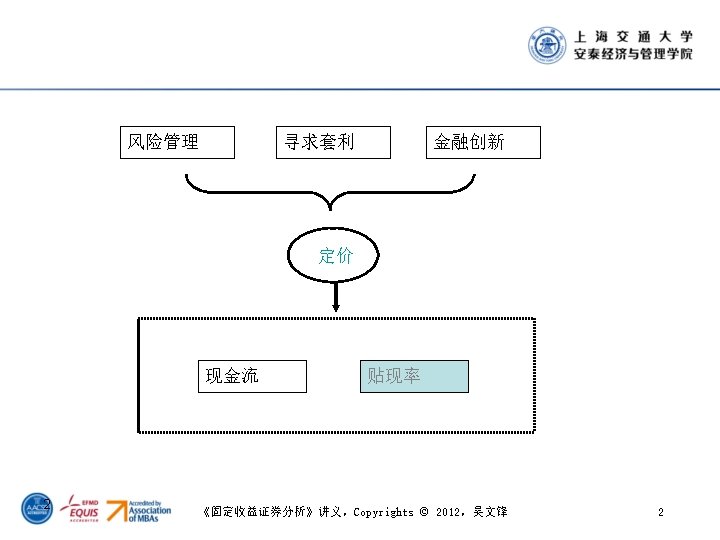

Time value of money Present value Future value

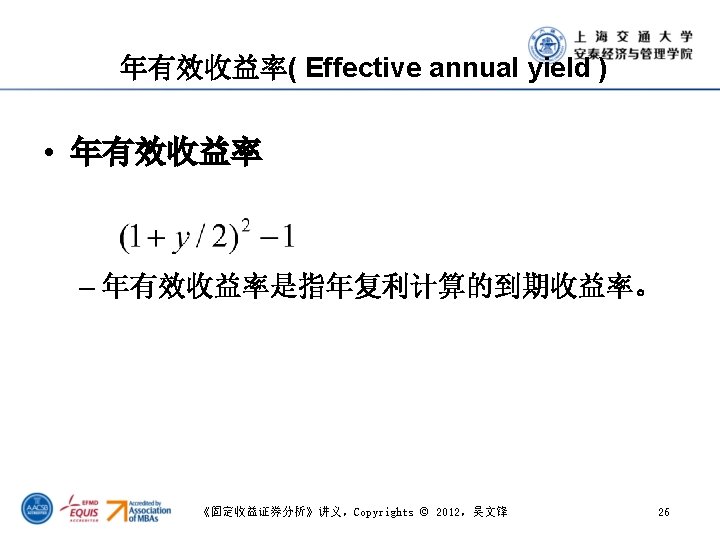

• 终值 ( Future value)")

Dirty Price Average(RMB) Years Yield to to Maturity( Maturity")

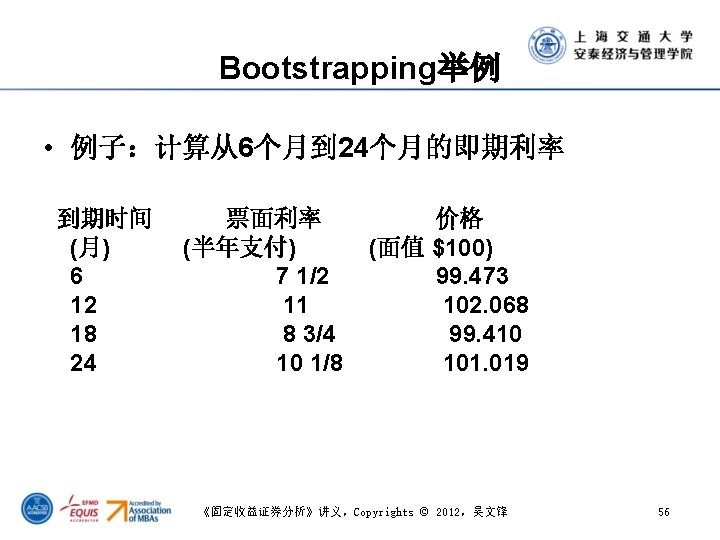

(半年支付) (面值 $100) 6 7 1/2 99. 473")

调整后( 大型金 融机构) 调整幅 度 调整前(中 小金融机构 )")

