INTERNATIONAL CAPITAL FLOWS Thorvaldur Gylfason Joint Vienna InstituteIMF

")

")

is considered the most")

- Slides: 61

INTERNATIONAL CAPITAL FLOWS Thorvaldur Gylfason Joint Vienna Institute/IMF Institute August 24–September 4, 2009

OUTLINE 1. � 2. � 3. Foreign Trade in Goods and Capital Analytical framework Financial Globalization Recent Trends and Crises Recent Experience of Capital Account Liberalization

GOODS AND CAPITAL The case for free trade in goods and services applies also to capital Trade in capital helps countries to specialize according to comparative advantage, advantage exploit economies of scale, scale and promote competition Exporting securities – e. g. , equity in domestic firms – earns foreign exchange, and also grants access to capital, ideas, know-how, technology But financial capital is volatile 1

TRADE IN GOODS AND CAPITAL SIDE BY SIDE Balance of payments R = X – Z + Fx – F z = X – Z + F DR = change in foreign reserves X = exports of goods and services Z = imports of goods and services F = Fx – FZ = net exports of capital ü Foreign direct investment ü Portfolio investment ü Foreign borrowing

DETERMINANTS OF TRADE IN GOODS AND SERVICES Trade in goods and services depends on Relative prices at home and abroad Exchange rates (elasticity models) National incomes at home and abroad Geographical distance from trading partners (gravity models) Trade policy regime Tariffs and other barriers to trade

DETERMINANTS OF TRADE IN CAPITAL Again, capital flows consist of foreign borrowing, portfolio investment, and foreign direct investment (FDI) Trade in capital depends on Interest rates at home and abroad Exchange rate expectations Geographical distance from trading partners Capital account policy regime Capital controls and other barriers to free flows

RELEVANCE AND CONTEXT �Since 1945, trade in goods and services has been gradually liberalized (GATT, WTO) Big exception: Agricultural commodities �Since 1980 s, trade in capital has also been freed up Capital inflows (i. e. , foreign funds obtained by the domestic private and public sectors) have become a large source of financing for many emerging market economies

EVOLUTION OF CAPITAL FLOWS Capital mobility A stylized view of capital mobility 1860 -2000 First era of international financial integration Return toward financial integration Capital controls Source: Obstfeld & Taylor (2002), “Globalization and Capital Markets, ” NBER WP 8846.

CAPITAL FLOWS: FOR WHAT? Facilitate borrowing abroad to smooth consumption over time Dampen business cycles Reduce vulnerability to domestic economic disturbances Encourage saving, investment, and economic growth Increase welfare

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Real interest rate Emerging countries save a little Saving Investment Loanable funds

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Real interest rate Industrial countries save a lot Saving Investment Loanable funds

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Emerging countries Industrial countries Saving Real interest rate Financial globalization encourages investment in emerging countries and saving in industrial countries Borrowing Investment Loanable funds Lending Saving Investment Loanable funds

MIRROR IMAGE

PUSH VS. PULL FACTORS Capital flows result from interaction between supply and demand Capital is “pushed” pushed away from investor countries Investors supply capital to recipients Capital is “pulled” pulled into recipient countries Recipients demand capital from investors

PUSH FACTORS External factors “pushed” capital from industrial countries to LDCs Cyclical conditions in industrial countries § Recessions in early 1990 s § Decline in world interest rates Structural countries changes in industrial § Financial structure developments § Demographic changes

PUSH FACTORS Institutional investors, banks, and firms in mature markets increasingly invest in emerging markets assets to diversify and enhance risk-adjusted returns (i. e. , to reduce “home bias”), owing to Low interest rates at home, high liquidity in mature markets, stimulus from “yen” carry trade § Demographic changes, rise in pension funds in mature markets § Changes in accounting and regulatory environment allowing more diversification of assets §

PUSH FACTORS Institutional investors, banks, and firms in mature markets increasingly invest in emerging markets assets to diversify and enhance risk-adjusted returns (i. e. , to reduce “home bias”), owing to Sovereign wealth funds (e. g. , future generations funds) need to invest abroad as the domestic financial market is too small or too risky Need to invest the windfall gains accruing to commodity producers, in particular oil producers (e. g. , Norway)

