The Institute of Chartered Accountants of India Jaipur

“SMEs & Its role in")

")

of GDP 1. Agriculture Sector")

eligible. Under")

- Object : -MSME business is challenging in")

: Motivating and encouraging MSEs for use of bar")

Rajasthan Tenancy Act,")

is an online portal for Government officials")

- Slides: 43

The Institute of Chartered Accountants of India (Jaipur Branch) “SMEs & Its role in Indian Economy, Effect of COVID-19 & Relief Provided by the Governement” Virtual CPE Meeting on : Sat, 11 th July, 2020 11. 00 A. M Speaker : CA Ravi Jain Mob No. +91 77 -376 -21514 Email ID- ravijain 125@gmail. com

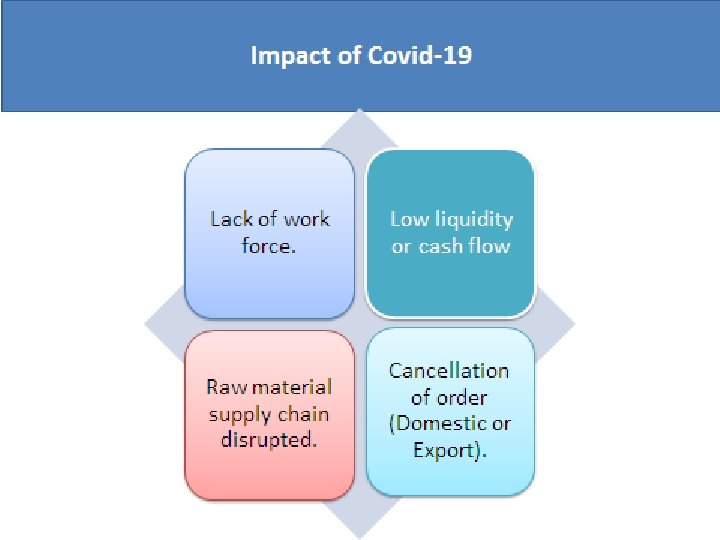

INDEX • Background of MSMEs • Why It was needed to form a separate ministry and Separate Act for Small enterprises. • Challenges to MSMEs • Enterprises covered under MSMEs act • New Definition of MSMEs. • Major Schemes by Ministry of Central Government/RBI. • Impact of Covid-19 • Covid-19 measures announced by the Government

Background of MSMEs • Government made an act of The Industries (Development & Regulation) Act, 1951’ • Manufacturing license will be given only after “full and complete investigation”. • Due to many Government controls & regulations it has become difficult to set up an industry by all. • Only large scale units were able to set up as small scale units were way behind. • First time in 1984, Government recognized the importance of small scale units and introduced Section 11 B in “The Industries (Development and Regulation) Act, 1951” which gave Supportive measures, Exemptions and favorable treatment to small units.

• However there was neither separate Act nor separate ministry for the small units till 1999. • In Oct 1999, Separate Ministry of Small Scale Industry & Agro and Rural Industries were established. • In 2006, a separate act was enacted on June 2006 called Micro, Small and Medium enterprises development act, 2006 for providing various support measures for small units. • In 2007, Govt change the name of the Ministry from Small Scale Industry & Agro and Rural Industries to Ministry of Micro, Small and Medium Enterprises.

Why It was needed to formed a separate Ministry & Act for Small enterprises? Contribution to Indian Economy: Market: India’s Micro, Small, and Medium Enterprises (MSMEs) base is the largest in the world after China. Number of MSMEs: In India, at present, there are nearly 63 million such enterprises in various industries. of these, -99. 5 per cent of MSMEs are micro. -nearly 14% are women-led enterprises. GDP Contribution: MSME sector accounts for 29. 70% of India’s GDP which includes contribution of Mfg sector of approx 6. 11 % and Service sector of 23. 59%. Target to increase 50% from 29. 70% to achieve 5 trillion economy. Employment opportunity: The significance of the MSMEs sector can be noted from the fact that it is the second-largest employment provider, after agriculture in India employing close to 124 million people. Target to increased 180 million in next 5 years

Products: The sector provides a wide range of services and is engaged in the manufacturing of over 6, 000 products – ranging from traditional to hi-tech items. MSME Export: 48% of India Total exports. Target to export 60 % from MSMEs Output: 45 % of the total Indian manufacturing output. Bank Lending: Accounts for Rs. 17. 75 trillion lending to MSMEs sector.

Growth Engine of the Economy S. No. Sector Share (%)of GDP 1. Agriculture Sector 15. 87 % 1. 1 Agriculture forestry and fishing 15. 87 % 2. Industry Sector 29. 73 % 2. 1 Mining & Quarrying 2. 70 % 2. 2 Manufacturing 16. 83 % 2. 3 Electric, Gas water supply and other utility service. 2. 67 % 2. 4 Construction. 7. 54 % 3. Service sector. 54. 40 % 3. 1 3. 2 Trade, hotels, transport, Communication and Service related 18. 62 % to broadcasting. Financials, real estate and Prof service. 20. 96 % 3. 3 Public administration, defence and other service. 14. 82 % Total 100. 00%

Challenge to MSMEs High cost of Raw Material Low Access to National and Global Market Absence of adequate and Timely banking finance Limited capital and Knowledge Low level of Innovation and Little R&D MSMEs Lack of Skilled Manpower

Enterprises covered under MSMEs act? • The Government of India has enacted the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 in terms of which the definition of micro, small and medium enterprises is as under: • MSME Covers both Manufacture as well as Service provider entity. • Manufacturing Entities: - Enterprises engaged in the manufacture or production, processing or preservation of goods. • Service Entity: - Enterprises engaged in providing or rendering of services.

