High Volatile Markets HARRV Fed Funds Rate Motivation

• BK (new) (Bank of New York")

98731. 66")

1499. 84")

11. 3")

1121. 1")

")

- Slides: 18

High Volatile Markets HAR-RV Fed Funds Rate

Motivation • Examine HAR-RV model differ in the financial sector data from 1997 compared to post July 2007 and post September 15 2008

Financial Sector Data • JPM (JP Morgan) • BK (new) (Bank of New York Mellon) • BAC (Bank of America) • AXP (American Express) • ALL (Allstate) Others Not Included Because of Data Differences

Financial Sector Data • Equally Weighted • Modify data so that stock splits do not affect the RV • Portfolio 1: 4/10/1997 through 1/7/2009 (1 share of each stock) • Portfolio 2: 4/10/1997 through 1/7/2009 (equally weighted)

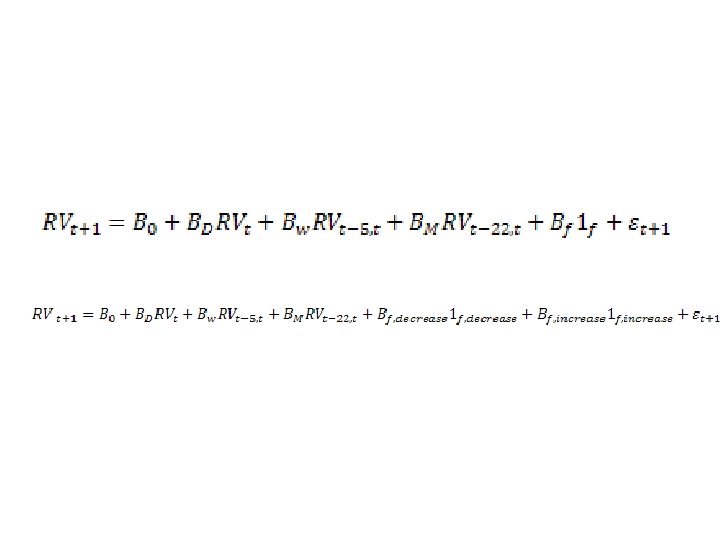

HAR-RV

Data Points From 1997 2900 Post July 2007 356 Post Sept 15 2008 76

HAR-RV: Full Data Robust regression Number of obs 2895 F( 3, 2891) 98731. 66 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 3082 0. 002 154. 970 0. 000 0. 304 0. 312 v 3. 1525 0. 001 122. 480 0. 000 0. 155 v 4. 0289 0. 001 54. 390 0. 000 0. 028 0. 030 _cons. 0001 0. 000 11. 090 0. 000

HAR-RV

HAR-RV: Financial Crisis Robust regression Number of obs 355 F( 3, 351) 1499. 84 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 4904 0. 014 34. 840 0. 000 0. 463 0. 518 v 3. 1024 0. 009 11. 600 0. 085 0. 120 v 4 -. 0017 0. 004 -0. 420 0. 675 -0. 010 0. 006 _cons. 0012 0. 000 4. 700 0. 001 0. 002

HAR-RV Prediction Finance

HAR-RV: Post Lehman Robust regression Number of obs 75 F( 3, 71) 11. 3 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 3054 0. 065 4. 690 0. 000 0. 175 0. 435 v 3. 0212 0. 039 0. 540 0. 591 -0. 057 0. 099 v 4. 0039 0. 031 0. 120 0. 901 -0. 058 0. 065 _cons. 0120 0. 006 1. 980 0. 052 0. 000 0. 024

HAR-RV with Fed Factor: Full Data Robust regression v 1 Coef. v 2. 3079 v 3. 1528 v 4. 0289 v 5. 0001 _cons. 0001 Number of obs F( 4, 2890) Prob > F Std. Err. 0. 002 0. 001 0. 0000719 0. 0000102 t P>t 154. 440 122. 570 54. 400 1. 14 10. 89 0. 000 0. 256 0 [95% Conf. 0. 304 0. 150 0. 028 -0. 0000593 0. 0000912 2895 74118. 55 0 Interval] 0. 312 0. 155 0. 030 0. 0002225 0. 0001

HAR-RV with Fed Robust regression Number of obs 355 F( 4, 350) 1121. 1 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 4932 0. 014 34. 500 0. 000 0. 465 0. 521 v 3. 1026 0. 009 11. 550 0. 000 0. 085 0. 120 v 4 -. 0021 0. 004 -0. 490 0. 622 -0. 010 0. 006 v 5 -. 0003 0. 001 -0. 270 0. 785 -0. 003 0. 002 _cons. 0012 0. 000 4. 670 0. 001 0. 002

HAR-RV with Fed: Post Lehman Robust regression Number of obs 76 F( 4, 71) 13. 57 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 2931 0. 053 5. 490 0. 000 0. 187 0. 400 v 3. 0275 0. 041 0. 680 0. 499 -0. 053 0. 108 v 4. 0020 0. 032 0. 060 0. 949 -0. 062 0. 066 v 5. 0042 0. 010 0. 430 0. 668 -0. 015 0. 024 _cons. 0121 0. 006 2. 020 0. 048 0. 000 0. 024

HAR-RV with Fed Direction Changes: Full Data Set Robust regression Number of obs 2896 F( 5, 2890) 63084. 36 Prob > F Std. Err. t P>t 0 v 1 Coef. [95% Conf. Interval] v 2 . 3079 0. 002 153. 830 0. 000 0. 304 0. 312 v 3. 1524 0. 001 123. 990 0. 000 0. 155 v 4. 0290 0. 0005305 54. 67 0 0. 0279631 0. 0300435 v 6. 0002 0. 000099 2. 25 0. 024 0. 0000287 0. 0004169 v 7. 00002 0. 0001043 0. 18 0. 859 -0. 0001859 0. 000223 _cons. 0001118 0. 0000102 10. 94 0 0. 0000917 0. 0001318

HAR-RV with Fed Direction: Financial Crisis Robust regression Number of obs 355 F( 4, 350) 1121. 1 Prob > F v 1 Coef. Std. Err. t P>t 0 [95% Conf. Interval] v 2. 4932 0. 014 34. 500 0. 000 0. 465 0. 521 v 3. 1026 0. 009 11. 550 0. 000 0. 085 0. 120 v 4 -. 0021 0. 004 -0. 490 0. 622 -0. 010 0. 006 v 6 -. 0003 0. 001 -0. 270 0. 785 -0. 003 0. 002 0. 000 4. 670 0. 001 0. 002 v 7 (dropped) _cons. 0012347

HAR-RV with Fed Direction: Post Lehman Robust regression v 1 Coef. v 2. 2931 v 3. 0275 v 4. 0020 v 6. 0042 v 7 (dropped) _cons. 0121 Number of obs F( 4, 71) Prob > F Std. Err. t P>t [95% Conf. 76 13. 57 0 Interval] 0. 053 0. 041 0. 032 0. 010 5. 490 0. 680 0. 060 0. 430 0. 000 0. 499 0. 949 0. 668 0. 187 -0. 053 -0. 062 -0. 015 0. 400 0. 108 0. 066 0. 024 0. 006 2. 020 0. 048 0. 000 0. 024