IBM IBM Corporate Financial Restructuring Prof Ian Giddy

IBM

IBM Corporate Financial Restructuring Prof. Ian Giddy New York University

Restructuring: Any substantial change in a company’s financial structure, or ownership or control, or business portfolio. l Designed to increase the value of the firm Restructuring l Improve capitalization Copyright © 2004 Ian H. Giddy Improve debt composition Change ownership and control Corporate Financial Restructuring 4

Restructuring Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 5

A Simple Framework A company is a “nexus of contracts” with shareholders, creditors, managers, employees, suppliers, etc l Restructuring is the process by which these contracts are changed – to increase the value of all claims. l Applications: l urestructuring creditor claims (Conseco); urestructuring shareholder claims (AT&T); urestructuring employee claims (UAL) Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 6

“Nexus of Contracts” Franchisors Senior lenders Salespeople Subordinated lenders Management Copyright © 2004 Ian H. Giddy Shareholders Corporate Financial Restructuring 7

A restructuring course on giddy. org Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 8

Why and How l Why restructure? u. What is the fundamental problem to be solved? l How restructure? u. Create or preserve value, and negotiate how the gains are distributed l When restructure? u. Pre-emptive, l or under duress? Implementing restructuring Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 9

Restructuring at Tower n. Portfolio? n. Financial? n. Organizational? n. Or Copyright © 2004 Ian H. Giddy what? Corporate Financial Restructuring 10

Why Restructure? Some Reasons Address poor performance l Exploit strategic opportunities l Correct valuation errors l Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 11

How Restructure? Fix the business l Fix the financing l Fix the ownership/control l Create or preserve value l Negotiate distribution of the value l Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 12

How Restructure? Some Obstacles There are market imperfections or institutional rigidities that make it difficult for the firm to recontract l These include: l u. Transaction costs u. Taxes u. Agency costs u. Information asymmetries l Example: The restructuring of UAL Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 13

TDI in Trouble Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 14

When The Creditors are Prowling Time for a Tiger Reason The financing is bad Remedy Raise equity or Change debt mix Copyright © 2004 Ian H. Giddy Business mix is bad Sell some businesses or assets to pay down debt The company is bad Change control or management through M&A Corporate Financial Restructuring 15

Average Impact of Restructuring on Company Performance Source: Bowman et al, “When Does Restructuring Improve Economic Performance? ” Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 16

Novartis

Operating Restructuring The increase in value that comes from the operating side: l Better operating margins (usually economies of scale ie lower costs) or l Future increased sales/profits from higher growth Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 18

Novartis

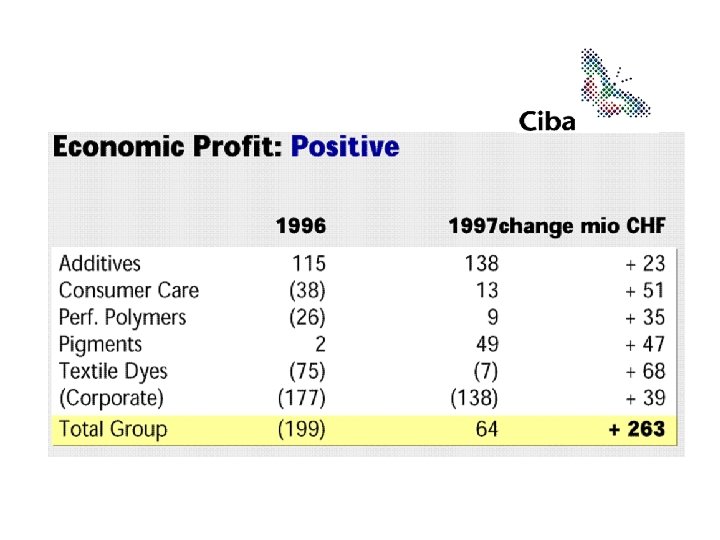

Value-Based Management Sales Operating margin NOPAT* Notional taxes Net Working capital Net Fixed Capital Goodwill *Net Operating Profit After Tax Copyright © 2004 Ian H. Giddy Economic Profit Invested Capital Cost of Capital Source: Ciba Specialty Chemicals Corporate Financial Restructuring 20

