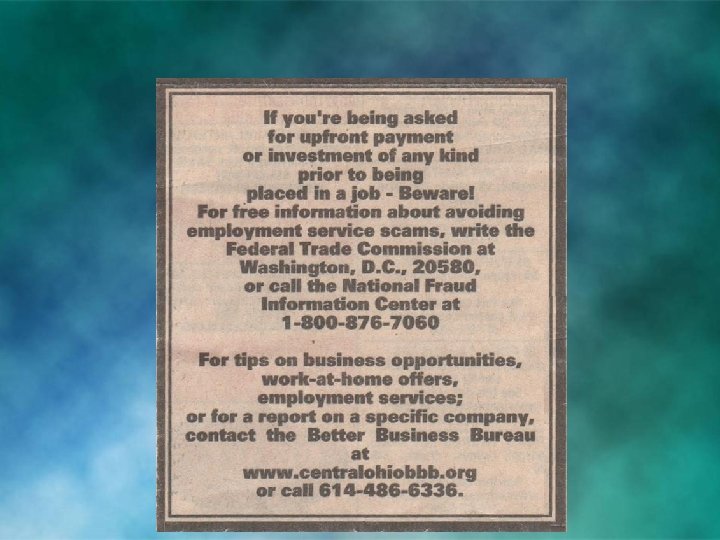

Consumer Protection Agencies to contact (handout page 2) You are a targeted group. Your information is a matter of public record. Better Business Bureau Call before you have work done or have complaints Chamber of Commerce (if no BBB in your city) Federal Trade Commission Fraud, deceptive, unfair business practices and identity theft. (Identity theft only takes a SS#. ) Food & Drug Administration For problems with foods, drugs and cosmetics Federal Communications Commission Misleading or deceptive ads on TV or radio Police to report con-artists or crooks going door-to-door State Attorney General US Post Office If you feel you’ve been defrauded through the mail for problems with items made, sold or advertised within the state.

DO NOT CALL list (handout page 3) 1 -888 -382 -1222 Who can still call: Charities Political parties Telephone surveys Any company you have existing relationship with • Includes contests you have entered • • or www. donotcall. gov What to do: • Ask the company to put you on their internal “do not call list. ” • If they are still calling after 30 days, report them.

UNSOLICITED EMAILS Forward unsolicited and phishing emails to: spam@uce. gov In Lesson 3, bottom of page 3 -8.

Work-at-home “opportunities” Be careful it is not a scam. Up to 80% are scams. Always in top 5% of all complaints BBB receives. If you have to pay money to make money, it is not a legitimate business opportunity. 77, 000 people paid $3 million to get involved assembling “refrigerator magnets” at home. They were told they could earn $800 per week in this business. To do that, of course, they’d have to assemble 20 magnets per hour for 40 hours per week for $1 per magnet. Since most of these refrigerator magnets don’t sell for over a couple bucks each, how did they think they could make more than the distributor and retailer combined?

Remember these tips for Smart Shopping – Don’t shop on payday. Have a spending plan and stick to it. If you must shop when you’re hungry, tired or in a hurry, buy only the things on your list. You don’t have to buy it today. Take a step back or sleep on it. The sales person is there to make money for themselves or the store, not save you money. Remember, _____ even if it is on sale, you will save more money if you don’t buy it.

Lesson 4 – Getting Your Credit Report – handout 4 www. annualcreditreport. com – only official website to get your no-cost reports ¢ 1 -877 -322 -8228 ¢ Use form to receive in mail (pages 5 & 6 of handouts in green folder) ¢ 3 national bureaus – Equifax – Trans. Union – Experian ¢ Free report does not include your credit score ¢

What Information is on Credit Reports? ¢ Identification and employment data ¢ Payment history ¢ Inquiries – Promotional inquiries – Hard inquiries ¢ Public Record Information – Bankruptcy 7 -10 years ¢ Address & phone number for bureau ¢ Information about your rights to correct errors and answers to common questions

Disputing Incorrect Information ¢ ¢ ¢ ¢ File disputes in writing, by form or letter or online Clearly identify the trade line and account number. Be specific about what action you expect and why. Send supporting documentation, if needed. Keep copies of what you send or who you speak with. Follow up with telephone call to number listed on report, if necessary. Credit bureaus must investigate your disputed information within 30 days. If creditor can’t verify their information is correct, it must be removed and a new report will be sent to you.

OPT-OUT -- handout page 3 1 -888 -567 -8688 www. optoutprescreen. co v. You may get “pre-approved” offers for credit cards or insurance. • “Pre-approved” only to receive offer not for the actual line of credit or insurance. • Credit cards are not to be used during bankruptcy. • Any non-emergency consumer debt of $1, 000. 00 or more must be approved by your Trustee or the Court. v The 888 number is an automated service. All you will need to opt-out is your Social Security number. v When you OPT-OUT, you are telling credit bureaus they cannot sell your information to a company for solicitations.

