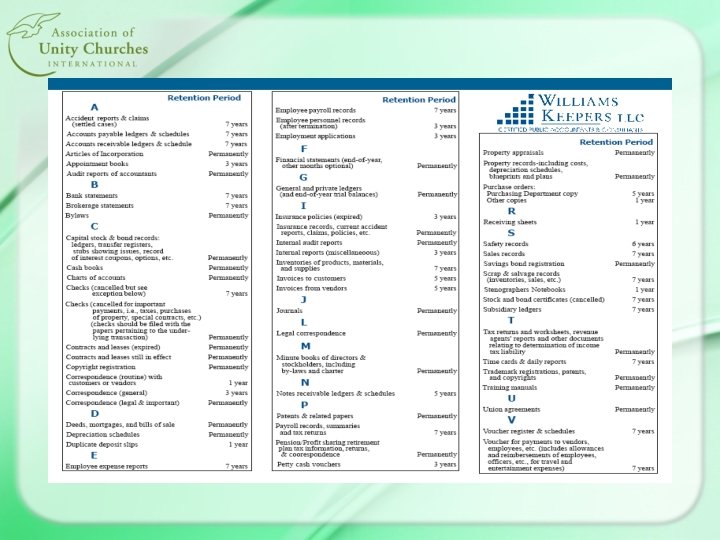

Polity Class Financial Support Services 1 Church Taxes

")

")

–")

Property gift in excess of $5, 000 • Donors")

")

• All church incomes are presumed to be tax exempted")

(W-2, Box 14)")

Allowance • Taxable? – A housing allowance is not taxable for federal")

Allowance (3 Requirements) – The housing allowance must be designated proactively by")

arrangement must meet all of")

– 2. Adequate accounting to the church for expenses with documentary")

– 4. Expenses must be substantiated within 60 days after")

")

")

. – file")

Out of Plan Investment $500, 000 Yield 10% Yield $50, 000")

- Slides: 56

Polity Class Financial Support Services 1. Church Taxes & Finance Rev. K. Young Bae, Ph. D. CFO & Vice President of Finance Association of Unity Churches (816) 524 -7414, young@unity. org Updated 3/6/2008

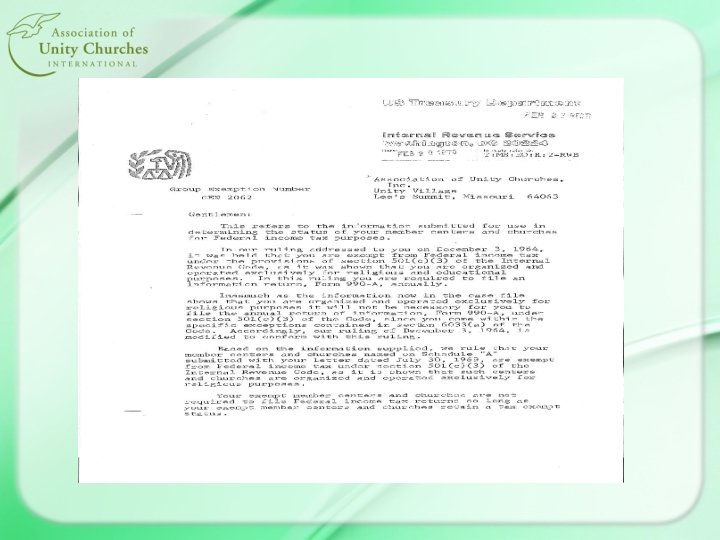

1. Church Taxes & Finance • AUCI provides a Group Tax Exemption Number (GEN 2062) to member churches • AUCI provides consulting services to our member churches on Church Taxes, Church Finances, and Human Resources. • AUCI provides a Group Pension Service and Church Liability Insurance Discount Benefits to member churches.

Church: Tax Exemption Status • Are churches required to apply tax exempt status under IRS Code 501(c)3? – Churches are not required to file: • Application for exemption number (Form 1023) • Annual report (Form 990) (Treas. Reg. 1. 6033 -2) – Key: Churches do not have to apply for tax-exempt status to qualify as tax exemption organizations. • Churches are exempted from paying income tax simply by operation as a church (Treas. Reg. 1. 511 -2 a)

Do we have to apply for a tax exemption number? • Churches affiliated with the Association are not required to file a separate application for exemption number for IRS Code 501 c 3 (Form 1023). • Member churches can use the Association’s Group Tax Exempt Number - Umbrella # (44 -0668175 GEN 2062) – The Association is responsible to evaluate the tax status of its affiliated churches

