Foreign Exchange Markets Foreign Exchange Market Products and

")

contract is a binding")

entails more than the assumption of")

")

-Bid/ask spread: w. Bid price (買價) -- the price at which")

and arbitrage (套利) An exchange rate between two currencies neither of")

1. 5561 ==> $1. 5561/£ Canadian dollar")

1. 5561 ==> $1. 5561/£ Canadian dollar (in")

Market A - 1£: 1. 5 US$ Market B -1")

- 1. 3008(US$/Euro) w Tokyo -112. 50(")

US$/Euro (€ ) Bid Ask $1. 5019 $1.")

describes capital flows that seek risk-free")

can be created by")

can be constructed by combining")

1. 0432 - 1. 0442 ($/ € ) one month")

1. 0432 - 1. 0442 ($/ € ) one month")

104. 35 - 104. 50 (¥/ $ ) one")

- Slides: 36

外匯市場 (Foreign Exchange Markets)

Foreign Exchange Market Products and Activities w A spot (即期) contract is a binding commitment for an exchange of funds, with normal settlement and delivery of bank balances following in two business days (one day in the case of North American currencies). w A forward (遠期) contract, or outright forward (直接遠期外匯), is an agreement made today for an obligatory exchange of funds at some specified time in the future (typically 1, 2, 3, 6, 12 months).

Foreign Exchange Market Products and Activities w Forward contracts typically involve a bank and a corporate counterparty and are used by corporations to manage their exposures to foreign exchange risk. w A foreign exchange swap (匯率交換) is the simultaneous sale of a currency for spot delivery and purchase of that currency forward delivery. w Foreign exchange swaps can be used by dealers to manage the maturity structure of their currency positions.

Foreign Exchange Market Products and Activities w Speculation(投機) entails more than the assumption of a risky position. It implies financial transactions undertaken when an individual’s expectations differ from the market’s expectation. w Arbitrage(套利) is the simultaneous, or nearly simultaneous, purchase of securities in one market for sale in another market with the expectation of a risk-free profit.

