IRAN TRANSPORTATION LOGISTICS FORUM IRAN RAIL TRANSPORT MOVING

Vertical Integration Vertical Separation A public railway Need to")

")

")

Developing new tracks? Providing")

%2015/2006 2015 21. 6% 2012 10459 10223 2009 2006")

Access")

1000/Train-Km 27. 6 20. 2")

Annual Comments 1000/Ton-Km")

2009 1980 Index +45%")

- Slides: 19

IRAN TRANSPORTATION & LOGISTICS FORUM IRAN RAIL TRANSPORT, MOVING TOWARD PPP (A VERTICAL SEPARATION APPROACH) Majid Babaie Secretary General, Guild of Rail Transport Companies and Related Services

Shift to Privatization 2005 (1384) Vertical Integration Vertical Separation A public railway Need to private sector’s investment Low Productivity of services & assets Low labor productivity Low quality of services Low market share Toward PPP

Vertical Integration vs. Vertical Separation Degree of EOS VI Balance (Regulator, Size, Investment Cost…) VS Degree of market pressure and openness

pros and cons of Vertical Separation in Iran’s rail industry (privatization and regulatory reform) PROS CONS §Broke down barriers to entry in industry §An independent regulator does not exist. No certain arbitration unit. §An appropriate way to curtail the monopoly power of “natural monopolies” §Government may pull out national budget from the sector. §Labor productivity is relatively higher than VI §More intensive use of capacity §More flexible management §Government don’t like to withdrawal from operational tasks. §Loss of Economies of Scale

Rail market share growth depends on? (Goal: 30% + 20%) Developing new tracks? Providing new rolling stock? Increase of prices? Increase of rail budget? Increase demand for rail? ? ? ? Appropriate Policymaking, A Sustainable PPP structure, More productivity,

Rail passenger to total land transportation % 15 13 11 9 7 5 Road passenger to total land transportation % 95 93 91 89 87 85 84 85 86 87 88 89 90 91 92 93 94 95 Rail freight to total land transportation % 15 13 11 9 7 5 Road freight to total land transportation % 95 93 91 89 87 85 84 85 86 87 88 89 90 91 92 93 94 95

Rail transport performance (2006 -2015) %2015/2006 2015 21. 6% 2012 10459 10223 2009 2006 Unit Index 9482 8595 Km Tracks 8. 2% 35. 7 34. 3 32. 8 33 M/ton Tonnage 22% 25 22. 6 20. 2 20. 5 Billion Ton-Kilometer -4. 3% 1435 906 1487 1500 1000/ton Transit Tonnage 14. 5% 24. 4 27 27. 7 21. 3 Million Passenger 19. 2% 14. 9 17. 2 16. 8 12. 5 Billion P - Kilometer 50% 39 53. 9 78. 6 % M/ton- Allocation of development credits 0% 3. 8 3. 9 3. 8 10. 1% 1150 1100 980 1044 1000/ton-K Freight wagon productivity 20. 2% 12. 5 11. 3 11. 8 10. 4 M/p-k Passenger wagon productivity passenger K Track productivity

Share of freight revenue % Value added tax Wagon owner Locomotive owner(70% public) Access charge year 0 25% 23% 52% 2009 0 22% 21% 57% 2010 2% 21% 23% 54% 2011 5% 18% 23% 54% 2012 6% 23% 31% 41% 2013 7% 29% 30% 34% 2014 8% 31% 32% 29% 2015 8. 2% 31. 3% 32. 4% 28. 2% 2016 95 ﺍﺳﻔﻨﺪ ﻣﺎﻩ , ﻣﻌﺎﻭﻧﺖ ﺑﻬﺮﻩ ﺑﺮﺩﺍﺭی ﻭ ﺳیﺮ ﻭ ﺣﺮکﺖ ﺭﺍﻩ آﻬﻦ , گﺰﺍﺭﺵ ﺭﻗﺎﺑﺖ پﺬیﺮی ﺣﻤﻞ ﺑﺎﺭ ﺭیﻠی : ﻊ

Track productivity (Train-Km per each km of main tracks) 1000/Train-Km 27. 6 20. 2 19. 7 ﻧﺎﻡ کﺸﻮﺭ Japan China England ﺭﺩیﻒ 1 2 3 16. 9 Germany 4 12. 1 11. 5 10. 5 9. 9 8. 1 6. 2 Russia EU World France Kazakhstan Iran 5 6 7 8 9 10 ﺍﺳﻔﻨﺪ , ﻣﻌﺎﻭﻧﺖ ﺑﻬﺮﻩ ﺑﺮﺩﺍﺭی ﻭ ﺳیﺮ ﻭ ﺣﺮکﺖ ﺭﺍﻩ آﻬﻦ , گﺰﺍﺭﺵ ﺭﻗﺎﺑﺖ پﺬیﺮی ﺣﻤﻞ ﺑﺎﺭ ﺭیﻠی : ﻣﺮﺟﻊ

