25 years in the postsocialist economies John Grahl

On average, income per capita has")

")

")

• Emerging Europe had a difficult time in")

Ukraine, locked in sectarian strife in the eastern")

As negotiations between Kiev and its creditors stall and")

Spot the difference in sentiment. In March a presentation")

- Slides: 38

25 years in the post-socialist economies. John Grahl Middlesex University Presentation to the workshop on conflict in post-socialist countries

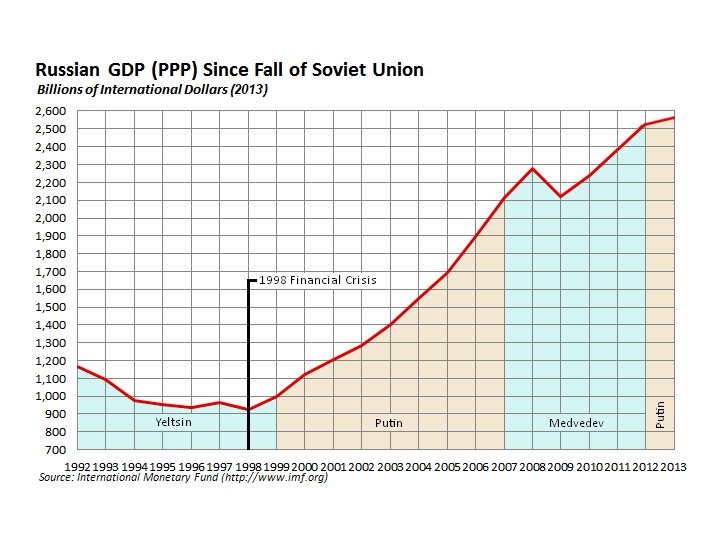

Main Source: IMF, “ 25 years of transition : post-communist Europe” A questionable judgement: “Countries that took bolder and more frontloaded reforms—notably in Central Europe and then the Baltics—were rewarded with a faster return to growth and stability, including avoiding the series of crises that hit the region in 1997 and 1998. ”

Alternative View • The real distinction is in the relationship to the EU and Germany • The crisis of 1998 was induced by the guys in the burberry macs • 1998 marked a decisive move away from neoliberalism and the beginning of recovery in the Russian Federation

Post-socialist states in Europe

Some weaknesses • • • Limited convergence Energy Dependence Recent decline in growth potential? Loss of financial autonomy? Convergence itself?

Limited convergence of post-socialist economies in Europe (1) On average, income per capita has risen from about 30 percent of EU 15 levels in the mid 1990 s to around 50 percent today. This average conceals large differences between countries, with some, such as the Baltics, making huge advances; and others, such as Bosnia and Herzegovina, Moldova, and Ukraine, getting increasingly left behind.

Limited convergence of post-socialist economies in Europe (2)

Energy Dependence: Exports

Energy Dependence : Imports

Potential Growth Slowdown

Factors in the slowdown

Demographic decline

The villainy you teach me I will execute….

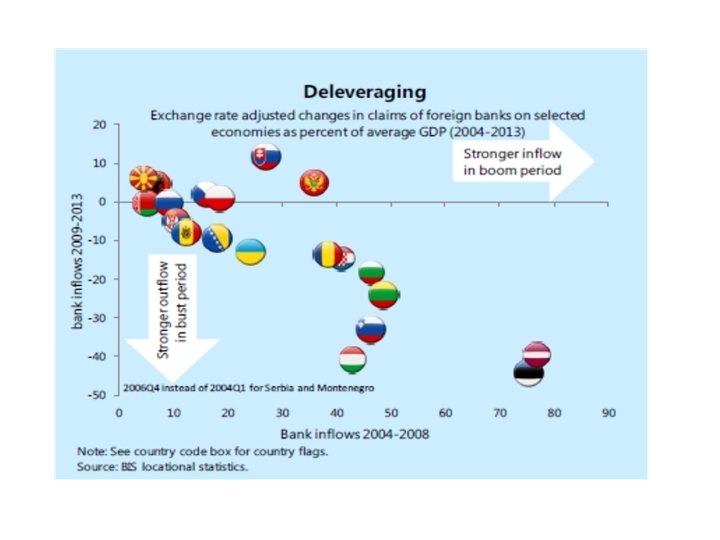

Financial penetration

Financial penetration • What happens when these banks have to shed assets?

Financial penetration • What happens when these banks have to shed assets?