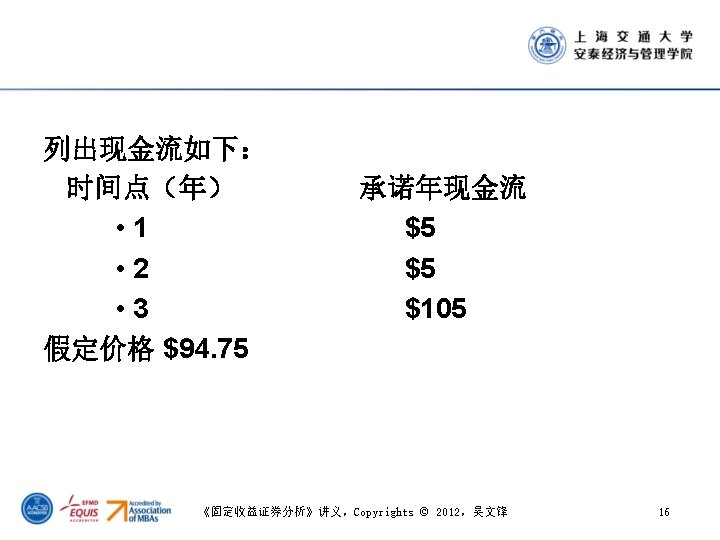

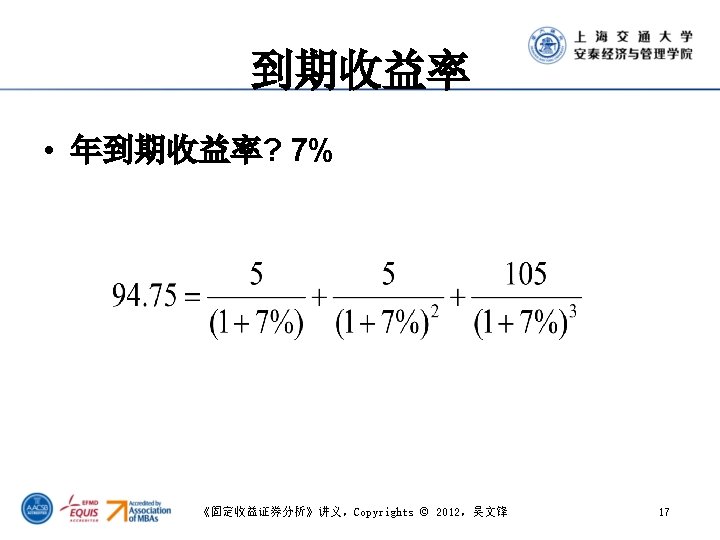

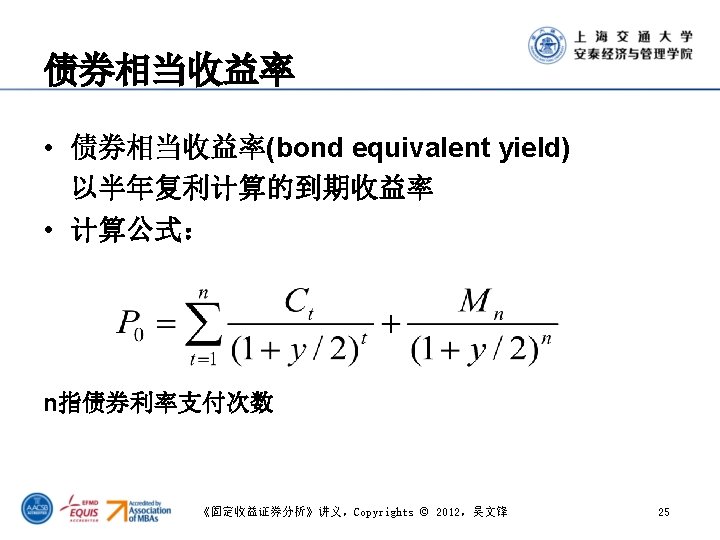

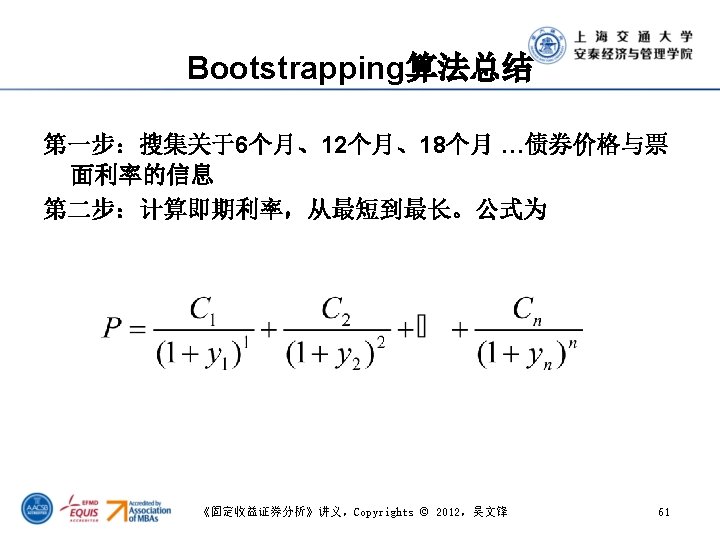

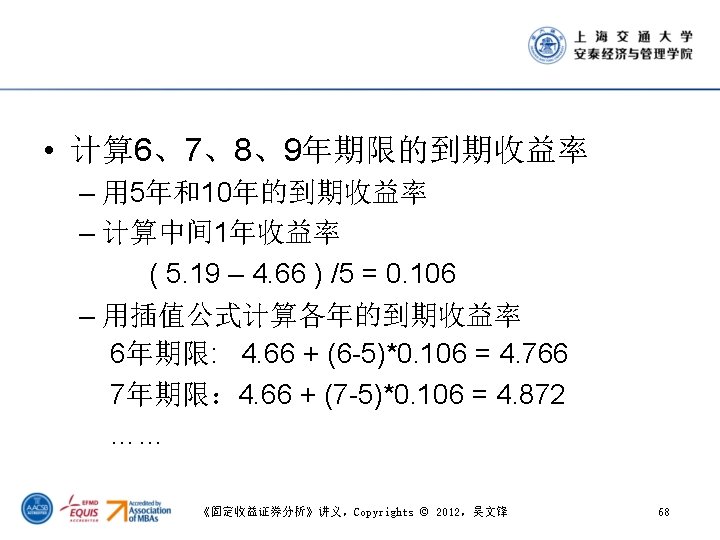

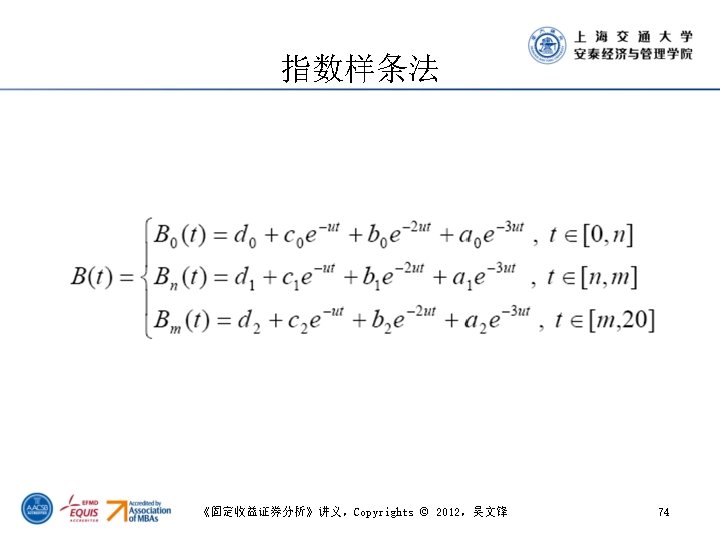

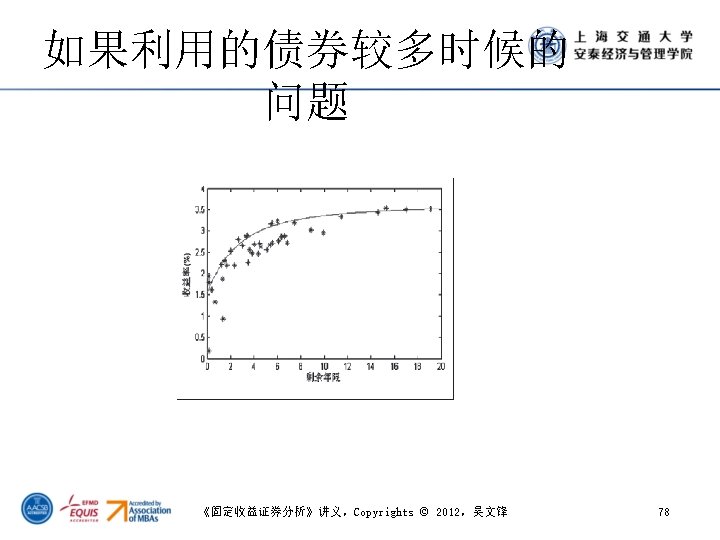

