Valuing shares earnings and dividends Corporate Finance 33

Source: Pearson plc, Annual Review 2006.")

model Current market price of share 200 p Historic PER")

stock markets, 1964– 2007")

- Slides: 26

Valuing shares, earnings and dividends Corporate Finance 33

Valuing shares: assets, dividends and earnings • The principal determinants of share prices • Estimate share value using a variety of approaches • The most important input factors • Net asset valuation • Dividend valuation models • Price earning ratio models

Share valuation: the challenge • Two skills are needed to be able to value shares: 1 Analytical ability, to be able to understand use mathematical valuation models 2 Good judgement is needed • Assets such as cars and houses are difficult enough to degree of accuracy value with any • Corporate bonds generally have a regular cash flow an anticipated capital repayment (coupon) and • With shares there is no guaranteed annual payment and capital repayment no promise of

Valuation using net asset value (NAV) Source: Pearson plc, Annual Review 2006.

Net asset values and total capitalisation of some firms Source: Annual reports and accounts; www. advfn. com 7. 5. 07.

What creates value for shareholders?

When asset values are particularly useful • Firms in financial difficulty • Takeover bids • When discounted income flow techniques are difficult to – 1 Property investment companies – 2 Investment trusts – 3 Resource-based companies apply

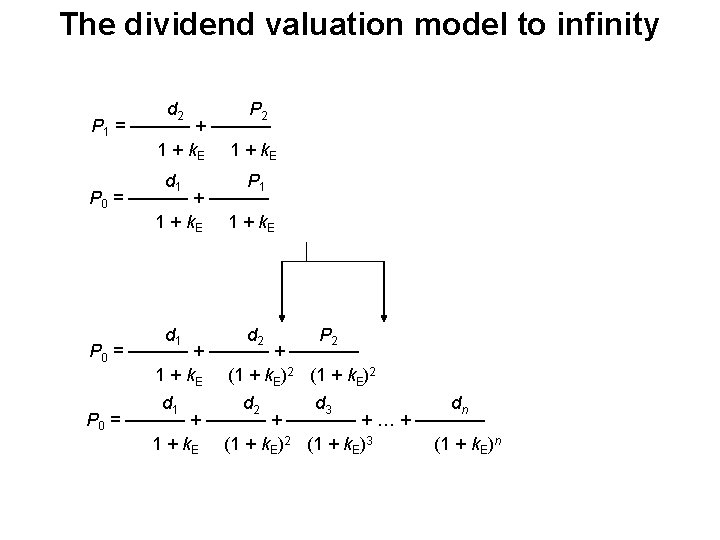

The dividend valuation models • The market value of ordinary shares represents the sum of the expected future dividend flows, to infinity, discounted to present value • The only cash flows that investors ever receive from a company are dividends. • An individual holder of shares will expect two types of return: – (a) income from dividends – (b) a capital gain d 1 P 0 = –––––– + –––––– 1 + k. E

Worked example • At the end of one year a dividend of 22 p will be paid and expected to be sold for £ 2. 43 • The rate of return required on a financial security of this 20 per cent. d 1 P 0 = –––––– + –––––– 1 + k. E 22 243 P 0 = –––––– + –––––– = 221 p 1 + 0. 2 the shares are risk class is

Worked example • If a firm is expected to pay dividends of 20 p per year to infinity and the rate of return required on a share of this risk class is 12 per cent then: 20 20 P 0 = –––––– + –––––––– + … + ––––––– 1 + 0. 12 (1 + 0. 12)3 (1 + 0. 12)n P 0 = 17. 86 + 15. 94 + 14. 24 +. . . + Given this is a perpetuity there is a simpler approach: d 1 20 P 0 = –––––– = 166. 67 p k. E 0. 12

The dividend growth model • If the last dividend paid was d 0 and the next is due in one year, d 1, then this will amount to d 0 (1 + g). Shhh plc has just paid a dividend of 10 p and the growth rate is 7 per cent then: d 1 will equal d 0 (1 + g) = 10 (1 + 0. 07) = 10. 7 p d 2 will be d 0 (1 + g)2 = 10 (1 + 0. 07)2 = 11. 45 p d 0 (1 + g)2 d 0 (1 + g)3 d 0 (1 + g)n P 0 = ––––––-- + –––––––– + … + –––– (1 + k. E)2 (1 + k. E)3 (1 + k. E)n 10 (1 + 0. 07)2 10 (1 + 0. 07)3 10 (1 + 0. 07)n P 0 = –––––––––– + … + ––––– 1 + 0. 11 (1 + 0. 11)2 (1 + 0. 11)3 (1 + 0. 11)n d 1 d 0 (1 + g) 10. 7 P 0 = –––––– + –––– = ––––– = 267. 50 p k. E – g 0. 11 – 0. 07

