Audit Planning and Analytical Procedures Yulazri M Ak

• The work is to be adequately planned •")

10 Pernyataan standar Generally Accepted Auditing Standards General")

level analysis of financial statements involving")

Prelim. Net sales Cost")

Current liabilities")

- Slides: 65

Audit Planning and Analytical Procedures Yulazri M. Ak. , CPA

First Standard of Fieldwork (GAAS) • The work is to be adequately planned • and assistants, if any, are to be • properly supervised.

Three Main Reasons for Planning To obtain sufficient competent evidence for the circumstances To help keep audit costs reasonable To avoid misunderstanding with the client

Proses/tahapan audit previous Planning Field work Reporting Risk respond Reporting new Risk

Perencanaan audit Audit should be plan

Summary of General Standards (before 2013) 10 Pernyataan standar Generally Accepted Auditing Standards General : 3 Field Work : 3 Reporting : 4 1. Adequate training and proficiency 2. Independence in mental attitude 3. Due professional care 1. Proper planning and supervision 2. Internal control understanding 3. Sufficient competent evidence 1. Statements prepared in accordance with GAAP 2. Circumstances when GAAP not followed 3. Adequacy of disclosures 4. Expression of opinion on financial statements 6

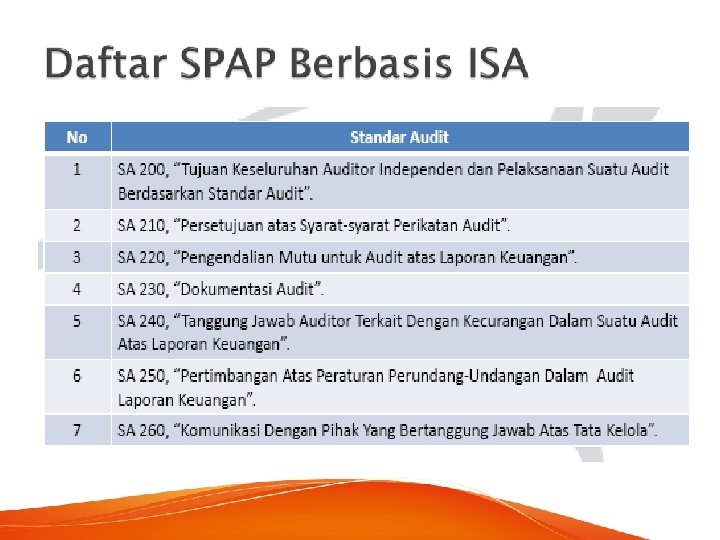

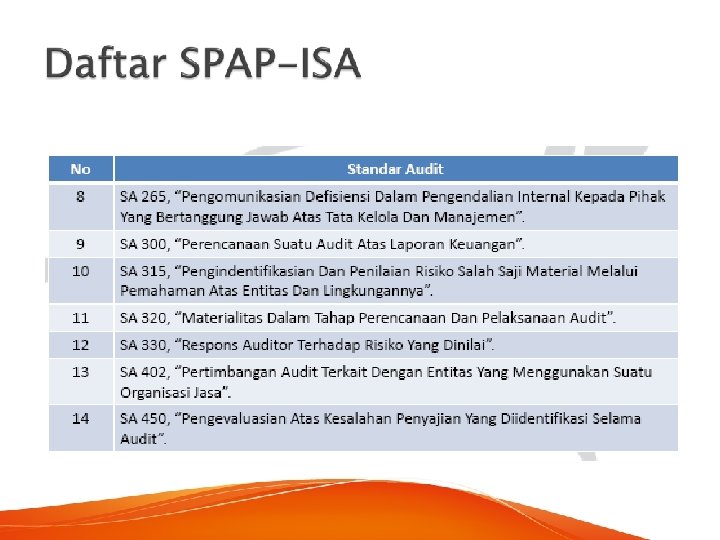

Standar Audit Prinsip Umum dan Tanggung Jawab SA 200 SA 210 SA 220 SA 230 SA 240 SA 250 SA 265 Penilaian Risiko dan Respons terhadap Risiko yang Dinilai SA 300 SA 315 SA 320 Bukti Audit Penggunaan Hasil Pekerjaan Pihak Lain SA 500 SA 600 SA 700 SA 800 SA 610 SA 705 SA 805 SA 706 SA 810 SA 501 SA 505 SA 510 Area Khusus SA 520 SA 330 SA 530 SA 402 SA 540 SA 450 SA 620 Kesimpulan Audit dan Pelaporan SA 550 SA 710 SA 720 SA 560 SA 570 SA 580 7

Three Main Reasons for Planning

Risk Terms Ø Acceptable audit risk Ø Inherent risk

Managing Risk is an Important Aspect of Auditing Acceptable audit risk – level of risk the auditor will accept, that an unqualified opinion is mistakenly issued. Inherent risk – likelihood of material misstatements In accounts before I/C effectiveness is considered.

Initial Audit Planning 1. Client acceptance and continuance 2. Identify client’s reasons for audit 3. Obtain an understanding with the client 4. Develop overall audit strategy

Client Acceptance and Continuance ØNew client investigations §If previously audited, the new auditor is required to communicate with the predecessor auditor §Client permission required ØContinuing clients §Annual evaluations whether to continue based on issues, fees, and client integrity

Identify Reasons for the Audit ØTwo major factors affecting acceptable risk §Likely statement users §Intended uses of the statements ØLikely to accumulate more evidence for companies that are §Publicly held §Have extreme indebtedness §Likely to be sold