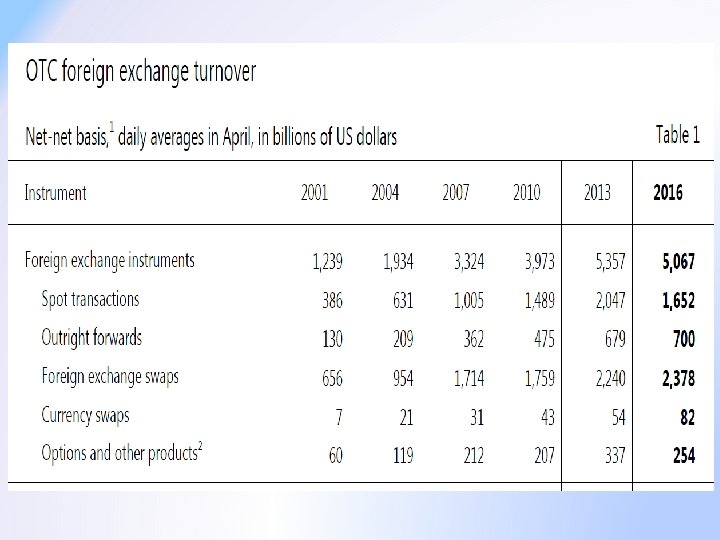

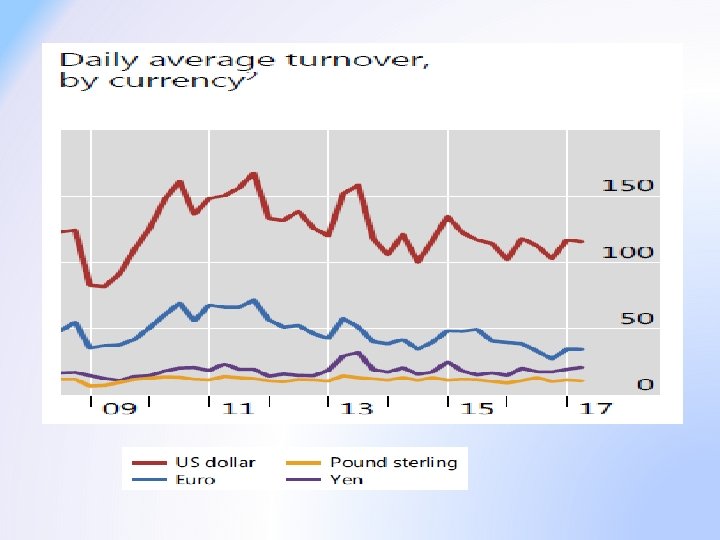

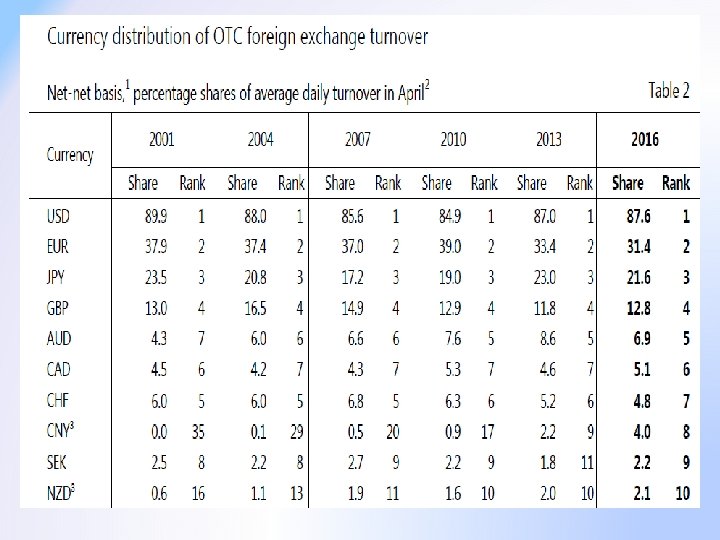

Statistics of Foreign exchange turnover w Data from the 2016 BIS(Bank for international settlements,國際清算銀行) Triennial Survey show that global FX trading has declined. -Trading in foreign exchange (FX) markets averaged $5. 1 trillion per day in April 2016. - This is down from $5. 4 trillion in April 2013. w FX spot trading declined for the first time since 2001, even as activity in FX derivatives(衍生性 商品) continued to increase.

Statistics of Foreign exchange turnover w Bank for international settlements w https: //www. bis. org/publ/rpfx 16. htm? m=6%7 C 35

Exchange rate quotations(匯率報價) -Bid/ask spread: w. Bid price (買價) -- the price at which a marketmaker is willing to buy a currency w. Ask price (賣價) -- the price at which a marketmaker is willing to sell a currency w. The difference between the two prices is referred to as the bid/ask or bid/offer spread, which is often expressed in percentage terms: Percent spread = [(ask price - bid price) / ask price ] x 100 Suppose: $1. 7019 -36 Percent spread = [(1. 7036 - 1. 7019) / 1. 7036] = 0. 1%

Cross rates (交叉匯率) and arbitrage (套利) An exchange rate between two currencies neither of which is the U. S. dollar. A cross rate is usually constructed from the individual exchange rates of the currencies with respect to the U. S. dollar. w Ignoring transaction costs, the prices for any three currencies A, B, & C must be consistent: A A B = C B C

British pound (in U. S. dollars) 1. 5561 ==> $1. 5561/£ Canadian dollar (in U. S. dollars) 0. 7293 ==> $0. 7293/C$ Swiss franc (per U. S. dollar) 1. 2445 ==> SF 1. 2445/$ Japanese yen (per U. S. dollar) 110. 36 ==> ¥ 110. 36/$ German mark (per U. S. dollar) 1. 5142 ==> DM 1. 5142/$ What is the exchange rate between the British pound and the Canadian dollar?

