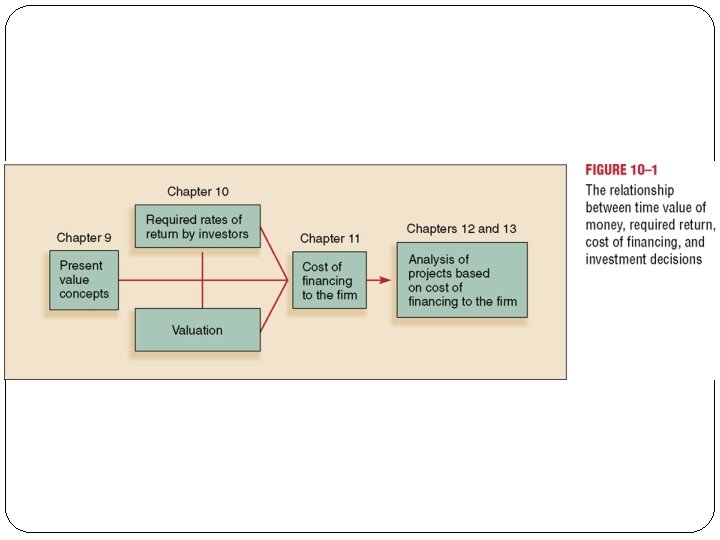

Chapter 10 Valuation and Rates of Return Chapter

")

is equal to the present value of expected future cash flows")

If dividends are expected to grow at")

ratio can also be used to")

- Slides: 17

Chapter 10 Valuation and Rates of Return

Chapter 10 - Outline Valuation of Bonds Relationship Between Bond Prices and Yields Preferred Stock Valuation of Common Stock Valuation Using the Price-Earnings Ratio Factors that Influence the Required Rate of Return

Valuation of Bonds The value of a bond is made up of 2 parts added together: – PV of the interest payments (an annuity) – PV of the principal payment (a lump sum) The principal payment at maturity: – can also be called the par value or face value – is usually $1, 000 The interest rate used: – is the yield to maturity or discount rate – is also the required rate of return

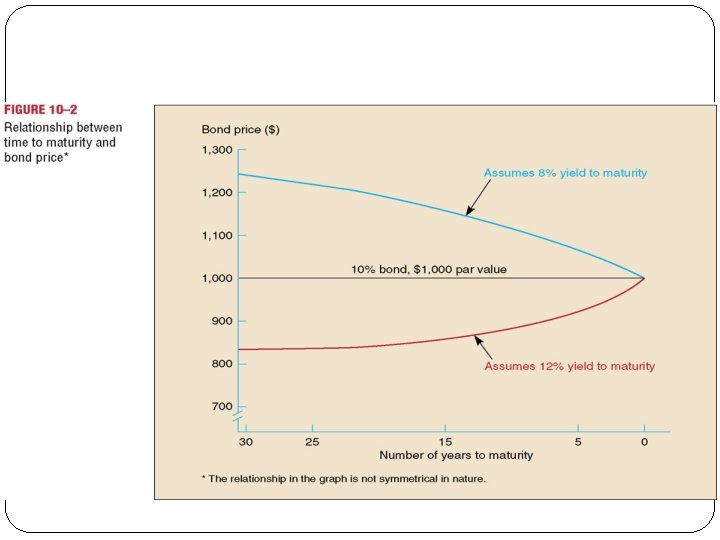

Relationship Between Bond Prices and Yields Bond prices are inversely related to bond yields (move in opposite directions) The longer the maturity, the more sensitive the bond prices are to interest rate changes. As interest rates in the economy change, the price or value of an existing bond changes: – if the required rate of return increases, the price of the bond will decrease – if the required rate of return decreases, the price of the bond will increase

Valuing bonds Some definitions: n BOND Long-term debt issued by government or firms n COUPON Regular interest payment on bond n FACE VALUE Amount repaid at maturity (usually $1000) Example: A Treasury 9% coupon bond matures in 1998. In 1993 each bond offered these cash flows: 1994 $90 1995 $90 1996 $90 1997 $90 1998 $1090 The interest rate on similar bonds was 5. 3%. Therefore the value of 9% Treasuries was $90 PV = $90 + + (1 + r)2 $90 = + 1. 053 = $1158. 87 $90 + (1 + r)3 $90 + (1. 053)2 $90 + (1 + r)4 (1 + r)5 $90 $1090 + (1. 053)3 $1090 + (1. 053)4 (1. 053)5