PULL FACTORS Internal factors “pulled” capital into LDCs from industrial countries Macroeconomic fundamentals Reduction in barriers to capital flows Private risk-return characteristics § Creditworthiness § Productivity

PULL FACTORS Structural changes in emerging markets Better financial market infrastructure § Improved corporate and financial sector governance § More liberal regulations regarding foreign portfolio inflows § Stronger macroeconomic fundamentals Solid current account positions (except in emerging European countries) § Improved debt management § Large accumulation of reserve assets §

POTENTIAL BENEFITS OF CAPITAL FLOWS, AGAIN Improved allocation of global savings (allows capital to seek highest returns) Greater efficiency of investment More rapid economic growth Reduced macroeconomic volatility through risk diversification (which dampens business cycles) Income smoothing Consumption smoothing

POTENTIAL RISKS OF CAPITAL FLOWS Open capital accounts may make receiving countries vulnerable to foreign shocks Magnify domestic shocks and lead to contagion Limit effectiveness of domestic macroeconomic policy instruments Countries with open capital accounts are vulnerable to Shifts in market sentiment Reversals of capital inflows May lead to macroeconomic crisis Sudden reserve losses, exchange rate pressure Drastic balance of payments adjustment, with severe macroeconomic consequences Financial crisis

POTENTIAL RISKS OF CAPITAL FLOWS Overheating of the economy Excessive expansion of aggregate demand with inflation, real currency appreciation, widening current account deficit Increase in consumption and investment relative to GDP § Quality of investment suffers § Construction booms – count the cranes! Monetary consequences of capital inflows and accumulation of foreign exchange reserves depend on exchange regime § Fixed exchange rate: Inflation takes off § Flexible rate: Appreciation fuels spending boom

TOTAL CAPITAL INFLOWS (USD, BILLIONS)

FINANCIAL GLOBALIZATION: RECENT TRENDS AND CRISES �Global 2 cross-border asset and liabilities accumulation has risen dramatically over the past 15 years, reflecting Financial Globalization �Following relatively narrow fluctuations 1980– 95, global cross-border flows tripled to $6. 4 trillion, reaching almost 15% of world GDP by 2005 �Financial crises 1997 -98 and 2008 -09

NEW PEAKS: GROSS CAPITAL FLOWS 1980 -2005 (% OF WORLD GDP)

IN AND OUT: NET CAPITAL FLOWS

CONCENTRATION OF NET PRIVATE CAPITAL FLOWS TO SELECTED COUNTRIES, 1990 -2007 Source: IMF, World Economic Outlook database.

NET PRIVATE CAPITAL INFLOWS: ALL EMERGING MARKETS, 1990 -2007 Source: IMF, World Economic Outlook database.

Africa: Net Capital Flows 1980 -2008 Source: IMF WEO

Asia: Net Capital Flows 1980 -2008 Source: IMF WEO

Western Hemisphere: Net Capital Flows 1980 -2008 Source: IMF WEO

Middle East: Net Capital Flows 1980 -2008 Source: IMF WEO

TRENDS IN NET CAPITAL FLOWS TO EMERGING MARKETS �Emerging markets, as a group, have become net exporters of capital and an important investor class in mature markets �Emerging markets’ outflows mirror the U. S. external financing gap �The flow of capital from emerging to mature markets is channeled in large part through Asian central bank reserves and sovereign wealth funds

ON THE RISE FDI has become a dominant source of private capital flows to emerging market economies; equity flows have also risen in importance; debt flows have declined

REAL STOCK PRICES DURING INFLOW PERIODS: SELECTED COUNTRIES Chile 1978 -81 Mexico Venezuela Sweden Chile 1989 -94 Finland Year with respect to start of Inflow period Note: The Index for Finland, Mexico, and Sweden is shown on the left; the index for Chile during the 1980 s and 1990 s and for Venezuela is shown on the right. Source: World Bank (1997).