- Slides: 125

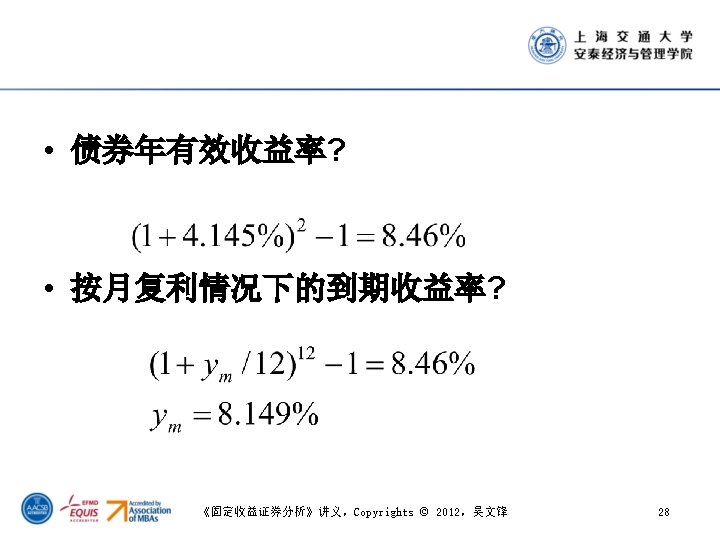

Time value of money • 现值 ( Present value) • 终值 ( Future value) • 单利和复利 8 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 8

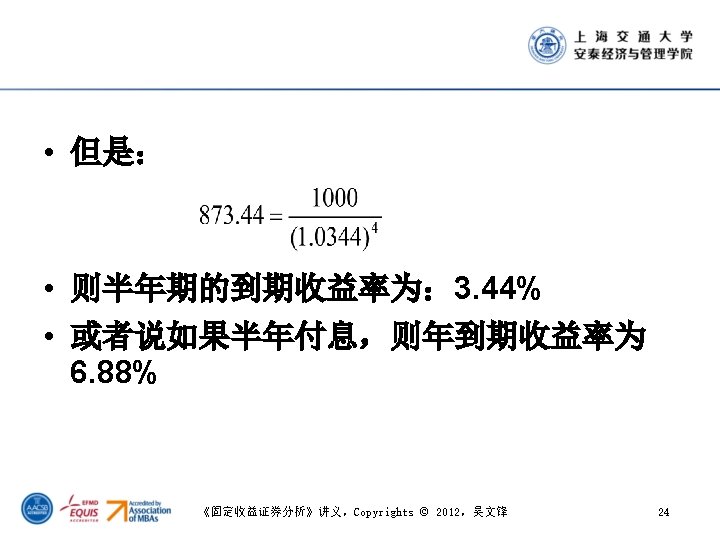

Zero Coupon Bond’s YTM • Price of a 2 -year zero coupon bond is 873. 