British pound (in U. S. dollars) 1. 5561 ==> $1. 5561/£ Canadian dollar (in U. S. dollars) 0. 7293 ==> $0. 7293/C$ Swiss franc (per U. S. dollar) 1. 2445 ==> SF 1. 2445/$ Japanese yen (per U. S. dollar) 110. 36 ==> ¥ 110. 36/$ German mark (per U. S. dollar) 1. 5142 ==> DM 1. 5142/$ w. What's the exchange rate between the British pound and the Japanese yen?

$ triangular arbitrage (三角套利) Market A - 1£: 1. 5 US$ Market B -1 £: 160 ¥ Market C – 1 US$: 115 ¥ Value of £ in $ £ Value of £ in ¥ Value of ¥ in $ JP ¥ w Cross rate (MKT A & B) – ¥ /US$ = (160 ¥ /1 £) x (1£/1. 5 US$ ) = 160 ¥ / 1. 5 US$ = 106. 67 ¥ / US$ < 115 ¥ / US$ (MKT C) w When the exchange rates of the currencies are not in equilibrium, triangular arbitrage will force them back into equilibrium.

triangular arbitrage Market A - 1£: 1. 5 US$ Market B -1 £: 160 ¥ Market C – 1 US$: 115 ¥ How to arbitrage? (1)Counterclockwise (2) Clockwise

Practice w. Taipei - 88. 080(¥ /US$) - 1. 3008(US$/Euro) w Tokyo -112. 50( ¥ / Euro) How to arbitrage?

w Cross rates with bid/ask spread: Rule: the trader would choose the most advantageous price with each transaction (so you, as a customer, will take the unfavorable of the two prices in each transaction) Example: $1. 5019 -36 per £, $1. 1250 -67 per € What is the direct quote for £? w Example: Bid Ask US$/ British pound (£) $1. 5019 $1. 5036 US$/Euro (€ ) $1. 1250 $1. 1267 € / £ ?

w Example: US$/ British pound (£) US$/Euro (€ ) Bid Ask $1. 5019 $1. 1250 $1. 5036 $1. 1267 (1). Ask rate ( € / £) A customer sells £ for per US$ and gets US$1. 5019 (per £ ) then use US$ to buy €, pays US$ 1. 1267 for per € ==> [1. 5019($/£)] / [$1. 1267($/ € )] = 1. 3350(€ /£) The ask rate: trader's selling price of £ is 1. 3350 € (2) Bid rate ( € / £) Customer sells Euro for $ and gets US$ 1. 1250 (per € ) then use US$ to buy £, pays US$ 1. 5036 for per £ ==> [1. 5036($/£)] / [1. 1250($ / €) ] = 1. 3365(€ /£) The bid rate: trader's buying price of £ is 1. 3365 € w So the bid/ask price : Euro 1. 3350 -65/£.

triangular arbitrage with bid/ask spread Market A - 1. 40 - 1. 41 (US$/ £) Market B - 151 – 155 (¥ / £) Market C – 110 – 112 (¥ / US$) • How to execute triangular arbitrage for this case? • Can triangular arbitrage for this case be profitable?

Covered interest arbitrage w Covered interest arbitrage (拋補套利) describes capital flows that seek risk-free profits based on differences between the forward exchange premium and the relative rate of interest in domestic and foreign currency. (拋補套利是指考量匯率貼水、兩國通貨相 對利率下,資本流動以追求無風險利潤之 套利行為)

w Driven by covered interest arbitrage, the two investments should produce identical ending wealth. w (IRP) % forward premium = % interest differential w The interest rate parity (IRP) condition was developed based on covered interest arbitrage between domestic and foreign currency denominated securities.

Foreign Exchange Market Products and Activities w In the absence of transaction costs, taxes, or default(違約), the price of the two alternatives must be identical: The US$ cost of each €. The price of 1 € for delivery on July 1. The cost of each borrowed US$. € The present value of 1 €.