UP AND DOWN: STOCK PRICES IN THAILAND 1987 -2000

EPISODES OF LARGE NET PRIVATE CAPITAL INFLOWS: NUMBER, SIZE, AND ENDING Source: IMF WEO, Oct. 2007, Chapter 3, Table 3. 1.

EARLY WARNING SIGNS Large deficits Current account deficits Government budget deficits Poor bank regulation Government guarantees (implicit or explicit) Moral hazard Stock and composition of foreign debt Ratio of short-term liabilities to foreign reserves (Giudotti-Greenspan Rule) Rule Mismatches Maturity mismatches (borrowing short, lending long) Currency mismatches (borrowing in foreign currency, lending in domestic currency)

ASIA: RATIO OF SHORT-TERM LIABILITIES TO FOREIGN RESERVES IN 1997

LARGE REVERSALS

RECENT EXPERIENCE OF CAPITAL ACCOUNT LIBERALIZATION External or financial crisis followed capital account liberalization E. g. , 3 Mexico, Sweden, Turkey, Korea, Paraguay Response Rekindled support for capital controls Focus on sequencing of reforms Sequencing makes a difference Strengthen financial sector and prudential framework before removing capital account restrictions Remove restrictions on FDI inflows early Liberalize outflows after macroeconomic imbalances have been addressed

SOME TYPES OF CAPITAL FLOWS ARE RISKIER THAN OTHERS High degree of risk sharing No risk sharing Portfolio equity Foreign direct investment Short term debt Long term debt (bonds) Transitory Permanent

SEQUENCING OF CAPITAL ACCOUNT LIBERALIZATION Pre-conditions for liberalization Sound macroeconomic policies Strong domestic financial system Strong and autonomous central bank Timely, accurate, and comprehensive data disclosure

VOLATILITY OF CAPITAL FLOWS AND YIELDS �Capital flows exhibit volatility and a “boom-bust” pattern �The pattern reflects in part waves of privatization (FDI) and liberalization in emerging market economies �But it can at times reflect contagion effects from a financial crisis across markets

MARKET CLOSURES �High volatility episodes can be associated with temporary loss of access to capital markets and high yields on emerging markets bonds �The loss of access often reflects adverse political or economic developments in emerging market economies �The loss of access is sometimes linked to developments in mature markets (e. g. , tightening of liquidity)

EVOLUTION OF FDI IN CRISIS EPISODES �Foreign Direct Investment (FDI) is considered the most stable capital flow to emerging markets �Experience shows that FDI in general continued to grow through capital account crisis episodes

FINANCIAL CRISES IN 1990 S CALLED CAPITAL LIBERALIZATION IN DOUBT �Financial globalization is often blamed for crises in emerging markets �It was suggested that emerging markets had dismantled capital controls too hastily, leaving themselves vulnerable �More radically, some economists view unfettered capital flows as disruptive to global financial stability �These economists call for capital controls and other curbs on capital flows (e. g. , taxes) �Others argue that increased openness to capital flows has proved essential for countries seeking to rise from lower-income to middleincome status

ROLE OF CAPITAL CONTROLS �Capital controls aim to reduce risks associated with excessive inflows or outflows � Specific objectives may include �Protecting a fragile banking system �Avoiding quick reversals of short-term capital inflows following an adverse macroeconomic shock �Reducing currency appreciation when faced with large inflows �Stemming currency depreciation when faced with large outflows �Inducing a shift from shorter- to longerterm inflows

TYPES OF CAPITAL CONTROLS � Administrative �Outright controls bans, quantitative limits, approval procedures � Market-based �Dual or �Explicit controls multiple exchange rate systems taxation of external financial transactions �Indirect taxation E. g. , unremunerated reserve requirement � Distinction �Controls inflows between on inflows and controls on outflows on different categories of capital