Tax Exemption Number • The Association has applied for a tax exemption number with filing the Form 1023, and received an IRS approval. – The Association Is not listed in Pub 78, Cumulative List of Organization. • It is because the Association has not filed the form 990, because we are exempted from filing requirement. – However, the Association is required to file an annual report on behalf of all affiliated churches. • The member churches need to make an annual report to the Association

Annual Membership Report to Association

Advantage of Tax Exemption Number • Although churches are, in general, recognized as tax exempted, a church with an exemption number has several advantages. Included are: • Deductible contribution by donors, reduced nonprofit mailing rate, eligible for government/foundation grant application, eligible for property & sales taxes exemption application, 403(b) pension possible, FUTA & SUTA taxes exemption, PSA announcement possible, to opt out from FICA & SECA tax, etc.

Employer Identification Number ? • All churches must obtain an Employer Id Number (EIN) by filing Form SS-4 – An EIN is required even if the church has no employee • This EIN shall be used for all payroll reports, bank account, & other reports. – A toll free (800) 829 -4933 is available to get an EIN by a phone call, without filing the Form SS-4.

Form SS-4 (www. irs. ustreas. gov)

Gifts Acknowledgement • Are churches required to send an annual receiving record to the donors at the year end? – Donors are not allowed a charitable deduction for donations of $250 or more unless the donor has a receipt from your church (Title XIII of OBRA '93 P. L. 103 -66) • For a single donation of $250 or more made by check, the cancelled check is not adequate substantiation • Church needs to send a letter to donors before February 1(see the next slide) – A church can total all of the contribution for a donor and only show the total amount on the receipt.

Required Statement for all receipts • Information on each gift receipt (IRS required) – "No benefits were provided to you in return for your contribution other than intangible religious benefits. Please retain this letter for your tax records, since it fulfills the substantiation requirements that must be met in order to deduct your contribution. " (Title XIII of OBRA '93 P. L. 103 -66)

Gifts Acknowledgement • Gift receipt statement should include: – The donor’s name – Description of the gifts • Amount of cash, or description of property received – The dates the gift made and the receipt issued – The church’s information (name, address, etc. ) – A statement explaining whethere any exchanges for the gift with the church (if yes, then see the next slide)

Quid Pro Quo Gifts • A Quid pro quo gift of more than $75 (Title XIII of OBRA '93 P. L. 103 -66) – A payment made partly as a contribution and partly for goods or services provided to the donor by your church. – Your church is required to provide a receipt for all transaction where the donor makes a payment to your church and receives goods or services other than intangible religious benefits • One single payments of more than $75 are subject to this rule.

– Property Gift (>$5, 000) Property gift in excess of $5, 000 • Donors must obtain a qualified appraisal and attach it to the Form 8283 • Your church needs to sign on the Form 8283 and give it back to the donors – Property gift in excess of $500 but less than $5, 000 • Need to fill out the first page of the Form 8283 • No need for appraisal and your church’s signature – Car donation is subject to a different rule

Property Gift - Car – When your church decides to sell it • Church must send a statement to a donor within 30 days from the date of the car sold, showing description, date, and the sale price of the donated car. – Car in excess of $500 sale price • Donor needs to attach the above statement from church – When church decides to keep it (or sold it to the low income earner) • Donors still can claim the fair market value, based on the rule of other property donation (Form 8283).

Form 8283

Property Gift & Sale – If the property gift of $ 5, 000 or more is sold, exchanged, or disposed of within two years after the gift received, your church must file Form 8282 with the IRS within 125 days of the disposition. – Exception: – No need to report for the property gift more than $5, 000 if the donor is a corporation entity.

Form 8282

Nondeductible Gifts • Non-tax deductible contribution – Strings attached gifts (revocable with some conditions) – Services (professional hour, etc) - Rev Rul. 67236 • However, mileage is deductible 14 cents per mile for the services • However, church needs to issue a statement if the annual total out-of-pocket expense including the mileage exceeds $250

Nondeductible Gifts • How about Classes, Workshop, Speaker Events? (See IRS Pub 526, charitable Contribution) – Adult Classes (Fees or love offering) deductible if • Related to church mission/activities • Presenters are church ministers or staff • Contributors are most likely church members • Payment is made to the church – Workshop, Speaker Events • None of the above, then non-deductible – IRS publication 526, Charitable Contribution