Reforms…. . • There is no end to reforms. If they don’t work that only shows that you haven’t reformed enough

Privatisation: Belarus behind (but note also Poland)

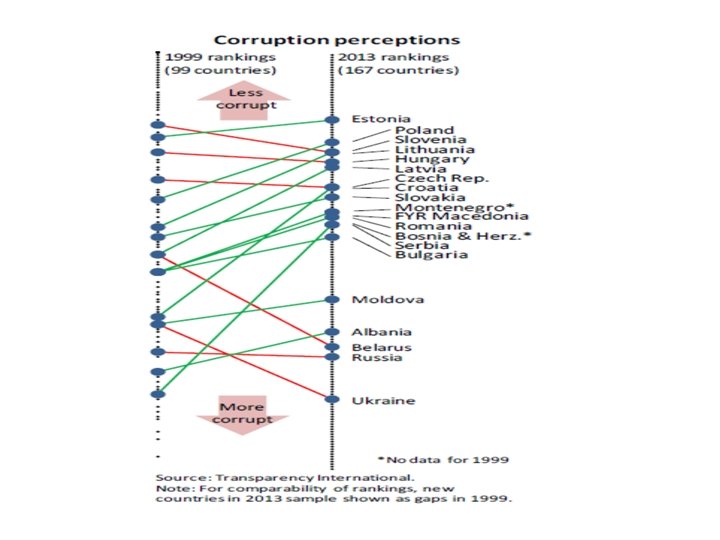

The least “reformed” countries….

…have the lowest unemployment

Reforms: Les mauvais élèves: Belarus, Serbia, Bosnia

Transition is bad for equality

IMF on the transition: welcome to the global economy In contrast to the turbulence and divergence of the 1990 s, growth patterns in the early and mid-2000 s were uniformly strong…. However. . . growth in this period became increasingly imbalanced. . . The resulting vulnerabilities combined with the effects of the global financial crisis with devastating effect: output declines in 2009 averaged 6 percent and ranged up to 18 percent, a more severe impact than in any other region of the world.

Unemployment rises in the crisis

IMF support programmes- much bigger in the global crisis

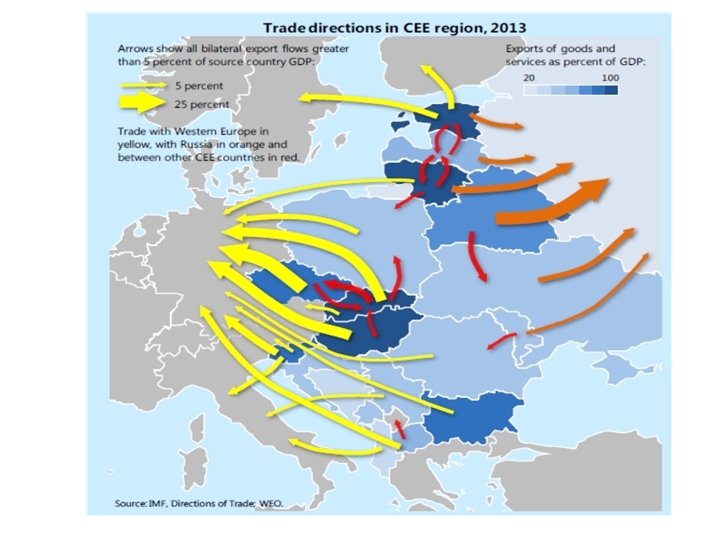

The Real Bifurcation? • Integration into German supply chains?

Hungary, Poland, Slovakia, Czech Republic, Lithuania - big rise in export shares

Some data on Ukraine, economic consequences of conflict Projected % Change 2015 Real GDP -5. 5 Consumer Prices 33. 5 2016 2. 0 10. 6 Source: World Economic Outlook (April 2015)

Impact of the Conflict The Eastern regions affected by the conflict comprise a non-negligible part of the economy. In 2012, the regions of Donetsk and Luhansk accounted for 15¾ percent of Ukraine’s GDP. In 2014: Q 1 their share in Ukraine’s volume of industrial production amounted to 23 percent and 14½ percent in retail trade. In addition, 23 percent of total exports of goods and 6¾ percent of total goods imports were associated with the two regions.

Growth Rates of Tax Revenue in the East (Percent; June 2014 relative to June 2013)

Ukraine - fall in FDI (1) • Emerging Europe had a difficult time in 2014, with a dearth of outbound investments from Russia impacting negatively on investment levels across central, eastern and southeastern Europe and the CIS markets. FDI into Russia itself took a plunge with a 39 per cent decrease in project numbers, although large investments by a handful of Chinese investors kept capital investment levels at an estimated $12 bn.

Ukraine - fall in FDI (2) Ukraine, locked in sectarian strife in the eastern part of the country and teetering on the brink of war with Russia, saw capital investment drop by 80 per cent and projects by 64 per cent.

Ukraine moves towards default (1) As negotiations between Kiev and its creditors stall and full-blown bankruptcy nears, the rhetoric of government communiques is shifting from conciliation to accusation. (FT website 27/05/15)

Ukraine moves towards default (2) Spot the difference in sentiment. In March a presentation to investors noted that “a collaborative process is paramount. . . Ukraine is committed to undertake consultations with its creditors”. By May the government declared it “has the right. . . not to return loans borrowed by the kleptocratic regime of Yanukovych”.