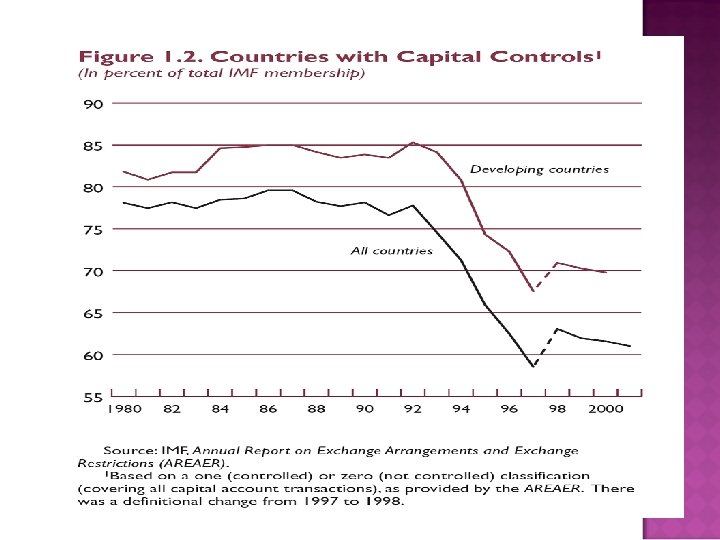

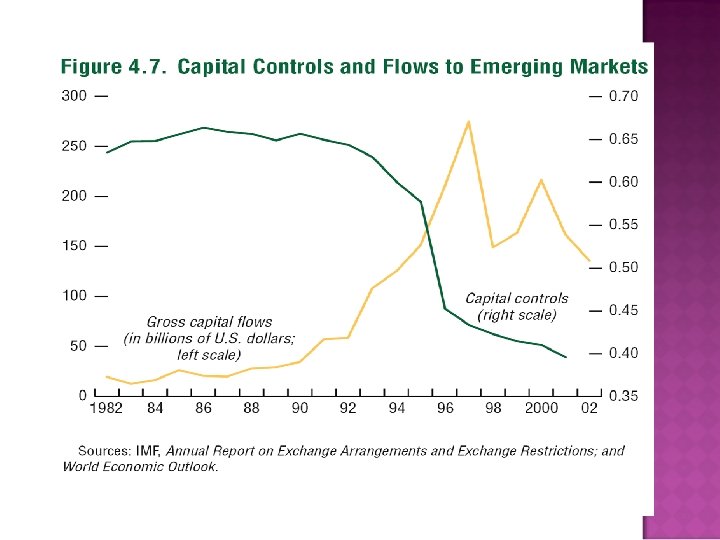

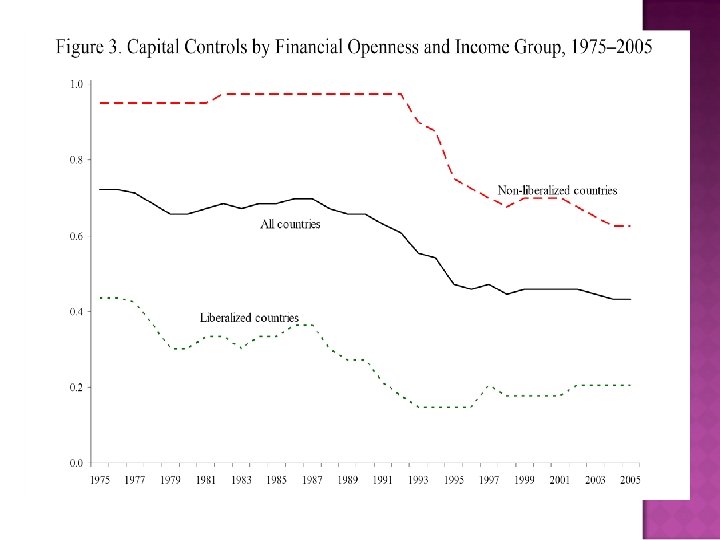

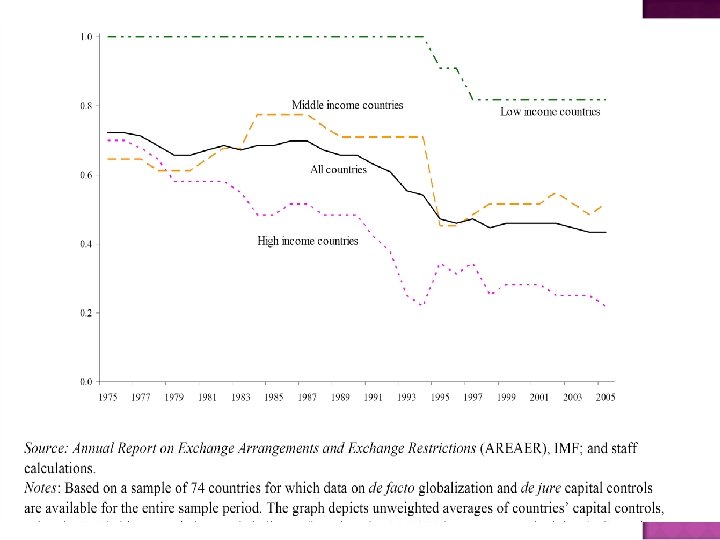

IMF ANNUAL REPORT ON EXCHANGE ARRANGEMENTS AND EXCHANGE RESTRICTIONS �IMF (which has jurisdiction over current account, not capital account, restrictions) maintains detailed compilation of member countries’ capital account restrictions �The information in the AREAER has been used to construct measures of financial openness based on a 1 (controlled) to 0 (liberalized) classification �They show a trend toward greater financial openness during the 1990 s �But these measures provide only rough indications because they do not measure the intensity or effectiveness of capital controls (de jure versus de facto measures)

CAPITAL CONTROLS: PROBLEMS �Implementation and circumvention �Controls distort behavior, as parties try to evade them �Controls reduce competition, and may promote cronyism �Higher capital costs, esp. for small firms �Controls may reduce FDI as well as other inflows �Hard to sustain controls over long periods �Investors learn how to evade them

CAPITAL CONTROLS: EFFECTIVENESS �There is some evidence that �Capital controls can help preserve some degree of monetary autonomy �Some countries have succeeded in using capital controls to alter the maturity of capital flows �There may be a case for imposing controls as an emergency measure during a limited period if the administrative capacity to manage controls is there �E. g. , Iceland 2008 �Market-based controls, such as unremunerated required reserves, are preferable to administrative measures

MOST OECD COUNTRIES LIBERALIZED GRADUALLY �In OECD countries, legacy of controls from 1930 s and from World War II took long to disappear �In France, it took until late 1980 s to abolish capital controls, and in the UK, capital controls were abandoned only in early 1980 s �It took long in part because of fear that any change in the system would be destabilizing �However, it was understood within the European common market and later EU that capital mobility was essential to economic integration

