Your Home Your Value A simplified approach to

• If values meet required levels, an entry will be issued")

- Credit = Tax – The tax")

- Slides: 26

Your Home, Your Value A simplified approach to understanding your county’s home valuation process. Presented by Rhonda Eddy, Allen County Auditor

Why Reappraise? • Ohio Constitution requires real property to be appraised at market value • Ohio Constitution also requires real property to be taxed by “uniform rule. ” = all taxpayers receiving a service must pay the same rate of taxation for that purpose. • Counties revalue according to a schedule set by the Department of Taxation.

2009 REAPPRAISAL COUNTIES • • • ALLEN SANDUSKY COSHOCTON VINTON GUERNSEY

2009 UPDATE COUNTIES • • • BELMONT BROWN CRAWFORD CUYAHOGA ERIE FAYETTE HIGHLAND OTTAWA STARK WARREN HURON JEFFERSON LAKE LORAIN LUCAS MORGAN MUSKINGHAM PORTAGE WILLIAMS

Understanding the home valuation process 1. Collection 2. Analysis 3. Setting 4. Feedback 5. Review 6. Finalization

1. Collection • Reappraisals happen every six years • Orders to reappraise issued two years prior to the scheduled reappraisal. – We have been working on the reappraisal since 2007. • Reappraisal requires that each property must be viewed by the auditor or his representative. – Ensures land improvements are correctly noted for tax purposes. • County Auditor may contract for the services of a professional appraisal firm – Firm must register with the Tax Commissioner before a contract can be signed. – Registration is for disclosure purposes

2. Analysis • Establish neighborhood boundaries • Reviews historic trends and actual sales over last three years • Determine estimated fair market value of properties.

3. Setting • Market value is the price that would be paid by a willing seller to a willing buyer. • Determination includes analysis of property sales, rental income, and other economic factors. • Ohio requires full disclosure of sales prices to facilitate the assessment of real property. • Mechanism is Conveyance Fee and Transfer Tax.

4. Feedback • Notices are mailed upon completion of property valuations • All records are made available for public inspection. • Face-to-face meeting with an appraiser and/or county representative to discuss their valuation.

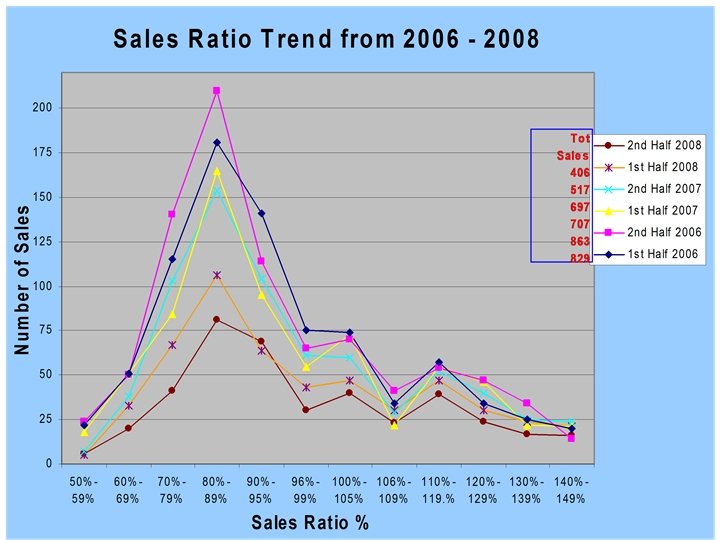

5. Review • DTE reviews the proposed values and conducts a sales ratio study. • Compares sales from the year preceding the tax lien date to the proposed values. • Sales have been screened for validity. • Questionable sales are removed from the study. • DTE also compares aggregate value changes by class with changes in the value of properties considered in the ratio study.

5. Review (con’t) • If values meet required levels, an entry will be issued accepting the values listed on the tentative abstract. • If values do not meet required levels, DTE will contact the county to discuss required adjustments. • The Tax Commissioner may order the necessary changes if no agreement can be reached.

6. Finalization • Values are aproved by DTE. • Tax Rates are set by DTE. • Tax bills are printed. • Taxpayer has right to file for a Board of Revision Hearing. 1 st Monday in Jan to March 31 st, 2010.

