Foreign Exchange Rates Exchange Controls Devaluation Foreign Exchange

is the rate")

represents")

- Slides: 10

Foreign Exchange Rates, Exchange Controls & Devaluation

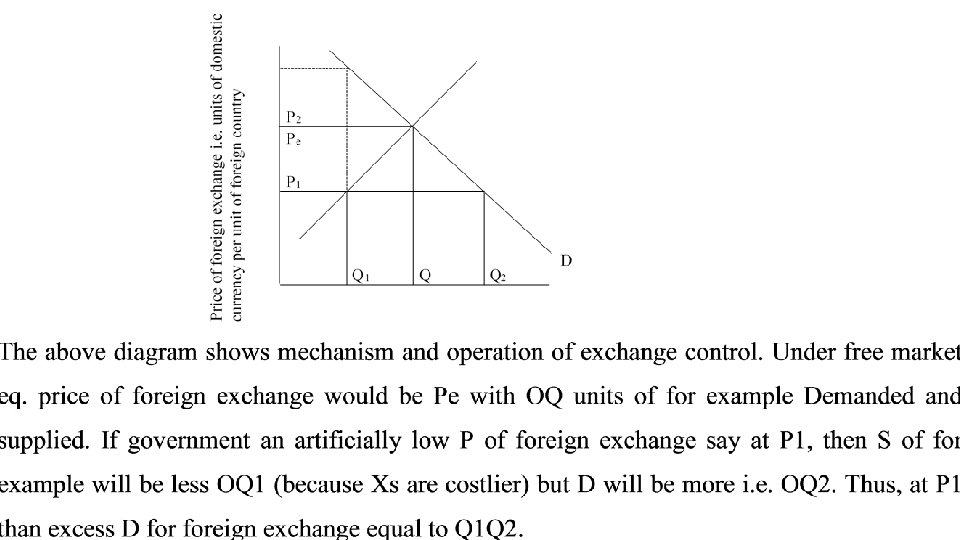

Foreign Exchange Rates, Exchange Controls Ø A country’s official exchange rate(ER) is the rate at which its Central Bank is prepared to exchange its local currency for other countries’currencies in approved for exchange markets - usually quoted in US Dollar. Ø Official Exchange Rates are not necessarily set at or near economic ‘equilibrium’ process for exchange i. e. the rate at which the domestic D for a foreign currency such as $ would just equal its S in the absence of govt. intervention Ø Currencies of most of Dy. Cs are usually overvalued Ø Such a situation which results in excess D over the available S of for. Ex.

In such a situation of excess D, Dy. Cs’ Central Bank have three options. 1. Meet excess D by running down their for ex. Reserves and/or by borrowing from abound - ↑ing their debt. 2. Curtail excess D by pursuing commercial policies and tax measures designed to ↓ D for Ms (e. g. tariff, quota, licensing); and 3. Intervene in for ex market by rationing the limited S of available for ex to “preferred” customers. - Such a rationing device is known as “Exchange Controls” widely used among Dy. Cs.

Ø Some mechanism will have to be devised to ration available S of OQ 1 Ø If govt. auctions it, Mers will be willing to pay a price of P 2, and govt. would make a profit of P 1 P 2 per unit of foreign currency. Ø However, such open auctions are not carried out and limited supplies of for ex are allocated through some administrative quota or licensing device Ø This gives scope of corruption, evasion & emergencies of “black-markets” Ø Question is why have most Dy. Cs opted for an overvalued OER? Ø They have done so as part of widespread programs of rapid industrialization and M-Sub.

Ø Overvalued ER ↓ domestic P of Ms Ø Cheaper Ms esp. of capital and intermediate goods are needed to ↑ industrialization process Ø But overvalued ER also ↓ Ps of Med consumer goods esp. of luxuries, therefore Dy. Cs need to establish; I. M-controls (mostly quotas), or II. A dual ER system - One overvalued ER to be applied to capital and intermediate goods and other lower ER for luxury cons. goods Ms Ø Dual ER system makes domestic P of Med luxury goods very high while maintaining low and subsidized P of capital goods and intermediate goods.

Ø However, dual ER system creates serious problem of administration and promotes corruption Ø Overvalued currency ↓es return to local Xers and M-competing inds. which are not protected by tariffs or quota Ø In the absence of X-subsides, Xers mostly farmers become less competitive in World Market as Ps of their products are artificially ↑ed by overvalued ER Ø In the absence of effective govt. regulation of the for ex dealings overvalued ERs have a tendency to aggravate Bo. P problem because they cheapen Ms, while making Xs costlier

ØChronic Bo. P deficit of current A/C can be ameliorated through devaluation. ØDevaluation by ↓ing foreign currency P of its Xs and ↑ing domestic currency P of Ms helps to improve trade balance of Dy. Cs ØAn alternative to devaluation is to allow for ex rates to fluctuate freely in accordance with changing conditions of IN demand supply Ø Flexible ERs in the past were thought not to be desirable esp. in Dy. Cs heavily dependent on Xs and Ms, because they are ; (i) extremely unpredictable, (ii) subject to wide and uncontrollable fluctuations, and (iii) susceptible to foreign and domestic currency speculation ØSuch unpredictable fluctuations can wreak havoc with both short and longrun development plans Ø Despite, this a no. of Dy. Cs like Mexico, Argentina, Chile, Philippines etc. adopted free floating ER to correct Bo. P deficit and prevent capital flows.

Ø Present IN system of floating ER (legalized at 1976 Jamaica IMF meeting) represents a compromise between a fixed and fully flexible ER systems. Ø Under this managed floating ER system major IN currencies are permitted to fluctuate freely, but erratic swings are limited through Central Bank intervention Ø Most Dy. Cs have decided to continue to peg their currencies to those of Dd. Cs Ø Some like Kenya, have decided to tie their currencies to the movements of a weighted index of the World’s major currencies Ø Devaluation has the immediate effect of ↑ing Ps of Med goods in term of the local currency Ø If as a result of these higher Ps, domestic workers seek to preserve the real value of their purchasing power, they will demand ↑ in wages & salaries, which will ↑ production cost and tend to ↑local prices even higher. Ø This will lead to wage-price spiral of domestic inflation. Ø This will also lead to ↑ in Ps of Xs worsening Bo. P Ø Thus devaluation could ↑ Bo. P problem while generating galloping inflation domestically

Ø Experience of many L. American countries esp. chronic and uncontrollable inflation has made them reluctant to use devaluation despite pressures for IMF and Western Countries Ø Devaluation is likely to affect income distribution also Ø It creates incentives for production of Xs as opposed to domestic goods Ø In general, those who do not participate in the X-sector stand hurt and Xers and businessmen engaged in foreign trade stand to benefit most Ø Though we cannot categorically say that devaluation tends to worsen income distribution, we may conclude that greater ownership and control over X-sector by private sector as opposed to the public, greater is likelihood that dev. will have an advance effect on income distribution Ø For this reason, among others, IN financial and commercial problems (e. g. Chronic Bo. P deficit) cannot be divorced from domestic problems (poverty & inequality). Ø Policy responses to alleviate one problem can either improve or worsen other