GAAP Generally Accepted Accounting Principles Over the years

")

- Slides: 21

GAAP Generally Accepted Accounting Principles

• Over the years, the CICA have established GAAP (Generally Accepted Accounting Principles) • GAAP are the standards and rules for accountants in Canada.

GAAP – The Business Entity Concept • The balance sheet of a business must reflect the financial position of the business alone. • Personal expenditures are charged to the owner.

GAAP - The Continuing Concern Concept • It is expected that the business will continue to operate. • If it is know that it will not continue, it must be made known.

GAAP – The Principle of Conservatism • Prices should be recorded at fair amounts. • If there is uncertainty, a best ‘conservative’ guess should be use. eg. We will probably make $20, but maybe someone will come along and pay us $100!! (Record the value at $20. )

Page 30, Exercise 1

Case 3, Page 43 • 1. If the company were to go out of business, and the Machinery and Equipment were worth much less than stated, it would be hard for the bank to still get its money. • 2. Sales figures for the year would also help the manager evaluate the company’s ability to repay the loan. • 3. The balance sheet should make sure to note that some of the business’ activities are stopping. (And should re-evaluate how much should be reported on the balance sheet for Machinery and Equipment. ) (Going Concern principle)

• 4. Changes to the balance sheet should include the reduction of $155, 000 of the Machinery and Equipment account to the $35, 000 it is worth on the open market. (Conservatism principle. )

5.

• 6. As indicated in the previous slides, the GAAPs of Conservatism and Going Concern influenced this case.

Claims against the assets: • If a business were to go out of business, what would happen? • To whom do the assets belong? – The claims of creditors are settled first. – The owner gets what is left after the creditors are paid.

Consider the following: How much would Joe have left, if the company went out of business, and he was able to sell the Land & Building quickly for $200, 000? Liquidated Assets: 275, 000 To Creditors: 150, 000 Left over: $125, 000

The Changing face of the balance sheet. . • The balance sheet can be though of as a ‘snapshot’ of a company’s finances. • It shows what a company is worth at a given moment in time. • What if a company makes a profit or sells some of its assets? • The company’s snapshot has changed, and this will be reflected in the balance sheet.

Transactions • On any given day, different events occur that cause the financial position of a business to change. • These events are called Transactions. • For example: – A business buys a truck for $20, 000. – Its asset ‘cash’ would decrease by $20, 000 – Its asset ‘trucks’ would increase by $20, 000

• A business transaction is defined as a financial event that causes a change in financial position.

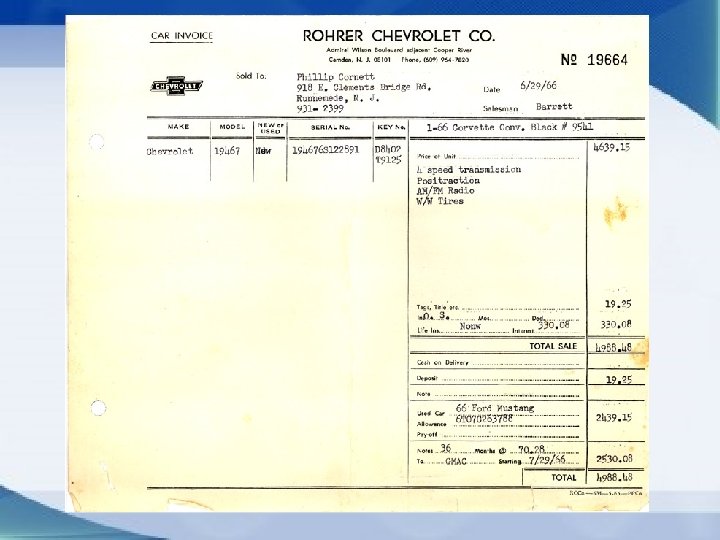

What is this? If a business were to buy an asset, it must have a business paper or document to verify the amount paid. This record of the transaction is called a ‘source document. ’

Source Documents • Include: – Telephone Bills – Store Receipts – Debit card slips – Cancelled Cheques – Invoices (Information needed by the accounting department to record the transaction. )

Documents… • • provide proof of payment are proof of purchase are used for reference are filed (for at least 6 years) in case owners, managers, or auditors wish to refer to them.

GAAP • The objectivity principle states that accounting will be recorded on the basis of objective evidence. (Receipts & Source Documents)

Homework: • Page 38, Review Exercises – 1 -5, 7 • Page 50, Exercises – 1 -4