Unrelated Business Income (UBI) • All church incomes are presumed to be tax exempted (IRC Sec 511 -13). • Exception: The following UBIs are taxable: – Not substantially related to the church mission • A restaurant by paid staff, tour with social purposes – A regularly operated business • A church parking lot, charged for a parking fee on a regular basis • Three or more transaction of the business (e. g. , property sales)

UBI - Rental Income & Interest Income • Rental income from unused spaces & Interest income from funds are not UBI – Rental income to another exempt organizations (tenants) is not taxable – Rental income from property with no mortgage loan is not taxable, regardless of tenants. • if not mortgage-free, then 85% rule applies • Churches are required to pay taxes if annual UBI gross income is more than $1, 000. – An excessive UBI may face revocation of exemption (UBI >50%) -TCM 566(1990)

Form 990 -T

UBI - Book Store • A bookstore income, if convenience of church members, is NOT UBI. • For the bookstore inventory items – Churches need to eliminate all unrelated items from the bookstore, or – The church needs to create a separate subsidiary (a for-profit entity) if the church wants to keep unrelated items (Rev. Ruling 8706012 & Reg 1. 501 (c)3. . 1(e))

Offering Counting - Cash receipts • 5 conditions • At least 2 members count offerings? (pastor or treasurer be not included) • Verify the inside & the outside of the envelopes? • All checks stamped immediately after the contents verified? • Money counters rotated each week? • Donor-restricted funds properly identified during counting offerings?

– 3 conditions Depositing of funds Cash receipts • Are 2 members of the offering counting team in custody of the offering until it is deposited in the bank, placed in a night depository, or in the church’s safe? • Are all funds promptly deposited? Compare offering and other receipt records with bank deposits. • Are all receipts deposited intact? Receipts should not be used to pay cash expenses.

Polity Class Financial Support Services 2. Ministers Taxes & Benefits Rev. K. Young Bae, Ph. D. CFO & Vice President of Finance Association of Unity Churches (816) 524 -7414, young@unity. org Updated 3/6/2008

2. Ministers Taxes & Benefits • AUCI provides consulting services on Ministers’ Tax and Benefits. • AUCI approves and administers Retired Ministers’ Manse Allowance request • Member ministers can opt out from the social security tax with using the AUCI’s Group Tax Exemption number.

An employee or selfemployed for income tax? • All ministers are employees for income tax purpose (Treas. 31 -3401, Rul. 80 -110) – A common-law test to determine employee or self-employed test • In general, a minister is an employee if the church has the legal right to control both what and how work is done. • (e. g. ) A minister is an employee when the church has a right to hire/fire him/her.

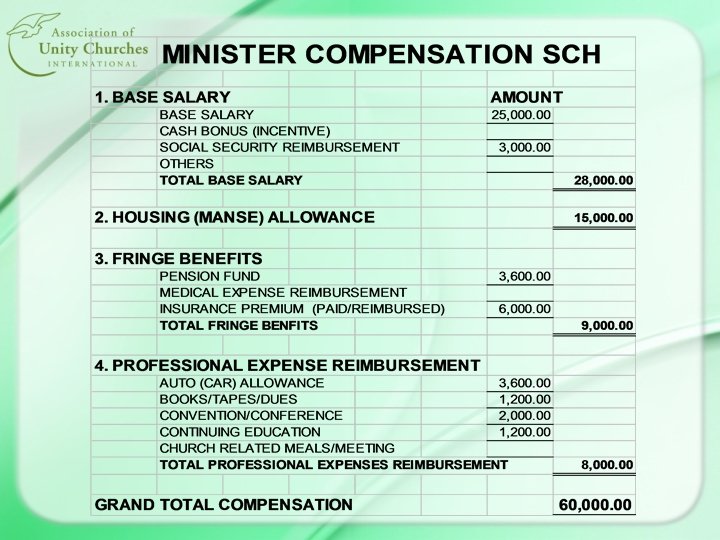

Compensation & taxes (W-2, Box 1 or 1099 MISC, Box 7) (W-2, Box 14)

Form W-2 Base Salary=Gross - Manse $ Blank $ Manse

Form 1099 MISC Base Salary=Gross - Manse Church Name & Address Minister’s Name

Housing (Manse) Allowance • Taxable? – A housing allowance is not taxable for federal income tax, but taxable for social security tax (SECA). Code 107. – A housing allowance includes cash, or a church-provided house. • Can a church designate the full amount of compensation as a housing allowance? (See next screen)

Housing (Manse) Allowance (3 Requirements) – The housing allowance must be designated proactively by the church – Only actual expenses can be excluded from taxable income – The housing exclusion cannot exceed the fair rental value (Rev Ruling 71 -280, 1971) • Exclusion Rules (Treas. Reg. 1. 107 -1 b, Warren v. Commissioner 114 T. C. 2000, Ltr. Rul. 8937025, 835005)

Housing Allowance Worksheet

Housing Allowance Resolution

Deductible Accountable Plan • • The church’s reimbursement (allowance) arrangement must meet all of the following rules: – 1. Expenses must have a business connection; expenses were paid or incurred while performing ministry services.

