Drinking Water Resiliency with Water Audits Under IFA

Water Audits Water Audit Level 1 Validations")

passed - water utilities required complete annual water audits. Even-numbered")

Validity score total")

Wrong")

- Slides: 48

Drinking Water Resiliency with Water Audits Under IFA Michael Simpson CEO John H. Van Arsdel Vice President

A little history… Indiana Finance Authority (IFA) Water Audits Water Audit Level 1 Validations About Why-Fi Water (2106) Senate Enrolled Act No. 347 - all public water utilities in Indiana to provide the Indiana Finance Authority with a Non-Revenue Water IFA analyzed water infrastructure needs for all water utilities Report submitted to the legislative services agency/Indiana Legislature.

Why Fi 552 utilities were represented Senate enrolled Act 416: Infrastructure Assistance Fund passed into law (Public Law 233) April 28, 2017. Began evaluating regionalizing utilities to improve efficiency Assist utilities with future water auditing needs

SEA 4 (2019) passed - water utilities required complete annual water audits. Even-numbered year, starting in 2020, water audits required to be “validated” by a Certified, third party water audit validator, submitted to IFA for compilation into a biennial report to the General Assembly. IFA will aid utilities in completing validated water audits. IFA contracted with the Indiana Section of the American Water Works Association and its partners, providing training and assistance helping utilities meet the requirements of SEA 4.

Resiliency of IFA Program Classes started Fall 2019, scheduled to be completed by Spring 2020 COVID -19 happens and program gets a short delay while class and test formats get set up for Virtual online meetings Classes ended in July, 2020, and deadline for first set of Validated Audits extended to Jan 1, 2021. Review Class and Validation test added for Oct. 14 & 15, 2020 in French Lick, IN.

Gallons of water being pumped into the distribution system each billing period exceeds the gallons being sold. Where did it all go? ? Water Sold Water Pumped

How the Audit Works Water Supplied – Authorized Consumption = Water Loss Authorized Consumption = Billed Metered + Billed Unmetered + Unbilled Metered + Unbilled Unmetered Water Loss = Apparent Losses + Real Losses Each area has various components that can be analyzed (Thus the term: Component Analysis) Each area is examined in detail as part of the audit process

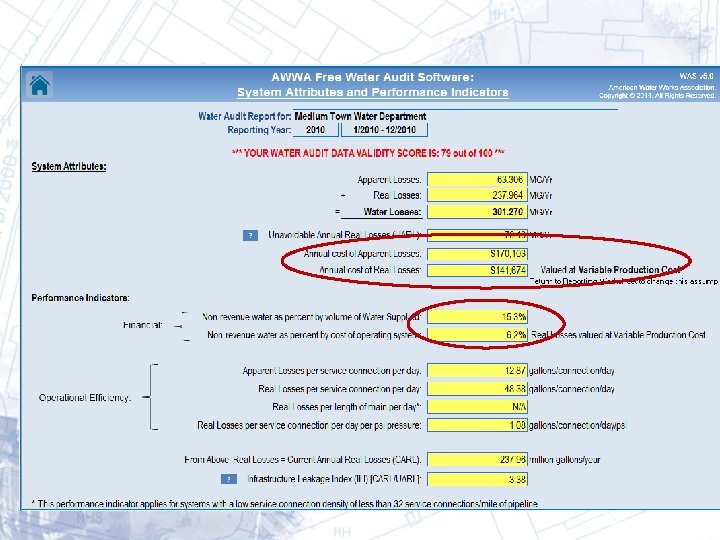

Water Audit Spreadsheet Water Supplied Authorized Consumption Water Losses Apparent Real Non-Revenue Water Cost Data System Data Validity Score Priority Areas for Attention

Grading each data input

How did the system do? Losses are totaled including Unavoidable Losses. Cost of losses are calculated.