Foreign Exchange Market Products and Activities w Synthetic forwards (組合式遠匯) can be created by using a spot contract combined with borrowing and lending. w By combining a spot contract with fixed-rate, nperiod borrowing and lending in the two currencies, an n-period forward exchange contract can be constructed.

w Suppose that an investor holds US$ cash and wishes to make a € payment in six months. The investor has two alternatives to choose between (投資者持有美元現金 但未來6個月擬以歐元付款,有下列二方法:) Ø Path 1: Buy € at the six-month forward rate (Ft, 1) for delivery on July 1, and hold US$ assets for six months (earn i$ ) until then. (買遠期歐元,持有美元半年) Ø Path 2: Buy € at the spot rate (St) for immediate delivery, and hold € assets for six months (earn i € ) until July 1. . (買即期歐元,持有歐元半年) In the absence of transaction costs, the two alternatives will be identical. (不考量交易成本時,二交易相等)

Construction of a Synthetic Dollar Security Path 2 - borrow US$ at i$ US$ B Path 1: buy € forward at F (and hold US$ assets for six months ) Path 2 - buy € spot at S € Jan 1 A C D Path 2 -hold € & lend € at i€ Jul 1

w Consider the case in which a manager wishes to own € on July 1. The manager has two alternative strategies to reach his goal. (若一 經理人半年後需歐元,有下列二法) Path 1 - The first strategy has the manager calling a bank to arrange a forward purchase of €. (向銀行買遠期歐元) Þ It will cost (today’s forward rate for delivery in six months) Path 2 - The manager could => borrow US$ for six months (cost - interest rate i$, 6)(借入US$半年) Þ use the borrowed US$ to purchase € at the spot exchange rate (St) (以借入美元去買即期歐元) Þ lend these € for six months (benefit – interest rate i €, 6) (將即期歐元 存入銀行賺利息) € * As the three contracts result in the same ultimate case flows, we can refer to them as a “replicating portfolio” or “Synthetic Forwards”

Suppose the spot rate is 100 ¥ /$, i$, 6 is 6. 5% per annum and i. Yen, 6 is 2. 5% per annum. a. What is your estimate of today's six-month forward rate? b. Suppose the forward is currently quoted at Yen 95/$. What would you do to take advantage of the arbitrage opportunity? Where would you borrow and lend? SOLUTIONS: a. Synthetic Ft = St × (1 + i ¥, 6/2) / (1 + i$, 6/2) = 100 ¥/$ ×(1 + 0. 025/2) / (1 + 0. 065/2) = 98. 0629 ¥/$ b. Borrow in US$, buy ¥ , invest in ¥ securities for six months, and then sell ¥ forward (that is, buy ¥ 95/US$ < Synthetic Ft = 98. 0629 ¥/$) Profit: [$1 × 100 ¥ /$ × (1 +0. 025/2)] / (95 ¥/$) - $1 × (1 + 0. 065/2) = $0. 0333; or 3. 33% gain on transaction Practice: exercise 1

Given: BP£ interest rate 2% $ interest rate 1% spot rate $1. 67/BP£ 1 year forward rate $1. 65/BP£ Synthetic forward = $1. 67 [(1 +. 01) / (1 +. 02)] = $1. 6536/£ > $1. 65/£ = F =>The actual forward rate is higher than the synthetic forward rate: BP £ is undervalued

=> Arbitrage opportunity: combine spot rate and money market, and sell US$ forward w. Borrow £ 1 in London at 2% for a year. w. Convert £ 1 into £ at spot $1. 67/£, get US$1. 67. w. Invest US$ at 1% for a year. You are sure to get US$1. 6876 at end of the year. w. Sell US$ 1. 6876 forward at $1. 65/£, lock in $ amount: $1. 0222. w. Repay £ 1 with 1% interest, left with £ 0. 0122 as profit.

w Synthetic securities (whether an asset or a liability) can be constructed by combining a security denominated in the other currency with a forward contract of similar maturity and a spot contract.