Pearson plc Ö 10 29. 3 ––––– – 1 = 0. 062 or 6. 2% 16. 1 If it is assumed that this historic growth rate will continue into the future (a big if) and 10 per cent is taken as the required rate of return d 1 29. 3 (1 + 0. 062) P 0 = ––––––––––––– = 819 p k. E – g 0. 10 – 0. 062 g=

Non-constant growth • Noruce plc has just paid an annual dividend of 15 p per share and the next is due in one year • For the next three years dividends are expected to grow at 12 per cent per year • After the third year the dividend will grow at only 7 per cent per annum • Expected return of 16 per cent per annum Stage 1 Calculate dividends for the super-normal growth phase. d 1 = 15 (1 + 0. 12) = 16. 8 d 2 = 15 (1 + 0. 12)2 = 18. 8 d 3 = 15 (1 + 0. 12)3 = 21. 1

Noruce Stage 2 Calculate share price at time 3 when the dividend growth rate shifts to the new permanent rate. d 4 d 3 (1+g) 21. 1 (1 + 0. 07) P 3 = –––––– + –––– = ––––––– = 250. 9 k. E – g 0. 16 – 0. 07 Stage 3 Discount and sum the amounts calculated in Stages 1 and 2. d 1 16. 8 –––– = ––––– 1 + k. E 1 + 0. 16 d 2 18. 8 + –––– = ––––– (1 + k. E)2 (1 + 0. 16)2 d 3 21. 1 + –––– = ––––– (1 + k. E)3 (1 + 0. 16)3 P 3 250. 9 + –––– = ––––– (1 + k. E)3 (1 + 0. 16)3 = 14. 5 = 14. 0 = 13. 5 = 160. 7 202. 7 p

Issues with DGM • What is a normal growth rate? • Companies that do not pay dividends • Problems with dividend valuation models – 1 They are highly sensitive to the assumptions d (1 + g) 24. 2 (1 + 0. 08) 0 e. g. Pearson: P 0 = ––––––––––––– = 1, 742 p k. E – g 0. 095 – 0. 08 – 2 The quality of input data is often poor – 3 If g exceeds k. E a nonsensical result occurs

Forecasting dividend growth rates – g • Determinants of growth – 1 The quantity of resources retained and reinvested within the business – 2 The rate of return earned on those retained resources – 3 Rate of return earned on existing assets

Growth • Focus on the firm – 1 Strategic analysis – 2 Evaluation of management – 3 Using the historical growth rate of dividends – 4 Financial statement evaluation and ratio analysis • Accounts have three drawbacks: (a) they are based in the past (b) the fundamental value-creating processes within the firm are not identified and measured in conventional accounts, (c) they are frequently based on guesses, estimates and judgements • Focus on the economy

The price-earnings ratio (PER) model Current market price of share 200 p Historic PER = –––––––––––––– = 20 Last year’s earnings per share 10 p Source: Financial Times, 5 May 2007. Reprinted with permission.

PERs for the UK and US (S&P 500) stock markets, 1964– 2007

The crude and the sophisticated use of the PER model • Some analysts use the historic PER (P 0/E 0), to make between firms comparisons • Analysing through comparisons lacks intellectual rigour – The assumption that the ‘comparable’ companies are correctly priced is a bold one • It fails to provide a framework for the analyst to test the implicit input assumptions d 0 P 0 = ––––––– k. E – g P 0 d 1/E 1 = ––––––– E 1 k. E – g important

Ridge plc • Payout ratio of 48 per cent of earnings • Discount rate 14 per cent • Expected growth rate 6 per cent d 1/E 1 P 0 = ––––––– E 1 k. E – g P 0 0. 48 = –––––– = 6 E 1 0. 14 – 0. 06 • Now assume a k. E of 12 per cent and g of 8 per cent P 0 0. 48 = –––––– = 12 E 1 0. 12 – 0. 08 • If k. E becomes 16 per cent and g 4 per cent then the PER reduces to two-thirds of its former value: P 0 0. 48 = –––––– = 4 E 1 0. 16 – 0. 04

Whizz plc • Earnings per share rise by 10 per cent per annum • Prospective price earnings ratio (PER) of 25 • Beta of 1. 8, Risk premium 5 per cent, Current risk-free rate of return is 7 per cent k. E = rf + β (rm – rf) k. E = 7 + 1. 8 (5) = 16% P 0 d 1 / E 1 0. 5 = ––––––––––––– = 8. 33 E 1 k. E – g 0. 16 – 0. 10

Prospective PERs for various risk classes and dividend growth rates

A comparison of the crude PER and the more complete model

Lecture review • Valuation using NAV • The dividend valuation models • Growth rate • Price-earnings ratio model