Credit Scoring ¢ ¢ Credit score at discharge depends on credit score when bankruptcy was filed. Credit scoring is done by computer. Gain points for positive info & lose points for negative info. Most creditors use FICO score: 300 -850. VANTAGE score is 501 -990 & uses letter grades, A to F. To calculate estimated FICO score from a VANTAGE score, multiply it by. 86.

To Rebuild Credit: ¢ ¢ ¢ ¢ FIRST STEP in credit re-establishment after discharge (before applying for new credit) is to check all three reports to make sure accounts have been updated and as much negative informative as possible has been deleted. Check your credit score after credit report is as good as can be. Open a savings account and make regular deposits, even if deposits are small. Make all payments on time, including utilities and medical bills. Get pre-approved for a loan before shopping for a major purchase. Save money and make a deposit for a secured credit card (after discharge. ) Keep charges below 50% of your credit limit.

Lesson 5 – Wise Use of Credit ¢ Credit spends your future income now. ¢ There is a difference between how much credit you can qualify for and how much you can afford. ¢ Don’t confuse being able to afford the minimum payment with being able to afford the entire debt amount.

Costs and Kinds of Credit ¢ Two things impact how much credit costs you: – – Interest rate charged Length of time to repay the loan Secured credit requires something to be promised as collateral. ¢ Unsecured credit is a loan without collateral. ¢ If you must use credit, be sure you use the type of credit that best meets your needs.

DANGERS OF COSIGNING (handout page 6) ¢ Loan is yours even though you may not benefit from the money or collateral. ¢ Cosigners are necessary if the borrower is not financially able to handle the debt. ¢ Loan may be in serious default before you are contacted and immediate payment is expected. ¢ Your paycheck is on the line.

Most Expensive Way of Financing Purchases ¢ Rent-to-own Contracts – (handout page 7)

Most Expensive Credit (handout page 8) ¢ Payday loans, cash advance loans. ¢ Interest is capped at 28% but interest rate is still 300% - 400%. ¢ Part of the problem, not part of solution. ¢ Do everything you can to stay away from these places. ¢ Once you get involved, it’s very hard to buy your way out.

Alternatives to payday loans Consider these short-term alternatives to borrowing money, but remember that selling goods and services, bartering, and renting out space may cause a taxable event. Become an Odd-Jobber (Be creative) If you have any skills, talents or hobbies, offer your services to your neighbors or friends for a fee. Sewing, mowing lawns, running errands, babysitting or walking the dog are examples. If you are good with crafts, check out Etsy. com as a way to market your goods. ¢ Learn to Barter If your crisis involves a car repair and you know a good mechanic, offer him a service in exchange for the repair. In other words, pay with a service instead of with cash. ¢

Alternatives to payday loans ¢ Sell Your Gently Used Items The internet is a great place to sell your gently used items. EBay and Craigslist are just two of many websites that make it easy to list and sell your items. ¢ Rent Out Space If you have an extra room in your house or you are not using your garage, think about renting the space for extra income. Make sure you carefully screen any applicant.

Alternatives to payday loans ¢ Cancel Services That You Do Not Need Limit yourself to necessary services until the crisis passes. For example, cancel premium cable channels, data packages on your cell phones and gym memberships. Be aware of cancellation charges prior to taking action. ¢ Selling Blood Plasma Some commercial blood banks pay up to $50 cash to blood/plasma donors per visit up to 4 donations a month. Remember, there could be some health risks for frequent donors, so ask your family physician about the risks prior to giving.

Alternatives to payday loans ¢ Seek help from public or private service agencies Check with the Salvation Army, the American Red Cross, the department for Human Services, Community Action Organizations, Traveler’s Aid, and other humanitarian organizations for assistance with rent, food, utilities, medical bills, prescriptions, and transportation needs. Religious organizations such as Lutheran Social Services, Catholic Social Services, or local churches in your area may have programs to help.

Alternatives to payday loans ¢ Other possible alternatives: If you are in the military, contact the Dept. of Defense at www. militaryonesource. com or call 1800 -342 -9647 or contact a Military Aid Society. ¢ As a last resort, and with your attorney’s help, you may consider requesting permission from your Chapter 13 Trustee to borrow against your life insurance policy if it has cash value, to borrow from your retirement plan if permitted by your employer, or to borrow from family or friends. Understand that loans not repaid as quickly as possible can lead to strife and discord.

Forms to complete & turn in before you leave today: ¢ Yellow Sign-out sheet ¢ Green – Evaluation form ¢ If you are in the last year of your Plan and would like to be part of a debtor panel to discuss your experiences with the Trustee, please indicate on the yellow sheet how we can get in touch with you.

Time for Review & Questions EVERYONE must turn in yellow sign-out sheet to receive certificate. ¢ Please turn in green evaluation form. ¢ You do not have to repeat this mandatory seminar even if you receive pink schedules in the mail. ¢ The Trustee invites you to the voluntary seminars (Budgeting, Buyer Beware, Credit Re-establishment. Schedules on table & website. ) ¢ Please return our pens. ¢ Thank you! Go Bucks! ¢