44,where par value is 1000. 由于: 所以:YTM 为 7% . 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 23

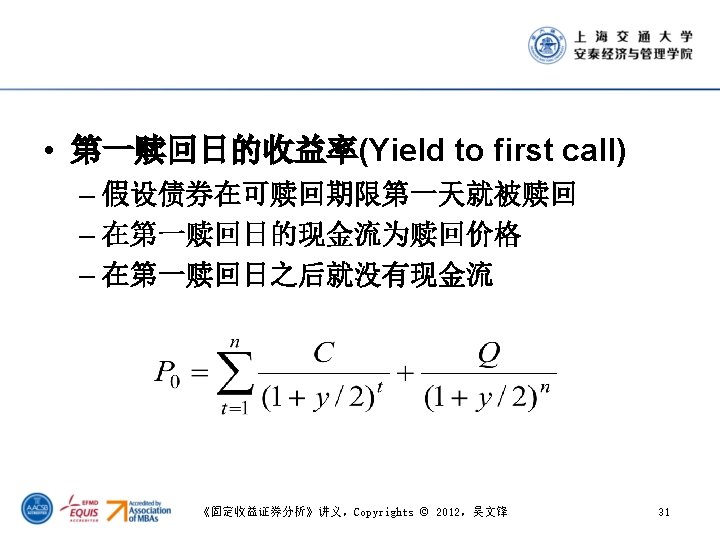

Example • P = 105, C = 5, F = 100, n = 40 YTM = 9. 44% • 如果 5年后按面值赎回, Yield to first call = 8. 74% 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 32