Obtaining an Understanding with the Client ØEngagement terms should be understood between CPA and client. ØStandards require an engagement letter describing: §objectives §responsibilities of auditor and management §schedules and fees ØInforms client that auditor cannot guarantee all acts of fraud will be discovered ØSee figure 8 -2

Develop Overall Audit Strategy ØPreliminary audit strategy should consider §client’s business and industry §material misstatement risk areas §number of client locations §past effectiveness of controls ØPreliminary strategy helps auditor determine resource requirements and staffing §staff continuity §need for specialists

Understanding of the Client’s Business and Industry Client business risk is the risk that the client will fail to meet its objectives. Ø Information technology ØGlobal operations ØHuman capital

Understanding of the Client’s Business and Industry

Industry and External Environment Reasons for obtaining an understanding of the client’s industry and external environment: 1. Risks associated with specific industries 2. Inherent risks common to all clients in certain industries 3. Unique accounting requirements

Business Operations and Processes Factors the auditor should understand: Ø Major sources of revenue Ø Key customers and suppliers Ø Sources of financing Ø Information about related parties

Tour the Plant and Offices Touring the physical facilities enables the auditor to assess asset safeguards and interpret accounting data related to assets.

Identify Related Parties ØAffiliated companies ØPrincipal owners of the client ØAny other party with which the client deals ØA party who can influence management or client policies

Management and Governance includes: ØOrganizational structure ØBoard activities ØAudit committee activities. Governance insights: ØCorporate charter and bylaws ØCode of ethics ØMeeting minutes Management establishes the strategies and processes followed by the client’s business.

Code of Ethics In response to the Sarbanes-Oxley Act, the SEC now requires each public company to disclose whether is has adopted a code of ethics that applies to senior management. The SEC also requires companies to disclose amendments and waivers to the code of ethics.

Client Objectives and Strategies are approaches followed by the entity to achieve organizational objectives. Auditors should understand client objectives. § Financial reporting reliability § Effectiveness and efficiency of operations § Compliance with laws and regulations

Measurement and Performance The client’s performance measurement system includes key performance indicators. Examples: – market share – sales per employee – unit sales growth – Web site visitors – same-store sales – sales/square foot Performance measurement includes ratio analysis and benchmarking against key competitors.