THE IMF'S ROLE �Since 1944, IMF has had full surveillance jurisdiction over the current account �IMF moved close to reaching an agreement in 1997 on an amendment to its Articles of Agreement giving the Fund full surveillance jurisdiction over the capital account as well �After Asian crisis, the move to amend the Articles weakened, and was shelved �IMF today follows an eclectic and integrated approach toward capital account liberalization, emphasizing proper sequencing and phasing combined with several concomitant reforms �IMF’s approach is flexible, recognizing specific country circumstances

CAPITAL ACCOUNT LIBERALIZATION AND FINANCIAL STABILITY �Experience has shown that a country with a poor macroeconomic situation, or a weak financial system, should not liberalize �It is necessary to create a reasonably stable banking and financial system before implementing a meaningful liberalization �As this takes a lot of time and effort, capital account liberalization should be gradual

CAPITAL ACCOUNT LIBERALIZATION AND FINANCIAL STABILITY Experience suggests Sequencing by type of capital flow by liberalizing … � � � Inflows before or at the same time as outflows Long-term capital flows before short-term flows FDI before portfolio investment Sequencing by sector by liberalizing … � � � First, the business sector, Second, individuals, Third, financial sector However, not easy to devise an operational plan that puts these principles in practice

CONCLUSION �Capital flows can play an important role in economic growth and development �But they can also create macroeconomic vulnerabilities �Recipient countries need to manage capital flows so as to avoid hazards �Need sound policies as well as effective institutions, including financial supervision, and good timing THE END