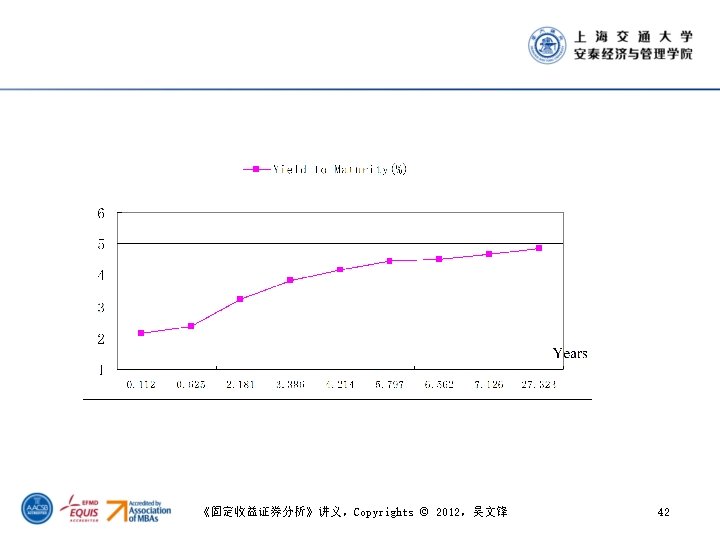

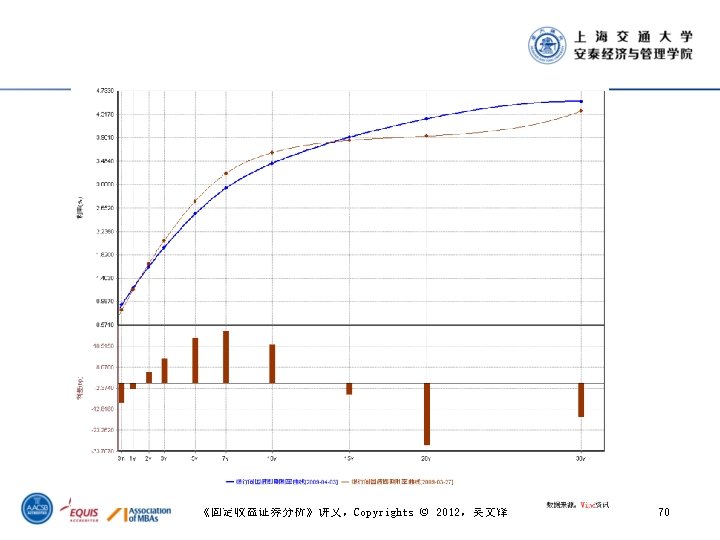

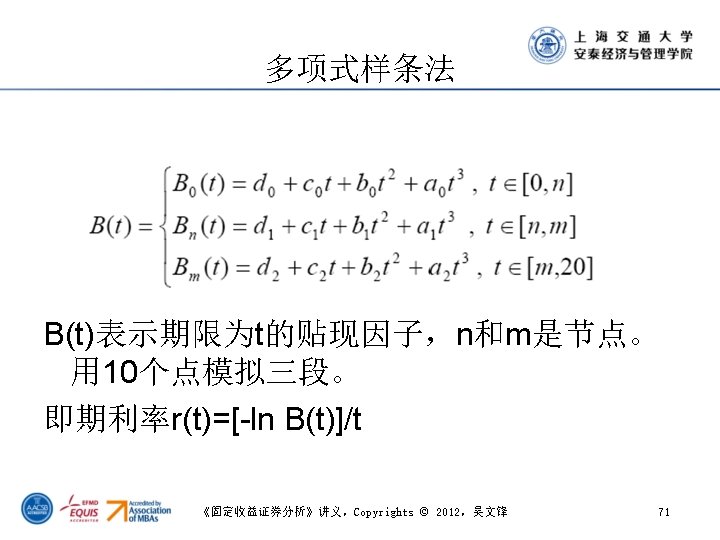

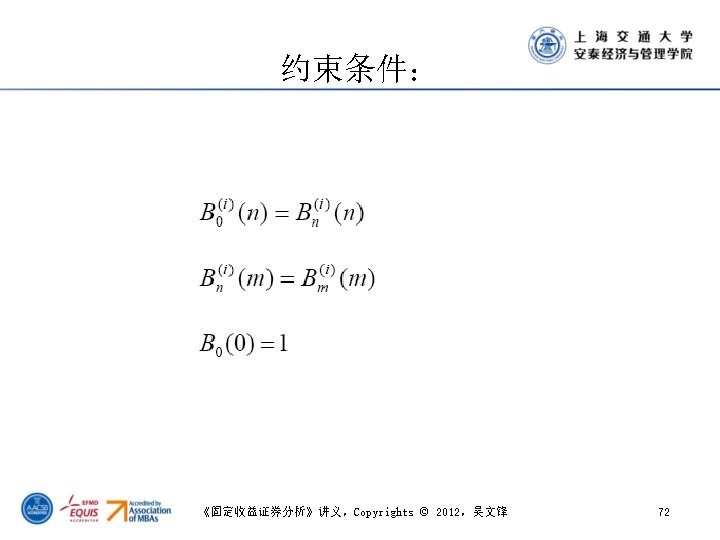

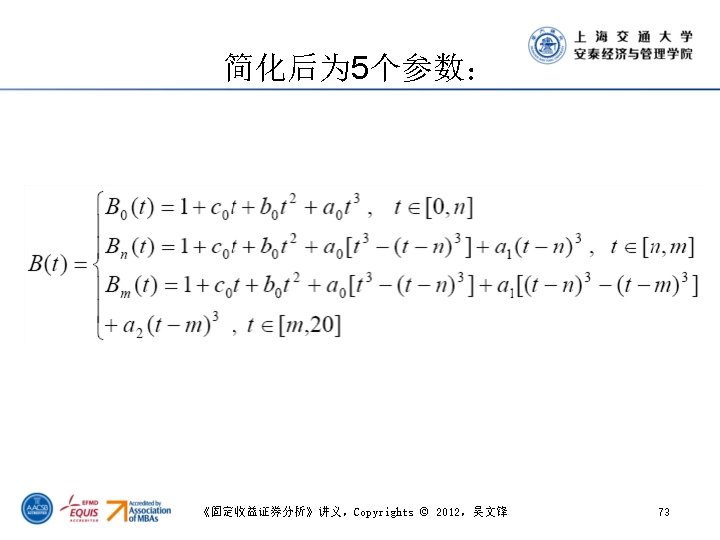

3. 2 利率期限结构及其构造 净价平均价格( 元 )Dirty Price Average(RMB) Years Yield to to Maturity( Maturity %) (year) 债券简称 债券代码 本期平均价 格(元) Accrued Interest (RMB per 100 RMB per value) 04国债 01 040001 99. 758 0. 000 99. 758 0. 112 2. 1570 02国债 12 020012 100. 813 0. 863 99. 950 0. 625 2. 3610 04国债 02 040002 102. 570 2. 621 99. 948 2. 181 3. 2210 01国债 05 010005 101. 902 2. 287 99. 615 3. 386 3. 8280 04国债 03 040003 104. 477 3. 488 100. 989 4. 214 4. 1550 03国债 11 030011 95. 929 0. 719 95. 210 5. 797 4. 4540 04国债 07 040007 103. 198 2. 078 101. 120 6. 562 4. 5040 02国债 01 020001 90. 775 2. 375 88. 400 7. 126 4. 6500 02国债 05 020005 71. 061 0. 556 70. 505 27. 323 4. 8660 41 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 41