Assess Client Business Risk Client business risk is the risk that the client will fail to achieve its objectives. Ø What is the auditor’s primary concern? Ø Material misstatements in the financial statements due to client business risk

Client’s Business, Risk, and Risk of Material Misstatement

Sarbanes-Oxley Act Management must certify it has designed disclosure controls and procedures to ensure that material information about business risks is made known to them. Management must certify it has informed the auditor and audit committee of any significant control deficiencies.

Perform analytical procedures.

Analytical Procedure Definition • Analytical Procedures consist of the evaluation of financial information in audit, made by a study of plausible relationships among both financial and non-financial data. • It involves analysis of significant ratios and trends including the fluctuations that are inconsistent with other relevant data or which deviate from expectations.

Definition-Contd. • “Expectations”, in this context, refer to the auditor’s expectations of what a figure in the accounts being audited should approximately be as worked out from other relevant financial and non-financial information. • Their use is based on the assumption that there are relationships between items in the accounts and that these relationships may be expected to continue.

Analytical Procedure: Examples • The reasonableness of the figure of expenditure on salaries can be verified by multiplying the average number of the employees in each grade with the average salary for the grade. • The reasonableness of the interest on General Provident Fund balance can be verified by multiplying the average balance in the General Provident Fund with the prescribed rate of interest.

Commonly used analytical review procedures • • • comparisons involving a single component comparison across components system analysis predictive analysis regression analysis; and business analysis

Comparisons involving a single component • There are two types of comparisons. – Comparison of the recorded value of a component with its budgeted value. – Comparison of a component’s current value with its value in previous years (trend analysis) • This procedure may be used at both the planning and execution stages of audit. • In trend analysis, it is preferable to compare figures of a few previous years than just the immediately preceding year in order to factor out any anomalies or aberrations specific to a given year.

Comparison across components • This involves analysis of the relationship between more than one financial statement component. (also known as ratio analysis) • Some examples are accounts receivable to turnover ratio, inventory-turnover ratio, gross-margin ratio, etc. • This procedure may be used at both the planning and execution stages of audit. • More effective than single component comparisons because it considers the inter-relationships among different components and provides assurance simultaneously for more than one component.

System analysis • This involves identification of anomalous items within an account balance rather than a macro level analysis of the balance itself. • Individual entries in transaction listings are analysed to locate unusual entries or abnormalities. • This procedure can be effectively used during the execution stage. • However, it is time consuming as it may involve scrutiny of numerous transactions, if performed manually. • For computerized data, use of appropriate auditing software could significantly aid the adoption- of this procedure.

Predictive analysis • This involves creation of an expectation using not just financial data but also operating or external data, independent of the accounting system. • This can be used only where sufficient information independent of the accounting system is available. • Also known as an “independent test of reasonableness”. • For example, volume of imports and import duty rate may be used to predict import duty revenue. • The method is generally used in the execution stage. • As it involves collection of reliable data from outside the accounting system, it is more time consuming than simpler analytical procedures.

Regression analysis • This is a statistical technique that creates an equation to reveal how one variable is related to one or more other variables. • Similar in principle to predictive analysis but has added mathematical rigor and objectivity. • Generally used in the execution stage. • It requires understanding of the statistics of complex variables and is therefore not “userfriendly” to the general auditor. • It also requires much time for application and testing and is therefore not in frequent use.

Business analysis • This is a high (macro) level analysis of financial statements involving critical ratios related to profitability, liquidity, financial stability, debt, etc. • It is a useful technique for identification of risk areas during planning and audit completion stages and also for a better understanding of the entity and its operations. • However, it provides no audit assurance and is not used in the execution stage. • It requires detailed knowledge of general business relationships and trends and thus is a more useful tool for those experienced members of the audit team who can apply their cumulative knowledge of

Steps involved in analytical review • • Develop an expectation Define significant differences Compare the actuals with the expectation Investigate any significant differences between actuals and expectation • Document the first four steps and make an audit conclusion as to whether assurance can be drawn

Analytical procedures can be used for different purposes at different stages of audit, viz. , • in planning the audit, to assist Audit by pointing areas requiring examination • as substantive tests, in areas where analytical procedures can be used to obtain evidential matter regarding the accuracy of figures • in reporting stage, to assist in the final stage of the audit in assessing the conclusions Audit has reached and in evaluation of the overall financial statement presentation by identifying odd or unusual figures in the final accounts.