How did the system do? Losses are normalized. Comparisons can be made year to year, water system to water system. ILI ratio calculated (UARL/CARL)

Start here Standard Water Balance Format Move this direction Water Exported Own Sources Total System Input Billed Water Exported Authorized Consumption Billed Metered Consumption Billed Unmetered Consumption Unbilled Authorized Consumption (allow Water ( allow for Supplied for known errors) errors ) Water Imported Billed Revenue Authorized Water Consumption Apparent Losses Water Losses Unbilled Metered Consumption Unbilled Unmetered Consumption Unauthorized Consumption Non. Revenue Customer Metering & Data Inaccuracies Water Leakage on Mains Real Losses Leakage on Service Lines (before the meter) Leakage & Overflows at Storage

Start here Move this direction

Completing the Water Audit Decide who will be in charge of the Audit for the Utility. Form a Committee. Input needed from: Water Production Billing Distribution GIS Engineering Proper input is needed from everyone to ensure success!

Develop an Audit Plan of Action Review Water Production Data Ø Meter error, meter setting issues, Water imported/exported Review Authorized water uses Ø Billed Metered, Billed Unmetered, Unbilled Metered, Unbilled Unmetered Review Apparent Loss inputs Ø Meter Error, Unauthorized Uses, Billing/Accounting errors Review Physical System Data Ø Miles of Main, Service connection count and average lengths, PSI averages Review Physical System Data Ø Total Operating cost, Average Customer Retail rate, Variable Production Costs Review Data Validity Grades (DVG’s) for each entry Review Performance Indicators

Areas where common errors occur Water Production Data Ø Tank level adjustments, offset MM reads, Imported/Exported Water, meter error Authorized Uses Ø All uses need proper accounting and proper characterizations Apparent Loss estimates Ø Composite customer meter error usually wrong System data and costs Ø Improper Counting of costs Data Validity Grade Assignments Ø (Be honest with assignments! Read descriptions) Performance Indicators Ø These are all calculated based on proper data inputs

Formulate a Strategic Plan for Water Loss Control Water Supply Ø Data issues (SCADA, Meter Reading data collection) Ø Field issues (Meter Accuracy, Meter Testing) Apparent Loss Recovery Ø Data issues (Billing/ Accounting) Ø Field issues (Meter accuracy issues, AMI/AMR issues)? Real Loss Recovery Ø Leakage issues Short Term Goals Ø Improve Audit data (will improve DVG’s) Ø Meter testing, leak detection, pipe condition assessments Long Term Goals AMR/AMI implementation Master Meter upgrades Main replacements

Water Supplied Data

How you finish your Audit is dependent on how you start your Audit so… if this is wrong… This will be wrong… too…

Is it possible to have a meter operate at 150% accuracy when the “certified report” says it is 99. 5% accurate? 8” Propeller Meter Well Pump Check Valve Distance too short Meter settings are very important for proper flow profile into the meter!!

Compared meter error from testing results to assumed error. ater W d e s i Rev input m e t s Sy -9. 62% versus -1%. How does this affect the Audit result? ater W l a n i Orig input m e t s Sy

Master meter tests can change Audit results! Original Water System input Revised Water System input This will change what the utility plans to do for loss remediation!!

Authorized consumption *Consumption and Billing review should be performed … *Unbilled Unmetered can enter an actual estimated amount used instead of the Default value to gain a higher DVG. Most utilities will use the default value.

Apparent Losses Original data used was an estimate Meter test data reviewed and consumption/billing data analyzed allowed for a more precise estimate.

System Data review…

UARL Explained Unavoidable Annual Real Losses “A theoretical reference value representing the technical low limit of leakage that could be achieved in all of today’s best technology could be applied to the water system” Leaks you may never find… *Background leakage that really cannot be found.