Novartis: Financial Restructuring Fixed the cash and working capital Copyright © 2004 Ian H. Giddy Assets Liabilities Cash Debt Fixed Assets Equity Fixed the capital structure Corporate Financial Restructuring 22

Financial Restructuring The increase in value that comes from a purely financial effect: l Lower taxes l Higher debt capacity l Better use of idle cash Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 23

Valuation is a Key to Unlock Value with and without restructuring l Consider means and obstacles l Who gets what? l Minimum is liquidation value l Valuation Going Concern Copyright © 2004 Ian H. Giddy After Restructuring Liquidation Corporate Financial Restructuring 24

Mr. Michael D. Eisner The Walt Disney Company 500 South Buena Vista Street Burbank, California 91521 Dear Michael: I am writing following our conversation earlier this week in which I proposed that we enter into discussions to merge Disney and Comcast to create a premier entertainment and communications company. It is unfortunate that you are not willing to do so. Given this, the only way for us to proceed is to make a public proposal directly to you and your Board. We have a wonderful opportunity to create a company that combines distribution and content in a way that is far stronger and more valuable than either Disney or Comcast can be standing alone. To this end, we are proposing a tax-free stock for stock merger in which Comcast would issue 0. 78 of a share of its Class A voting common stock for each share of Disney. This represents a premium of over $5 billion for your shareholders, based on yesterday's closing prices. Under our proposal, your shareholders would own approximately 42% of the combined company. The combined company would be uniquely positioned to take advantage of an extraordinary collection of assets. Together, we would unite the country's premier cable provider with Disney's leading filmed entertainment, media networks and theme park properties. …. . Copyright © 2004 Ian H. Giddy Estimates: Forbes, Dec 2002 February 11, 2004 Estimates: CNN, Jan 2003 Dear Michael, Corporate Financial Restructuring 25

Capital Structure: Too Little or Too Much? Nokia VALUE OFTHE FIRM Ahold Optimal debt ratio? DEBT RATIO Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 26

See Saw Business Uncertainty Operating Leverage Financial Risk Financial Leverage Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 27

Debt Restructuring Analysis Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 28

“Nexus of Contracts” Franchisors Senior lenders Salespeople Subordinated lenders Management Copyright © 2004 Ian H. Giddy Shareholders Corporate Financial Restructuring 30

TDI Financial History Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 31

u.")

Restructuring Debt and Equity l TDI (sequence of operational and financial restructuring efforts) u. Restructuring under threat of financial distress u. Restructuring to exploit free cash flows u. Exit options Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 32

TDI Financial History Leveraged Buyout New Management Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 33

Restructuring Debt and Equity at TDI Evaluate the financial restructuring that took place at TDI: l Effect of an LBO on capital structure? l How would LBO lenders protect their interests? l With too much debt, what possible restructuring plans? Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 34

Restructuring, Phase 1 Source: debtcapacity. xls Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 35

Interest Coverage, Ratings, and Cost Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 36

l Reduce interest l Swap")

What Possible Restructuring? Extend debt maturity (principal and/or interest) l Reduce interest l Swap debt into equity l Raise new funding l Sell assets l Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 37

TDI Financial History Copyright © 2004 Ian H. Giddy Banks are getting really annoyed Corporate Financial Restructuring 38

Restructuring, Phase 2 Source: debtcapacity. xls Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 39

Consider the choices facing TDI in 1994:")

Restructuring Debt and Equity at TDI (C) Consider the choices facing TDI in 1994: l Evaluate the alternatives available to take best advantage of TDI’s free cash flow: u Leveraged buyout u Leveraged ESOP u Leveraged recapitalization l l Or: Invest cash or debt in growth opportunities Or: Do nothing to retain flexibility Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 40

TDI Financial History Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 41

Restructuring, Phase 3 Source: debtcapacity. xls Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 42

Time for an IPO? Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 43

Restructuring Checklist Figure out what the business is worth now Use valuation model – present value of free cash flows Fix the business mix – divestitures Value assets to be sold Fix the business – strategic partner or merger Value the merged firm with synergies Fix the financing – improve D/E structure Revalue firm under different leverage assumptions – lowest WACC Fix the kind of equity What can be done to make the equity more valuable to investors? Fix the kind of debt or hybrid financing What mix of debt is best suited to this business? Fix management or control Value the changes new control would produce Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 44