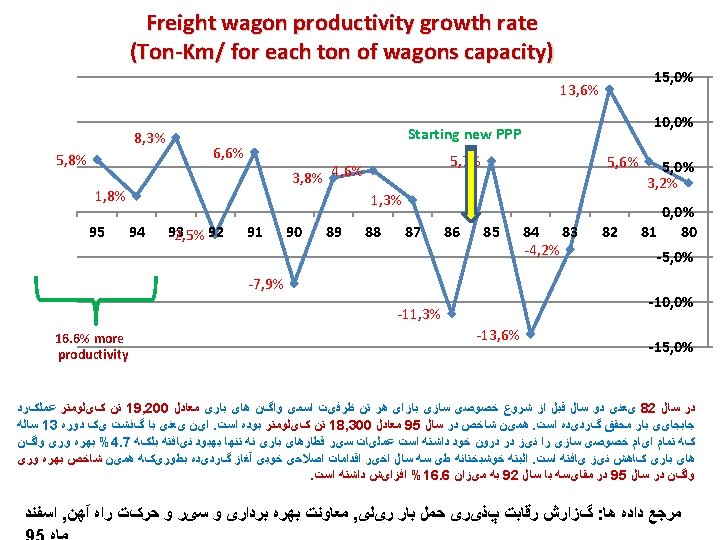

Freight wagon productivity rate (Ton-Km per each ton of wagon capacity) Annual Comments 1000/Ton-Km Growth% 3. 2% 16 5. 6% 16. 9 The highest record 13. 6% 19. 2 -4. 2% 18. 4 Starting new PPP -13. 6% 15. 9 5. 7% 16. 8 The lowest record -11. 3% 14. 9 1. 3% 15. 1 4. 6% 15. 8 3. 8% 16. 4 -7. 9% 15. 1 6. 6% 16. 1 Start point of the 11 th government -2. 5% 15. 7 8. 3% 17 1. 8% 17. 3 16. 6% increase in wagon productivity 5. 8% 18. 3 in 3 years Year 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 ﺍﺳﻔﻨﺪ , ﻣﻌﺎﻭﻧﺖ ﺑﻬﺮﻩ ﺑﺮﺩﺍﺭی ﻭ ﺳیﺮ ﻭ ﺣﺮکﺖ ﺭﺍﻩ آﻬﻦ , گﺰﺍﺭﺵ ﺭﻗﺎﺑﺖ پﺬیﺮی ﺣﻤﻞ ﺑﺎﺭ ﺭیﻠی : ﻣﺮﺟﻊ ﺩﺍﺩﻩ ﻫﺎ

Rail Transport Contribution 2005 -2016 Years 2005 -2016 Access Charges Paid Fuel Total by Rail sector to consumption Ton-Kilometer Saving government (Billion) (Billion $) 265 1. 5 3. 5 Other savings Billions of savings by Externality and side effect Costs in compare to road

Facilitate Competition Rail Market Share Growth Requirements Internal Requirements External Requirements Harmonization of rail and road access charge Uniform subsidies for rail and road fuel consumption More competitive advantages for rail Facilitate rail Transport Move to market Solutions Setup Regulatory Body More market share and growth for rail Increase Productivity Eliminating investment barriers by private sector Based on a Roadmap

Results of VS imperfect restructuring? • No separation between governance and operational activities • Government approach not changed • More intervention by government without any limitation • Real Private companies not entered (more government linked companies) • Unreliability space is the most important obstacle for new investors • Policymaking is a forgotten role of government • There is no enough authority for rail private companies to improve productivity by their capabilities • As a whole internal and external requirements for rail development is not available at both public and private sides

US railway, A successful reform

US rail performance after 1980 reform Change% (Last year/Base year) 2009 1980 Index +45% 2007 – 39% 27% Rail Market share% +100% +500% +110% 2007 - 1800 2008 - 360 2008 - 190 900 60 1990 - 90 Ton-Mile(Billion) Revenue to Operational cost -35% -61% 2007 – 65. 5 1985 - 100 Price index 2008 - 55 1990 - 140 Price to cost index +173% 8% 2. 93% Return on investment -67% 2008 -150, 000 450, 000 # of Personnel +150% 2008 - 250 100 Human resources cost index +427% 4177 792 Revenue by each Person($) +30% 2008 - 130 100 Fuel consumption cost index +110% +189% 480 9530 2. 6 228 3297 11. 4 Revenue by each gallon($) -77% Cost index Revenue by each track Km($) Accidents per each million train-mile

Performance of Class I Railroads 1964 -2005

IRAN TRANSPORTATION & LOGISTICS FORUM Thanks for your attention