The Income Statement and Statement of Cash Flows

n Extraordinary Items (net of")

n Reported on the face of the income statement –")

- Slides: 25

The Income Statement and Statement of Cash Flows Sid Glandon, DBA, CPA Assistant Professor of Accounting

Comprehensive Income n Total change in equity EXCLUDING transactions with owners

Other Comprehensive Income n Comprehensive Income – Change in equity as a result of non-owner transactions – Net income, plus (minus) – Other Comprehensive Income • Unrealized gains/losses • Foreign currency translations n Presentation – Extension of income statement – Statement of comprehensive income – Statement of shareholders’ equity

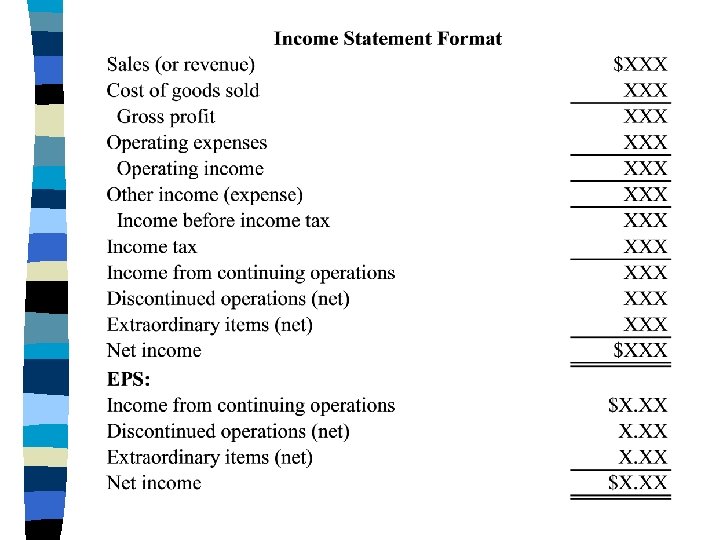

Elements of the Income Statement n Operating income – Revenues – Expenses n Other income (expense) – Gains – Losses

Multiple-Step Income Statement n Separation of – Operating activities – Nonoperating activities n Classification of expenses by functions – matches costs and expenses with related revenues

Separately Reported Items n Discontinued Operations (net of tax) n Extraordinary Items (net of tax)

Format: Multi-Step Income Statement n Operating section n Nonoperating section n Income tax n Discontinued operations n Extraordinary items n Earnings per share

Operating Section

Nonoperating Section

Separately Reported Items n Reported above the line - Income from continuing operations before income tax – Unusual gains and losses (if material) n Reported below the line - Income before discontinue operations and extraordinary item – Discontinued operations (net of tax) – Extraordinary items (net of tax)

Separately Reported Items Reported Below the Line

Intra-Period Tax Allocation n Income from operations n Discontinued operations n Extraordinary items

Earnings Per Share (EPS) n Reported on the face of the income statement – Income before discontinued operations and extraordinary items – Separately reported items • Discontinued operations (net of tax) • Extraordinary items (net of tax) – Net income n EPS calculation – [Net income less preferred dividends] ÷ [weighted average of common shares outstanding]

EPS

Accounting Changes n Change in accounting principle n Change in estimate n Change in reporting estimate

Change in Accounting Principle n Accounted for retrospectively – Revise prior years’ financial statements

Change in Accounting Estimate n Accounted for prospectively – Adjust current and future years n Estimates include: – Amortization – Depreciation – Depletion – Bad debt expense

Change in Reporting Entity n Accounted for retrospectively – Revise prior years’ financial statements

Correction of Accounting Errors n Required a prior period adjustment to retained earnings n Made to the earliest period reported in the comparative financial statements

Retained Earnings Statement n Beginning balance n Prior period adjustment – correction of an error in the financial statements of a prior period n Income or loss n Dividends n Ending balance

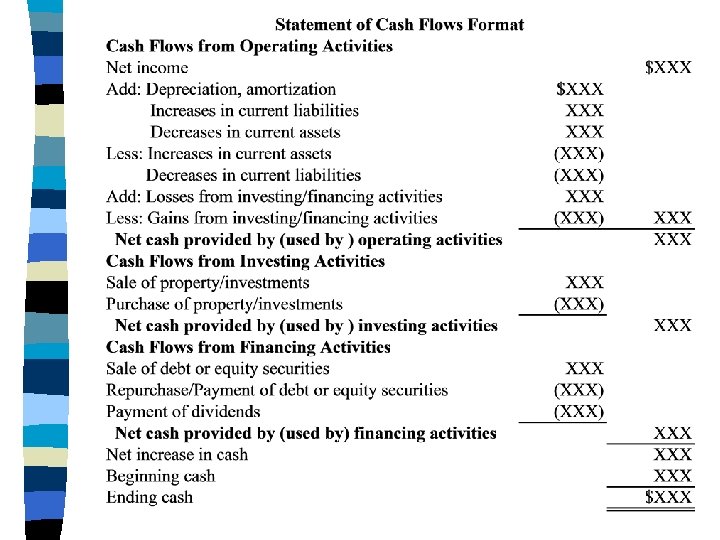

Statement of Cash Flows n Operating activities n Investing activities n Financing activities

Methods of Presenting Cash Flows from Operating Activities n Direct method n Indirect method – Reconciliation of net income to cash flows

Indirect Method of Reporting Cash Flows from Operating Activities n Net income – Plus: • Non cash charges • Increases in current liabilities • Decreases in current assets – Less: • Increases in current assets • Decreases in current liabilities – Plus: losses from investing or financing activities – Less: gains from investing or financing activities – Net cash provided by (used by) operating activities