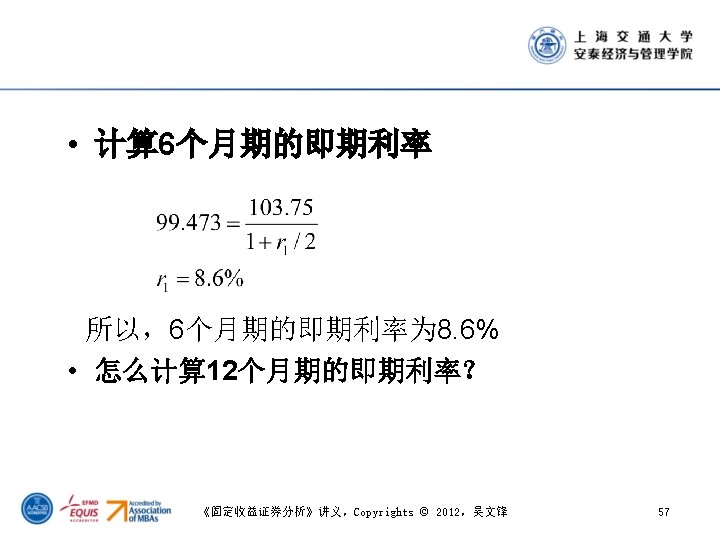

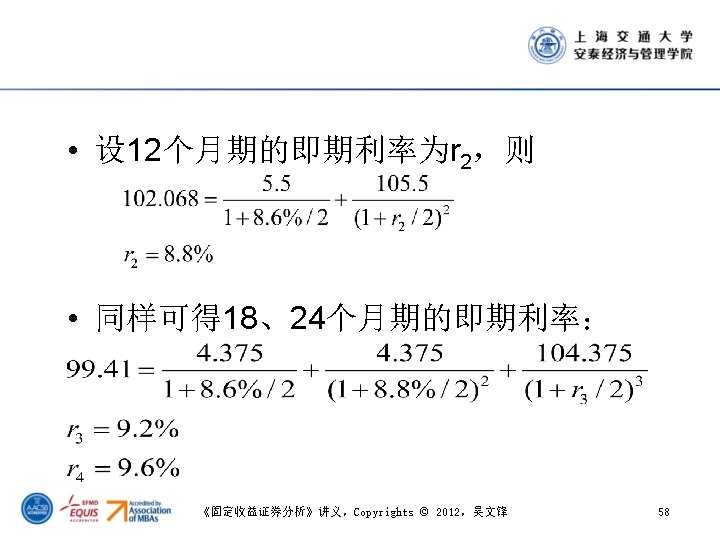

到期时间 票面利率 价格 即期利率 d (月) (半年支付) (面值 $100) 6 7 1/2 99. 473 8. 6% 0. 9588 12 11 102. 068 8. 8% 0. 9175 18 8 3/4 99. 410 9. 2% 0. 8738 24 10 1/8 101. 019 9. 6% 0. 8295 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 60

用于Bootstrapping的几种国债类型 1、on-the-run treasury 2、on-the-run and selected off-the-run treasury 3、all treasury coupon securities and bills 4、treasury coupon strips 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 62

1、on-the-run treasury Advantage: – Uses only the most accurately priced issues. Disadvantage: – Large maturity gaps after the 5 -year note. 2、on-the-run and selected off-the-run treasury Disadvantages: – Still doesn't use all issues – may be distorted by the repo market 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 63

3、All Treasury coupon securities and bills Advantage: – Does not ignore information from issues excluded by other approaches. Disadvantages: – Some maturities have more than one yield – current prices may not be available for all maturities. 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 64

4、Treasury coupon strips Advantage: – Intuitive approach that does not require bootstrapping to derive spot rates. Disadvantage: – Liquidity premium and tax law impact observed rates. 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 65

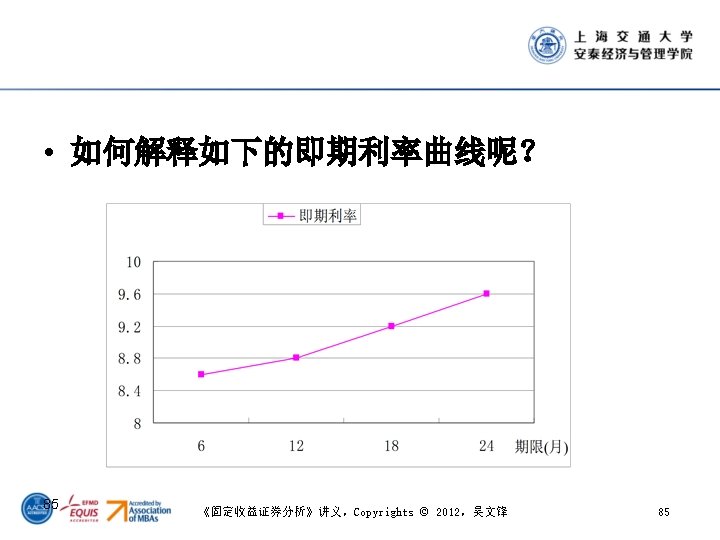

3. 3 利率期限结构的理论解释 • Treasury Yield Curve – Upward sloping, normal yield curve – Downward sloping – Flat – Humped 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 81

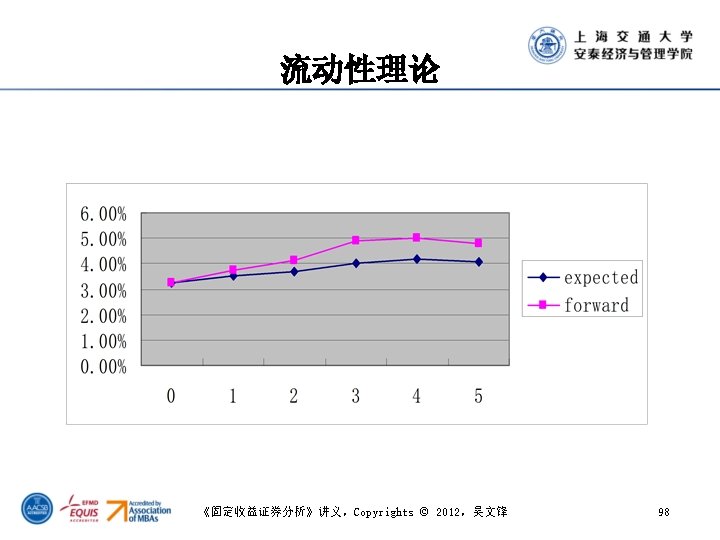

Term Structure Theory Expectations Hypothesis Pure Expectations Liquidity Theory Market Segmentation Biased Expectations Preferred Habit 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 83