Deductible Accountable Plan…(continued) – 2. Adequate accounting to the church for expenses with documentary evidence to verify the amount, time, place and professional purpose of each expense, and – 3. Excess reimbursement must be returned to the church.

Deductible Accountable Plan …(continued) – 4. Expenses must be substantiated within 60 days after expenses are paid or incurred. Any excess reimbursement must be returned to the church within 120 days after the expenses are paid or incurred.

Profit/Loss - Schedule C

Social Security Tax • Ministers are subject to SECA tax? (Self Employment Contribution Act) – All ministers pay the full 15. 3% on Schedule SE • The 15. 3% for salary up to $102, 000 for 2008 • Plus 2. 9% tax on all salary above $102, 000 • What Income is Subject to SECA? – Base salary plus housing allowance plus net earning (wedding & class income) minus all unreimbursed expenses

Schedule SE - Social Security Tax

Schedule SE - (continued. . . )

Computing SE Tax Worksheet

Opting out of Social Security • Exemption from SECA (Self Employment Tax). – file Form 4361 by the tax return due date of the second year in which the ministerial income of $400 or more (e. g. , for the class 2008, the filing due date is 4/15/2010) – conscientiously oppose to public insurance because of individual religious considerations – file for other than economic reasons – ordaining body must be a tax-exempt organization (use Association’s tax id: 440668175, GEN 2062)

Form 4361

Social Security Exemption - Losing Benefits? • Does a minister exempted from Social Security lose social security benefits? – Exemption covers only the compensation derived from service as a minister. – Ministers must continue to pay social security taxes for any other non-ministerial incomes even after exempted. – Ministers does not lose any social security benefits earned from non-ministerial services if worked more than 10 years & paid the FICA tax.

Social Security Exemption - Losing Benefits? • One Exception: a minister who opts out by filing a 4361 may not be eligible for SS Disability unless he has contributed into SS within the last 20 quarters. Example ‑ a person works from 20 until 30 years of age and contributes into SS. At 30, the person goes into the ministry and opts out of SS. If they become disabled at 36 (more than 20 quarters away from contributing into SS), they are not eligible for SS Disability or Medicare ‑ until they reach 65 for Medicare or 62 or later for SS retirement.

Advantages of Association’s pension plan • Tax saving with the manse allowance, which is only available through your Association. • Portable - no matter where you go. • Double “watch” by your Association (trustee) & custodians (administrator). – For more details, please visit to www. unity. org.

Pension Assumptions • $500, 000 retirement nest egg • 10% yield each year upon retirement • $35, 000 justifiable housing allowance • 30% marginal tax bracket • Now let’s compare …. . .

In Plan (Association) Out of Plan Investment $500, 000 Yield 10% Yield $50, 000 Manse Allowance Manse not allowed $35, 000 --Taxable Income $15, 000 $50, 000 Tax (reduced to 15% bracket) Tax (30% bracket) $2, 250 Net advantage in plan$15, 000 $11, 750 After tax --

Pension Plan • How much can I contribute annually? – You & your church may contribute up to a total of $40, 000 of "Includible Compensation" per year – However, Contribution by you (payroll reduction agreement): $15, 300 for 2008 – 50+: Catch Up Contribution: $5, 000 for 2008 • A minister's tax-free housing allowance is NOT treated as compensation • Treas. Reg. 1. 415 -2(d)(11)(i) and (ii) & IRS Ruling (PLR 200135045, 2001, EGTRRA 2001 • Therefore, Total Pension Contribution should NOT be more than Net Salary (after housing allowance)

JOIN TO THE MILLIONAIRE CLUB! The more you save, the more you earn. . . Scenario C: Begin at age Yearly contribution Number of years Rate of return “The Dream” 45 $ 7, 500 25 12% Total Contribution $187, 500 Value at Retirement $1, 000, 004