Calculating bond yields If the price of the 9% Treasury bond is $1158. 87, what return do investors expect? Return is usually measured by the yield to maturity. This is the discount rate, r, that makes a bond's present value equal to price. $90 PV = $90 + (1 + r)2 $90 + (1 + r)3 = $1158. 87 Yield to maturity (r) =. 053 or 5. 3%. $1090 + (1 + r)4 (1 + r)5

Preferred Stock Preferred stock: – usually represents a perpetuity (something with no maturity date) – has a fixed dividend payment – is valued without any principal payment since it has no ending life – is considered a hybrid security (a mixture of a stock and a bond) – owners have a higher priority than common stockholders Value = Pref. Div / Kp

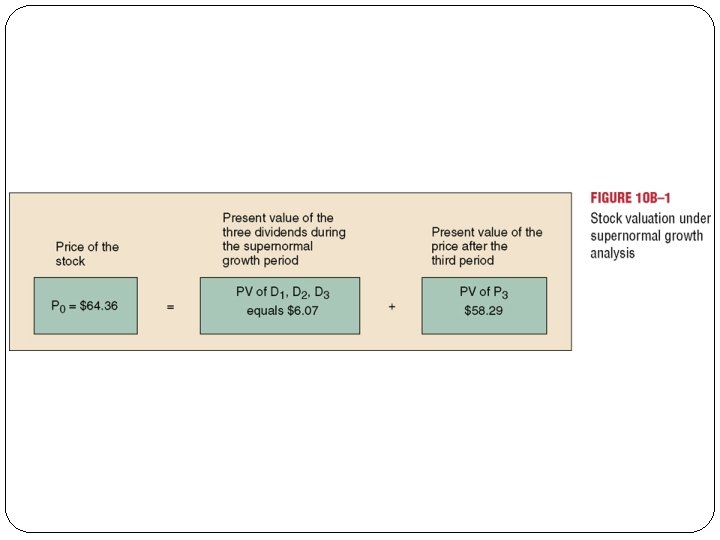

Valuation of Common Stock The value of common stock is the present value of a stream of future dividends Common stock dividends can vary, unlike preferred stock dividends There are 3 possible cases: – No growth in dividends (valued like preferred stock) – Constant growth in dividends – Variable growth in dividends

Stock price (value) is equal to the present value of expected future cash flows (dividends) P 0 DIV 1 + P 1 = 1+r Similarly P 1 = DIV 2 + P 2 1+r Therefore P 0 = DIV 1 1+r + DIV 2 + P 2 (1 + r) 2 We can also express P 2 in terms of DIV 3 & P 3 etc. Thus P 0 = DIV 1 1+r + DIV 2 (1 + r)2 + DIV 3 (1 + r)3 +. . .

Constant-growth dividend discount model (the Gordon model) If dividends are expected to grow at a constant rate (g), the value of the stock is DIV 1 PV = r-g Example: Blue Skies is expected to pay a $3 dividend next year (DIV 1 = 3). Investors expect Blue Skies dividends to increase by 8% a year indefinitely (g =. 08). The discount rate is 12% (r =. 12). PV = DIV 1 r-g 3 = = $75. 12 -. 08 Note: The formula works only if g is less than r

Estimating the required rate of return (a special cas If dividends are expected to grow at a constant rate, g P 0 = r = DIV 1 r-g DIV 1 + g P 0 Note: This is a special case that only works for constant growth cases.

Valuation Using the Price-Earnings Ratio The Price-Earnings (P/E) ratio can also be used to value stocks The P/E ratio is influenced by: – the earnings and sales growth of the firm – the risk (or volatility in performance) – the debt-equity structure of the firm – the dividend policy – the quality of management – a number of other factors

High vs. Low P/Es A stock with a high P/E ratio: – indicates positive expectations for the future of the company – means the stock is more expensive relative to earnings – typically represents a successful and fast-growing company – is called a growth stock A stock with a low P/E ratio: – indicates negative expectations for the future of the company – may suggest that the stock is a better value or buy – is called a value stock

Factors that Influence the Required Rate of Return Real Rate of Return: – represents the opportunity cost of the investment Inflation Premium: – a premium to compensate for the effects of inflation Risk Premium: – a premium associated with business and financial risk