总结: b. e. y 债券相当收益率 贴现率 --贴现因子 YTM Effective annual yield Yield to first call Yield curve Spot rate curve 线性插值 Bootstrapping 无偏预期理论 Term Structure Theory 流动性、偏好 市场分割 《固定收益证券分析》讲义,Copyrights © 2012,吴文锋 102

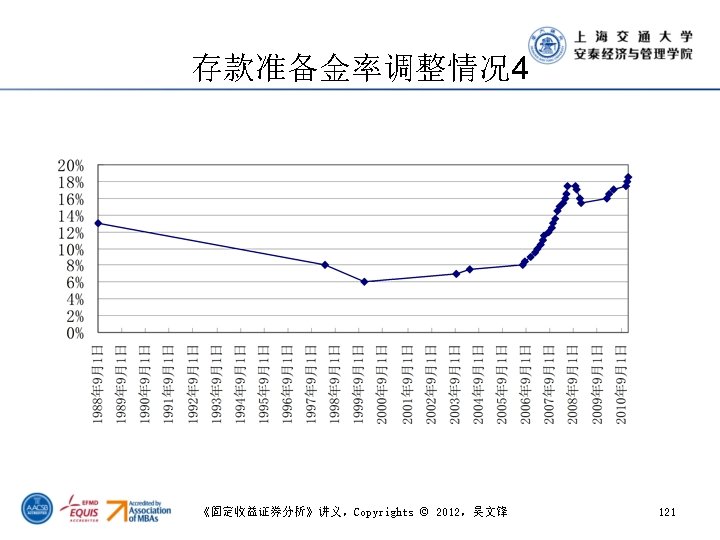

存款准备金率调整情况 1 时间 调整前( 大型金 融机构) 调整后( 大型金 融机构) 调整幅 度 调整前(中 小金融机构 ) 调整后 调整幅 度 2010年 12月 20日 18. 00% 18. 50% 0. 5 14. 50% 15. 00% 0. 5 2010年 11月 29日 17. 50% 18. 00% 0. 5 14. 00% 14. 50% 0. 5 2010年 11月 16日 17. 00% 17. 50% 0. 5 13. 50% 14. 00% 0. 5 2010年 5月10日 16. 50% 17. 00% 0. 5 13. 50% 0 2010年 2月25日 16. 00% 16. 50% 0. 5 13. 50% 0 2010年 1月18日 15. 50% 16. 00% 0. 5 13. 50% 0 2008年 12月 25日 16. 00% 15. 50% -0. 5 14. 00% 13. 50% -0. 5 2008年 12月 05日 17. 00% 16. 00% -1 16. 00% 14. 00% -2 2008年 10月 15日 17. 50% 17. 00% -0. 5 16. 50% 16. 00% -0. 5 2008年 09月 25日 17. 50% 0 17. 50% 16. 50% -1 118

存款准备金率调整情况 2 时间 调整前 调整后 调整幅度 2008年 06月 07日 16. 50% 17. 50% 1 2008年 05月 20日 16% 16. 50% 0. 5 2008年 04月 25日 15. 50% 16% 0. 5 2008年 03月 18日 15% 15. 50% 0. 5 2008年 01月 25日 14. 50% 15% 0. 5 2007年 12月 25日 13. 50% 14. 50% 1 2007年 11月 26日 13% 13. 50% 0. 5 2007年 10月 25日 12. 50% 13% 0. 5 2007年 09月 25日 12% 12. 50% 0. 5 2007年 08月 15日 11. 50% 12% 0. 5 2007年 06月 05日 11% 11. 50% 0. 5 119

存款准备金率调整情况 3 时间 调整前 调整后 调整幅度 2007年 05月 15日 10. 50% 11% 0. 5 2007年 04月 16日 10% 10. 50% 0. 5 2007年 02月 25日 9. 50% 10% 0. 5 2007年 01月 15日 9% 9. 50% 0. 5 2006年 11月 15日 8. 50% 9% 0. 5 2006年 08月 15日 8% 8. 50% 0. 5 2006年 07月 5日 7. 50% 8% 0. 5 2004年 04月 25日 7% 7. 50% 0. 5 2003年 09月 21日 6% 7% 1 1999年 11月 21日 8% 6% -2 1998年 03月 21日 13% 8% -5 1988年 09月 12% 13% 1 120