Efficiency and the Internal Capital Markets in the

on insurer's efficiency")

• Mergers and acquisitions in")

- Slides: 19

Efficiency and the Internal Capital Markets in the U. S. Property-Liability Insurance Industry Ji Yun Lim Temple University 18 th APRIA Annual Conference Moscow State University, Russia

Motivation • Questioning the influence of the internal capital markets (ICM) on insurer's efficiency • Powell, Sommer, and Eckles (2008) • Positive relationship between the investment decision of affiliated insurers and internal capital transfers in the U. S. P-L insurance industry is found • Internal capital markets are being utilized to transfer capital to affiliates with the best perceived investment opportunities • Most of the internal capital market studies are focused on the existence of the active internal capital markets and their activities • Many studies about efficiency in insurance industry examine the relationship of efficiency to the organizational form, corporate governance, and market structure • Few studies regarding the relationship between the utilization of internal capital markets and the firm's efficiency

Objective • Assumption • Internal capital market activity exists in the U. S. P-L insurers • Objective of this study • To determine whether utilizing the internal capital market is beneficial for the U. S. P-L insurers to operate efficiently and ultimately maximize firm value • Why the U. S. property-liability insurance industry? • Insurers are required to report the transactions among affiliates • Insurer groups are prevalent • Grouping structure creates an active internal capital market within the group, letting the holding company allocate capital among affiliated insurers

Literature Review – ICM • Many studies question whether or not the internal capital market is active and whether it is efficient if it is proven to be active • Mixed results among prior studies regarding the internal capital markets • Shin and Stulz (1998) and Rajan, Servaes, and Zingales (2000) • Transferring capital to and from affiliates could create an additional layer of information asymmetry between insurer and policyholders and shareholders • Internal capital market activity is not an economically significant factor in the investment strategy for conglomerate firms • Scharfstein and Stein (2000) • Internal capital markets may be less efficient than external capital markets • It may lead to value destroying cross-subsidization among divisions • Stein (1997) • Incentives to establish internal capital markets may be the greatest among firms that are narrowly focused and whose assets present difficulty in valuation

Literature Review - ICM • Some empirical studies have found support for the hypothesis that ICMs are active and play a meaningful role in the operations of financial intermediaries • Gertner, Scharfstein and Stein (1994) • Conglomeration may improve financial efficiency by creating internal capital markets • It is easier to efficiently redeploy the assets of poorly performing projects • Internal capital markets are less affected by capital market frictions • Khanna and Tice (2001) • Active and significant internal capital markets in discount retailing industry, focused industry without high levels of information asymmetry • Campello (2002) • Internal capital markets tend to play an efficiency-enhancing role in large bank holding companies

Literature Review - Efficiency • The main stream of efficiency studies in insurance industry has been organizational form, corporate governance and mergers and acquisitions • Cummins, Weiss and Zi (1999) • Stock and mutual are operating on separate production and cost frontiers • Stock cost frontier dominates the mutual cost frontier for the majority of both stock and mutual firms • Cummins, Tennyson and Weiss (1999) • Acquired firms achieve greater efficiency gains than firms that have not been involved in mergers or acquisition in the life insurance industry • Use DEA and the Malmquist methodology

Literature Review - Efficiency • Cummins and Xie (2008) • Mergers and acquisitions in P-L insurance were value-enhancing • Acquiring firms achieve more revenue efficiency gains than non-acquiring firms and target firms experience greater cost and allocative efficiency growth than non-targets • Choi and Weiss (2005) • Examine the relationship between the market structure and revenue and cost efficiency in P-L insurance industry • Cost-efficient firms charge lower prices and earn higher profits • Prices and profits are found to be higher for revenue-efficient firms

Hypothesis • Efficiency scores of the U. S. P-L insurers are related to the internal capital transactions • If transferring capital via internal capital markets facilitates insurer to minimize costs conditional on output levels produced and input prices, the relation of cost efficiency to the internal capital markets would be statistically significant • Two-stage DEA approach • Estimate the insurers' cost efficiency using data envelopment analysis (DEA) • Regress the efficiency scores on the proxy for internal capital market activity

Methodology - 1 st stage: DEA • Two primary frontier efficiency methodologies • Stochastic frontier analysis (SFA) • Data envelopment analysis (DEA) • In this study, the DEA method will be used because DEA is nonparametric, thus avoiding misspecification of functional form or the probability distributions assumed for the error terms • The proxy measures for the quantity and price follow the definitions in Cummins and Weiss (2012) • Insurers provide three principal services • Risk-pooling and risk-bearing • Real financial services relating to insured losses • Financial intermediation