Suppose a Canadian bond portfolio manager wishes to enhance his yield on Canadian short-term bills. Current one-year Canadian TBills yield 6%. The current spot rate is C$ 1. 40/$. The one-year forward rate is C$ 1. 45/$. The US one-year T-Bill rate is 3%. a. What yield could the portfolio manager obtain by creating synthetic Canadian T-Bills? b. What incentive is there in this case in terms of yield enhancement by building a synthetic C$ security? SOLUTIONS: a. 1 + i. C$ = Ft/St * (1 + i$); 1 + i. C$ = 1. 45/1. 40 * (1. 03); which implies that i. C$ = 6. 67%. b. There is a 0. 67% =(6. 67%-6%) yield pick-up before considering the additional transaction costs of the synthetic. Practice: exercise 2

When transaction cost are present, how about the case of Synthetic forwards? ex: spot rate- S ($/Euro) 1. 0432 - 1. 0442 one month forward rate – F ($/Euro) 1. 0448 - 1. 0458 one month i. Euro 3. 0625 - 3. 1875% p. a. one month i. Euro 5. 4375 - 5. 5625% p. a. w Application 1: One-Way Arbitrage è One-way arbitrage is picking the better-priced alternative for a transaction in the presence of transaction costs.

w The firm has payment of € 1 milllion due in 30 days and you want to lock in a price today. Suppose that the manager has access to the same quotes as above. What is the best way for the manager to transact? Ø Path 1 -The manager could travel along path 1 (as figure), first investing his US$ for 30 days and then selling US$ for € at the forward rate. The cost of path 1 is (buy forward) Ø (cheaper) Ø Path 2 -The manager could travel along path 2, first selling his US$ for € at the spot rate and then investing his € for 30 days. The cost of path 2 is (buy spot ) Ø

ex: spot rate (St) 1. 0432 - 1. 0442 ($/ € ) one month forward (Ft, 1) 1. 0448 - 1. 0458 ($/ € ) one month i€ 3. 0625 - 3. 1875% p. a. one month i$ 5. 4375 - 5. 5625% p. a. Application 2: Round-Trip Arbitrage Can you earn arbitrage profits by round-trip arbitrage? 1. borrow US$ and invest € Cost of borrowing US$ (domestic) 1+0. 055625/12 Revenue of investing € (1/1. 0442)(1+0. 030625/12)× 1. 0448 cost/revenue= [1. 0442 ×(1+0. 055625/12)]/[(1+0. 030625/12)× 1. 0448] = 1. 0015 >1 => cost > revenue => cannot earn profit

ex: spot rate (St) 1. 0432 - 1. 0442 ($/ € ) one month forward (Ft, 1) 1. 0448 - 1. 0458 ($/ € ) one month i€ 3. 0625 - 3. 1875% p. a. one month i$ 5. 4375 - 5. 5625% p. a. 2. borrow € and invest US$ Cost of borrowing € (foreign) (1+0. 031875/12) Revenue of investing US$ 1. 0432/1. 0458)(1+0. 054375/12) cost/revenue= [1. 0458 ×(1+0. 031875/12)]/[(1+0. 054375/12)× 1. 0432] = 1. 0006 Þcost > revenue => cannot earn profit Therefore, there is no profit opportunity for both cases. The calculations show that transactions costs preclude the possibility of profitable round-trip arbitrage.

exercise 3: spot rate (St) 104. 35 - 104. 50 (¥/ $ ) one month forward (Ft, 1) 104. 55 – 104. 80 ((¥/ $ ) one month i$ 2. 0625 - 2. 1875% p. a. one month i¥ 0. 4375 - 0. 5625% p. a. Please answer the following questions. a. The firm has payment of US$ 1 milllion due in 30 days. Suppose that the manager has access to the same quotes as above. What is the best way for the manager to transact? How? b. Can you earn arbitrage profits by round-trip arbitrage? How?