Purposes of Analytical Review Procedure • • • Understand the entity Indicate risk areas Indicate possible misstatement Reduced detailed test Obtain direct, positive audit assurance Assess going concern

Factors to Consider • • Objective of the analytical procedure Nature of the entity Knowledge gained from the previous audit Availability Reliability Relevancy Source Comparability

Preliminary Analytical Procedures Comparison of client ratios to industry or competitor benchmarks provides an indication of the company’s performance. Preliminary tests can reveal unusual changes in ratios.

Examples of Planning Analytical Procedures

Summary of the Parts of Auditing Planning A major purpose is to gain an understanding of the client’s business and industry.

Planning an Audit and Designing an Audit Approach ØSet materiality and assess acceptable audit risk and inherent risk. ØUnderstand internal control and assess control risk ØGather information to assess fraud risks ØDevelop overall audit plan and audit program

State the purposes of analytical procedures and the timing of each procedure.

Analytical Procedures AU 329 emphasizes the expectations developed by the auditor. 1. Required in the planning phase 2. Often done during the testing phase 3. Required during the completion phase

Timing and Purposes of Analytical Procedures

Select the most appropriate analytical procedure from among the five major types.

Five Types of Analytical Procedures Compare client data with: 1. Industry data 2. Similar prior-period data 3. Client-determined expected results 4. Auditor-determined expected results 5. Expected results using nonfinancial data.

Compare Client and Industry Data Client 2009 Inventory turnover 3. 4 Gross margin 26. 3% 2008 3. 5 26. 4% Industry 2009 3. 9 27. 3% 2008 3. 4 26. 2%

Internal Comparisons

Compare Client Data with Similar Prior Period Data 2009 (000) Prelim. Net sales Cost of goods sold Gross profit Selling expense Administrative expense Other Earnings before taxes Income taxes Net income % of Net sales $143, 086 100. 0 103, 241 72. 1 $ 39, 845 27. 9 14, 810 10. 3 17, 665 12. 4 1, 689 1. 2 $ 5, 681 4. 0 1, 747 1. 2 $ 3, 934 2. 8 2008 (000) Prelim. $131, 226 94, 876 $ 36, 350 12, 899 16, 757 2, 035 $ 4, 659 1, 465 $ 3, 194 % of Net sales 100. 0 72. 3 27. 7 9. 8 12. 8 1. 6 3. 5 1. 1 2. 4

Compute common financial ratios.

Common Financial Ratios Ø Short-term debt-paying ability ØLiquidity activity ratios ØAbility to meet long-term debt obligations ØProfitability ratios

Short-term Debt-paying Ability Cash ratio Quick ratio = (Cash + Marketable securities) Current liabilities = (Cash + Marketable securities + Net accounts receivable) Current liabilities Current assets Current ratio = Current liabilities

Liquidity Activity Ratios Accounts receivable turnover Days to collect receivable Inventory turnover Days to sell inventory = Net sales Average gross receivables = 365 days Accounts receivable turnover = Cost of goods sold Average inventory 365 days = Inventory turnover

Ability to Meet Long-term Debt Obligation Debt to equity = Total liabilities Total equity Times interest = earned Operating income Interest expense

Profitability Ratios Earnings per share Gross profit percent Profit margin = Net income Average common shares outstanding = (Net sales – Cost of goods sold) Net sales = Operating income Net sales

Profitability Ratios Return on assets Return on common equity = Income before taxes Average total assets = (Income before taxes – Preferred dividends) Average stockholders’ equity

Summary of Analytical Procedures Compare ratios of recorded amounts to auditor expectations. Used in planning to understand client’s business and industry. Used throughout the audit Øto identify possible misstatements Øreduce detailed tests Øassess going-concern issues.