Methodology - 1 st stage: DEA Outputs Three principal services Output Proxy Quantity Lines of business Price Risk pooling and risk Present value of real The difference of bearing losses incurred premiums earned and the present “Real” insurance value of losses services incurred divided by the present value of losses incurred Financial intermediation Average invested assets of a firm Expected rate of return on the insurer’s assets • Personal short-tail losses, • Personal long-tail losses, • Commercial shorttail losses, • Commercial longtail losses

Methodology - 1 st stage: DEA Inputs Category Quantity Price Administrative labor Sum of expenses associated with home office labor: salaries + payroll taxes + employee relations and welfare Real national average weekly wage rate for property–liability insurers (SIC code 6331) Agent labor Net commissions + brokerage fees + allowances for agents Average weekly wage rate for insurance agents (SIC 6411) Business services and materials Sum of all non-labor expenses Average weekly wage rate for business services (SIC 7300) Financial equity capital Average of the beginning and end-of-year equity capital Average 90 -day Treasury bill rate in year t + the long-term average market risk premium on large company stocks Policyholdersupplied debt capital Loss reserves + unearned premiums reserves Total investment income minus expected investment income from equity divided by average debt capital

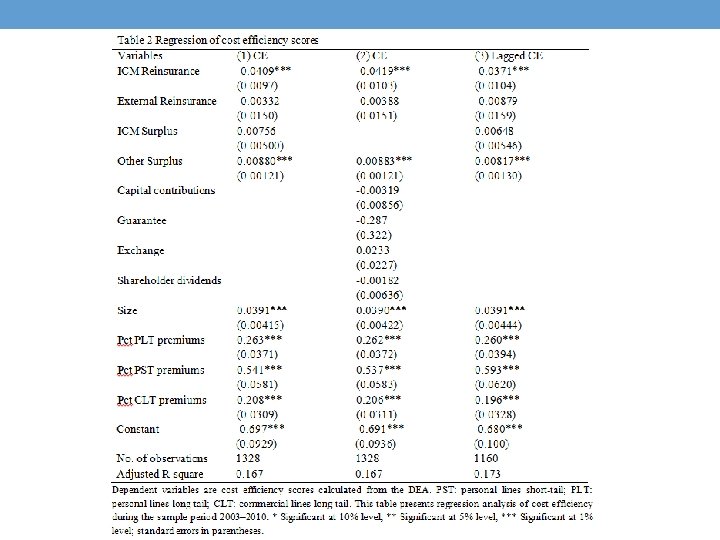

Methodology - 2 nd stage: Regression • Efficiency scores from the 1 st stage are regressed on • Internal capital market activity in the group • ICM Reinsurance • ICM Surplus • Capital transactions other than internal capital market activity • External Reinsurance • Other Surplus • Firm characteristics • Size • Proportion of personal long tail, personal short tail, commercial long tail, commercial short tail line of business

Key Variables • ICM Reinsurance* : the ratio of net ceded reinsurance among affiliates divided by net premiums written • External Reinsurance : the ratio of net ceded reinsurance to and from non-affiliates divided by net premiums written • ICM Surplus** : the sum of four types of the internal capital transactions divided by net premiums written • Shareholder dividends paid to affiliates • Capital contributions • Guarantees made on behalf of affiliates • Capital exchanged when one affiliate purchases, sells or exchanges an asset from another • Other Surplus : the total surplus minus ICM Surplus divided by net premiums written *The Underwriting and Investment Exhibit Part 2 B - Premiums Written in the NAIC P-L regulatory annual statements **The Schedule Y-Part 2 Summary of the Insurer's Transactions with any Affiliates in the NAIC P-L regulatory annual statement

Data • Main source of data is the NAIC annual statements • Sample period of 2003– 2010 • Decision making units used in DEA are defined as groups consisting of at least two affiliates • The data needed for DEA estimation is summed up by group code • Excluded insurers with • Zero or negative net worth, premiums, or inputs • Less than $1. 5 million in assets

• The final sample accounts for approximately 84% of total property-liability insurance industry assets

Summary • Conclusion • Groups cede more reinsurance within affiliates than they assume are expected to have higher cost efficiency than those do not • Internal capital transactions except internal reinsurance have no influence on the cost efficiency of insurers • In the future work • Revenue and profit efficiencies • Two-stage least square regression using the rank of efficiency scores as an instrument (Weiss and Choi, 2008)

Thank you