Applying the Checklist Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 45

IBM Applied Corporate Finance Prof. Ian Giddy New York University Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 46

Risker Investments Have to Offer Higher Returns Risk and Return u. A positive relationship exists between risk and nominal or expected return u The actual return earned on a security will affect the subsequent actions of investors u Investors must be compensated for accepting greater risk with the expectation of greater return Risk Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 47

Equity versus Bond Risk Assets Liabilities Debt Uncertain value of future cash flows Copyright © 2004 Ian H. Giddy Contractual int. & principal No upside Senior claims Control via restrictions Equity Residual payments Upside and downside Residual claims Voting control rights Corporate Financial Restructuring 48

“Efficient frontier” Individual assets Global minimumvariance portfolio")

The Minimum-Variance Frontier of Risky Assets E(r) “Efficient frontier” Individual assets Global minimumvariance portfolio Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 49

The Cost of Capital Choice Cost 1. Equity - Retained earnings - New stock issues - Warrants Cost of equity - depends upon riskiness of the stock - will be affected by level of interest rates Cost of equity = riskless rate + beta * risk premium 2. Debt - Bank borrowing - Bond issues Cost of debt - depends upon default risk of the firm - will be affected by level of interest rates - provides a tax advantage because interest is tax-deductible Cost of debt = Borrowing rate (1 - tax rate) Debt + equity = Capital Cost of capital = Weighted average of cost of equity and cost of debt; weights based upon market value. Cost of capital = kd [D/(D+E)] + ke [E/(D+E)] Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 50

Pfizer’s WACC l l l We do not recommend any specific changes to Pfizer's D/E ratio. We observe that management could safely increase the D/E ratio (slightly decreasing the WACC) if worthy projects were identified. Should management choose to increase the D/E ratio, the bond rating would not be lowered until the D/E ratio hits approximately 30%. Copyright © 2004 Ian H. Giddy (See Excel spreadsheet for details. ) Corporate Financial Restructuring 51

Investment Decisions: Would You Buy One of These? Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 52

Forestry Application Outlay $2321 Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 53

Forestry Application giddy. org/ibmfinance/forestry. xls Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 54

Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 55

: n. USD 15% n.")

Nokia’s Risk Management Net foreign transaction exposure (non-EUR currencies) : n. USD 15% n. GBP 30% n. AUD 7% n. JPY 26% n. SEK 5% n. Others 17% Conclusion : Nokia’s distribution of sales and production/personnel is well balanced throughout the 10 major markets, with the exception of Japan. However, the risk due to the Japanese Yen is reduced by the fact that purchases in Yen exceed sales in Yen. Japanese companies are a major source for parts. In 2003, Nokia used the following financial instruments and notional amounts to hedge the financial risks due to currency exchange rates, interest rates and investment activities (USDm) : Derivative financial instrument notional amount, 2003 n. Foreign exchange forward contracts 12’ 623 n. Currency options bought 3’ 594 n. Currency options sold 3’ 045 n. Interest rate swaps 1’ 844 n. Cash settled equity options 280 Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 56

The Gains From an Acquisition Gains from merger Synergies Top line Copyright © 2004 Ian H. Giddy Bottom line Control Financial restructuring Business Restructuring (M&A) Corporate Financial Restructuring 57

What’s the Company Worth? Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 58

The Decisions That Affect Value Macro Factors Economy Industry Life Cycle Company Dynamics Financial Choices Strategic Choices Decision Makers Business Issues Business M&A Divestitures Restructuring Enhance Company Value Financial Debt Equity Risk Management Financial Issues Volatility of Cash Flows Operating Leverage Copyright © 2004 Ian H. Giddy Financial Leverage Corporate Financial Restructuring 59

Contact Info Prof. Ian H. Giddy NYU Stern School of Business Tel 212 -998 -0563; Fax 212 -995 -4233 Ian. giddy@nyu. edu http: //giddy. org Copyright © 2004 Ian H. Giddy Corporate Financial Restructuring 62

- Slides: 59