UARL Explained Accounting for differences in numbers… GIS data identified: § Private water mains § Shopping malls § Strip malls § HOA’s § Condo Associations § Community College campus *Any changes in theses numbers will affect the UARL

Consequences of unmetered private water mains Leaks can occur unnoticed on unmetered private mains. No incentive for owner to perform any pipe maintenance until the leak becomes huge and/or noticeable Utility absorbing costs of lost water A lot of water systems have these types of private mains! Includes Fire loops Gated neighborhoods Commercial/industrial sectors

ILI Explained ILI = Infrastructure Leakage Index It is the ratio of the CARL (Current Annual Real Loss) divided by the UARL ( Unavoidable Annual Real Loss) In theory the Index ratio cannot be lower than a “ 1” A “ 1” would indicate a perfect water system!

Interpreting the Grades: ILI

Data Validity Grade for each entry (little white boxes with numbers) Validity score total

Grading Matrix… lots of pages of grades

Apparent Losses Meter Error Composite How can this $$ loss be recovered?

“ 4 Pillars” of Apparent Loss Management NRW Management Team: ü Billing ü Meter Reading ü Customer Services ü Revenue Water ü Field Services ü System Development ü IT

Controlling Apparent Losses Measurement Technology Ø Accurate customer meters Ø Refined datalogging capability Ø Automatic Meter Reading gaining in use Improved Information Management Ø Customer Billing Systems Rational Policies Ø Service provision, Ø Unauthorized consumption Ø Billing procedures Ø Use of fire hydrants Meter equals Cash register

Reading and Billing AMR / AMI systems have changed the way meters are read Each Utility must choose a system which best compliments their strengths, based on man power and resources Consistency in billing is vital to ensuring that costly mistakes are not made and that liabilities are reduced

Data Handling Errors **Billing - What’s a Zero Among Friends? (nothing … really…) Wrong number of fixed zeroes Ø (Register programed incorrectly, manual read incorrect) Meters that are not being billed Ø Municipal accounts Accounts that are being billed as sewage or trash only and not as water

AMI Can Help Identify Non-Revenue Water Variable NRW level suggests source is meter error or theft Supply to system Controllable NRW constant level suggests source is leakage NRW Supply to system NRW Metered Usage

Meter Testing Program Meters must be periodically tested/repaired/retested for accuracy and the results documented Monitor meter test results, establish trends *helps the utility decide to perform a system wide replacement Test results show which meters are losing revenue To promote conservation, reduce water loss and use best management practices

Meter Change-out Approach Historical approach to meter replacement AWWA M 6 standard PSC requirements Run to failure – stopped meters are replaced Preventative – based on set age &/or consumption; systematically replaced Opportunistic – coordinate with AMR/AMI project

Real Losses ILI= CARL / UARL ILI= infrastructure Leakage Index

Unavoidable Annual Real Losses ELL: Economic Level of Leakage Reduce Pressure Add zones **Four ways to reduce leakage ! Pressure Management UARL: ELL Speed & Quality of Repairs Active Leak Control Program UARL Shorten Leak Surveys DMA’s response time Asset Management Recoverable Losses Maintain/ R&R infrastructure

Utility Challenges - Budgetary Programs needed to address challenges Ø Infrastructure replacement Ø Water quality and regulations Ø Workforce management Ø Source water – protection & security Ø Climate change Increasing debt service to pay for capital projects Increasing O&M expenses for energy, chemicals, staffing, etc. New rate structures to improve revenue stability & affect customer behavior

Resiliency Lessons learned from the Program Indiana water systems were a bit skeptical at first, but then embraced the program Systems realized that the Audit was a way to correct water loss and efficiency issues The Water Audit demonstrates where the water and financial losses were occurring Adjustments to the Audit were easily made when corrections were needed Future planning of water systems could make use of their data to allocate proper funds for improvements without overspending.

Resiliency Lessons learned from the Program Systems understood: Correct Data for the Audit needed to reach proper conclusions Funding for improvements was tied to the completion of the Audits (carrot on the stick) Level 1 Validations (3 rd party) provided a way to make sure data entry and Performance Indicators calculated from the data were correct Short term corrections were usually simple (data related) and not costly Long term corrections were now based on true revenue recovery from the Audit

Information to get started https: //www. awwa. org/Resources. Tools/Resource-Topics/Water-Loss-Control

Thank you!!