Exchangerate volatility exchangerate regime and trade volume evidence

- Slides: 10

Exchange-rate volatility, exchange-rate regime, and trade volume: evidence from the UK–US export function (1889– 1999) Kyriacos Aristotelous* 王成杰 10342272 國貿四乙

CONTENT 01 Introduction 04 02 Model Specification 05 03 Measure of variables and data sources Estimation procedure and empirical results Conclusions

INTRODUCTION ‣ this study investigates the impact of exchange-rate volatility and exchange- rate regime on the UK exports to the US for the period 1889– 1999 in the context of a generalised gravity model. ‣ The exchange-rate regime is included in the analysis as a determinant of trade volume on top of exchangerate volatility. ‣ Many exchange-rate regimes of the last 110 years are categorised into three types, namely, fixed exchangerate regime, managed-float exchange-rate regime, and freely-floating exchange-rate regime as suggested by Grilli and Kaminsky (1991).

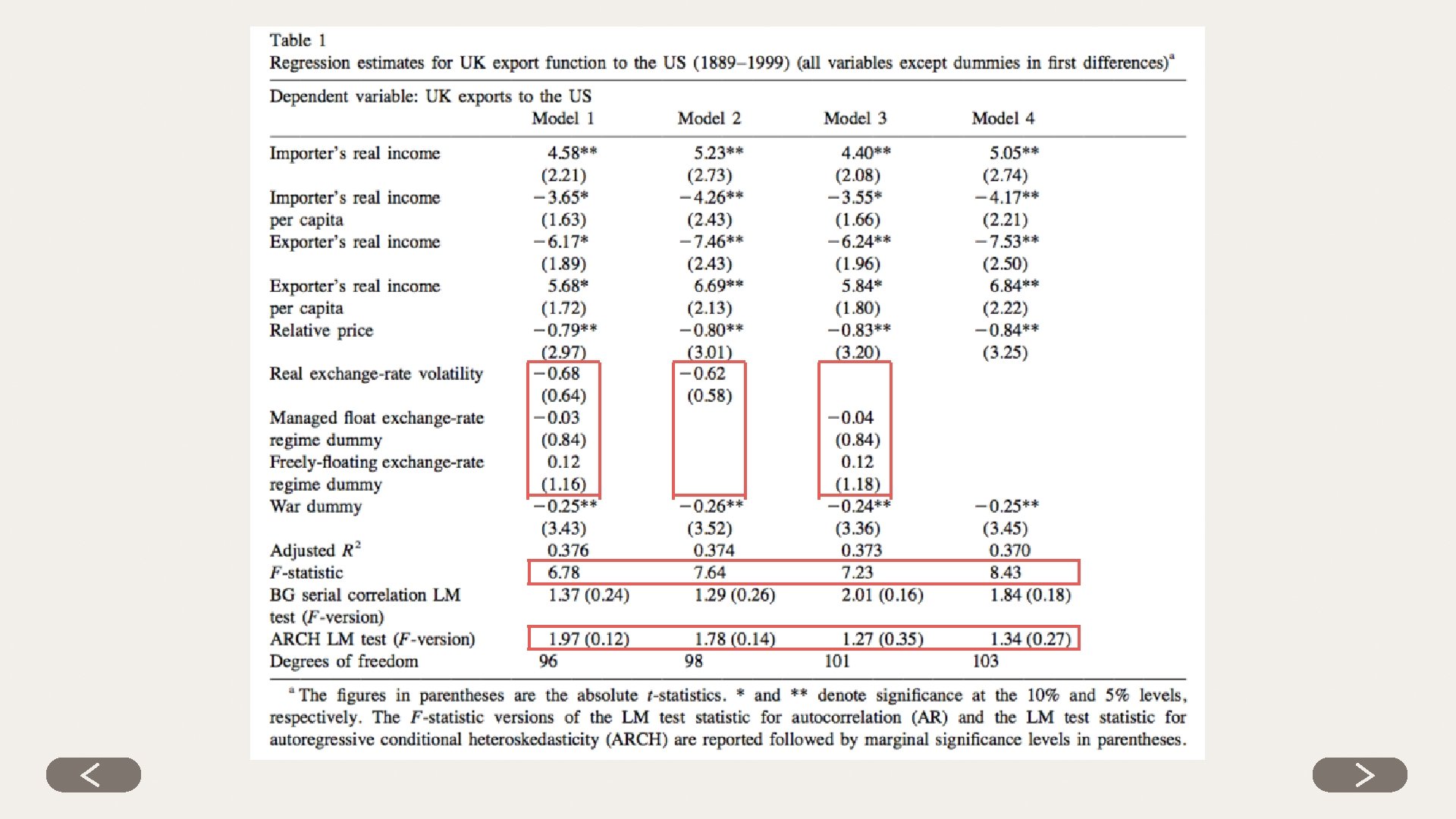

MODEL SPECIFICATION ‣ ln Xijt = β 0 + β 1 ln Yit + β 2 ln Yjt + β 3 ln yit + β 4 ln yjt + β 5 ln Pijt + β 6 Vijt + β 7 D 1 t + β 8 D 2 t + β 9 Wt + ℇt (1)

MEASUREMENT OF VARIABLES AND DATA SOURCES ‣ The moving S. D. of the growth of real effective exchange rate is used as a measure of time varying exchange-rate volatility in order to account for periods of high and low exchange-rate. ‣ Vt = [(1/m) m ] ∑ ( ln. Qt+i-1 - ln. Qt+i-2)2 1/2 i=1 (2)

ESTIMATION PROCEDURE AND EMPIRICAL RESULTS ‣ The order of integration of the individual time series was determined using the augmented Dickey - Fuller (ADF) and Phillips - Perron (PP) unit root tests. ‣ The results available upon request, indicate that all series are I(1) at a 5% significance level. ‣ Johansen likelihood approach among the variable in Equation(1).

CONCLUSIONS ‣Exchange rate volatility did not have an effect on the volume of British exports to the US. ‣There is no evidence that any of the exchange-rate regimes of the late 19 th and 20 th centuries had any impact on the volume of British exports to the US.

Thank You for Listening

Thank You for Listening