How do I provide feedback to my county auditor? Some homeowners may wonder when it is appropriate to provide feedback about their valuation. Some of the questions to consider are: 1. Have we missed something when your home was reviewed that might change your valuation? 2. Would you sell your home for the current appraised value of the property? Homeowners who have questions or concerns about their valuation have the opportunity to provide feedback to a county representative to discuss their valuation and request that changes be made. Property owners can appeal informally or formally. The informal hearings allow homeowners to meet with the appraiser and correct any mistakes or raise any questions. This informal process saves you time and money by not filing a formal appeal; although the formal appeal route can serve their needs as well. Either avenue leads to fair play for property owners.

What are your responsibilities as a homeowner? 1. Understand the process by reviewing the materials available to you or visiting our web site for more information. 2. Report any changes or discrepancies to your auditor since your last valuation. 3. Provide feedback to your auditor about your valuation to ensure its accuracy.

TAXES How does my valuation affect my taxes? Two primary components make up a property tax bill: 1. The first component includes the various tax rates, which are requested by taxing authorities, such as school districts, park districts, townships, villages and city councils and approved by the voters. 2. The second component is the assessed value of one’s property. A third component may include special assessments submitted from municipalities, townships and counties.

Basic Taxation Formula • (Base x Rate) - Credit = Tax – The tax base is appraised value – The tax rate is expressed in mills • 1 mill = $1. 00 per $1, 000 of taxable value – Examples of tax credits include reduction factors and rollbacks

Where does your tax money go? • • 72% School Districts 13% Townships/ Municipalities 1% Park District 5% County General Fund 5% MRDD 1% Tri-County Mental Health 2% Children Services 1% Senior Services

How is the Tax Rate Determined? • Most mills are approved by voters; • Some mills are levied without voter approval – this is called inside or unvoted millage. • Average tax rate is well over 50 mills, so most rates have been approved by voters. • Inside millage cannot exceed 10 mills as it is applied to any individual property.

Tax Reductions • The Department of Taxation reviews the levies and valuations each year to adjust the effective rate so that an entity cannot receive more than they should per the voted millage or set amount.

Voted Levies Fixed Rate Levy = Voter is voting on # of mills that will be charged against value. (Police, Fire, Permanent Improvement, Current Expense levies). As values change the DTE changes the rates (effective rate) so that the entity will never receive more money than the first year the levy was collected. New construction is not included in the effective rates. Rate * Value = Amount

Voted Levies Fixed Sum Levy = Voter is voting on set amount of money, no matter what the valuation. (Emergency & Bonds levies for schools) As property values decrease or increase, the amount to be collected is spread out among all the property owners in that school district. Amount / Valuation = Rate

Tax Credits Available Owner-occupancy Owner-occupied homesites are entitled to a 2. 5% tax rollback. Homestead Exemption Homeowners who are at least 65 years old or permanently disabled may be eligible for the Homestead Exemption. Agricultural Use Value Program (CAUV) The Current Agricultural Use Value program exists for eligible commercial agricultural property. Property damage Reporting damaged or destroyed property may reduce its appraised value.

Calculation of a Property Tax Bill Market Value of Home Taxable Value (35% of $100, 000) $100, 000 $35, 000 Effective Tax Rate (reduced tax rate) 42. 87 Mills Effective Tax (. 04287 Mills X $35, 000) $1, 500. 45 Subtotal (Before any tax credits) $1, 500. 45 10% Rollback (. 1 X $1, 500. 45) 2 ½% Rollback (. 025 X $1, 500. 45) Net Tax Due -150. 04 -37. 51 1, 312. 90

The value of your home is related to the amount of tax you pay… However…. It is not a direct correlation of the taxes you pay. If your value drops 10%, it doesn’t mean your taxes drop 10%. If your value increases 5%, it doesn’t mean your taxes increase 5%.

For more information: County web site www. allencountyohio. com/auditor Your home, your value web site www. Your. Home. Your. Value. org Property valuation feedback (419) 228 -3700 x 8794 Rhonda Eddy, Allen County Auditor 301 N. Main St, Room 105 Lima, OH 45801 (419) 228 -3700 x 8794 phone (419) 222 -2543 fax reddy@allencountyohio. com email