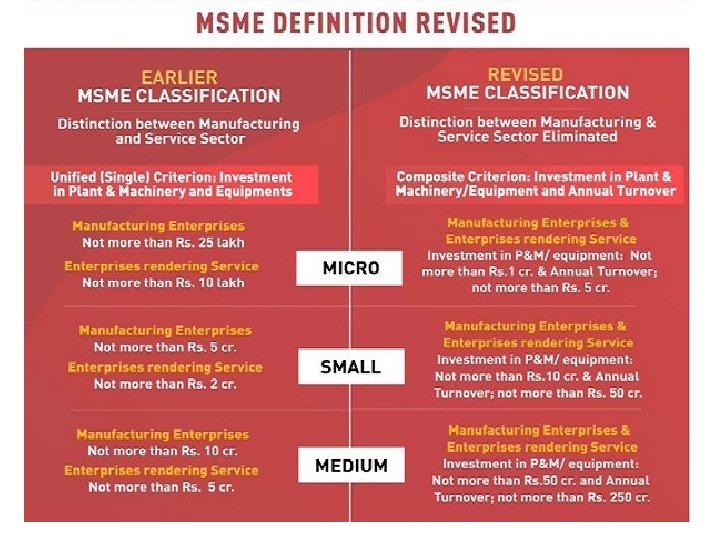

Definition of MSMEs. -Sec-7 of MSMED Act, 2006 • Based on the investment in Plant & Machinery and Equipment. Earlier MSME Classification Micro Small Medium Manufacturing Enterprises Investment< Rs. 25 lakh Investment< Rs. 5 Investment< Cr. Rs. 10 Cr. Service Enterprise Investment< Rs. 10 lakh Investment< Rs. 2 Investment< Rs. 5 Cr Cr

New MSMEs definition: - • Included Turnover. • Distinction between manufacturing & service enterprises eliminated • Limit criteria are increased. Classification Micro Small Medium Manufacturing Investment < Rs. 1 Cr. Investment < Rs. 10 Cr. Investment < Rs. 50 Cr. & Service And And enterprises Turnover < Rs. 5 Cr. Turnover < Rs. 50 Cr Turnover < Rs. 250 Cr • Announced on 13 th May, 2020 • Applicable from 1 st July, 2020 • Notification: S. O. 2119(E)dated 26 th June, 2020 • Export turnover shall not considered.

Loan without Collateral-CGTMSE Loan upto Rs. 2 Crore. Project Should be viable. Promoter margin should be at least 10 %. Guarantee given by the CGTMSE upto 75%. Eligible Micro and Small Enterprises. Approx 7000 Cr is disbursed to 18 lakh entrepreneurs beneficiaries *If any assistance required may write a mail to info@indiansmechamber. com

Category Maximum extent Guarantee given by CGTMSE where credit facility is Upto 5 lac Micro Enterprises 85% of the amount in default subject to a maximum of 4. 25 lac Above 5 lac upto 50 lac Above 50 lac upto 200 lac 75 % of the amount in default subject to a maximum of 37. 50 lac Women enterprises/Unit located in north east region (other than credit facility upto 5 lacs to micro enterprises) 80% of the amount in default subject to a maximum of 40 lac All other category of borrowers 75 % of the amount in default subject to a maximum of 37. 50 lac 75 % of the amount in default subject to a maximum of 150 lac

Public Procurement Policy-Sec 11 of MSMDE Act, 2006 Object: -The objective of Policy is promotion and development of Micro and Small Enterprises by supporting them in marketing of products produced and services rendered by them. Scheme was introduce on 2012 and amended on 2015 and 2018. Scheme for Micro and Small Enterprises (MSEs). Every Central Ministry /Department / PSUs( 374) shall set an annual target for 25% procurement from MSE Sector. sub-target of 4% out of 25% target of annual procurement earmarked for procurement from MSEs owned by SC/ST entrepreneurs. Sub-Target of 3% out of 25 % target of annual procurement from MSEs owned by women entrepreneurs 358 items are reserved for procurement from MSEs For effective monitoring of procurement from MSEs, Govt launched public procurement portal”MSME SAMBANDH” on Dec, 2017

. Procurement by Govt. CPSE of Rs. 125, 634 Crore in FY 2019 -20. Procurement from MSEs of Rs. 37, 669 Cr in FY 19 -20 from 152926 lac unit. 29. 98% • Https: //eprocure. gov. in

Raw Material Assistance Scheme: Object: -Raw Material Assistance Scheme aims at helping MSMEs by way of financing the purchase of Raw Material. This gives an opportunity to MSMEs to focus better on manufacturing quality products. Quality raw materials. Timely Delivery. Financial Assistance for procurement of Raw Material upto 90 days. Raw Material on Manufacturing Price. Selective raw material-Aluminum, Zinc, Copper, Iron and Steel, Coal and polymer. Limit-Single Unit-Rs. 5 Cr. Multiple unit of the borrower-15 Cr Infrastructure Unit(Single/Multiple)-Rs. 5 Cr. *Eligible Micro, Small and Medium Enterprises(MSMEs) *Apply through nsic. co. in

Protection against delayed payments- Sec 15 -24: Micro and Small Enterprises (MSEs) eligible. Under the MSME registration benefits, a buyer is expected to make a payment for the goods/services within 15 days of the purchase. If the buyer delays, the payment for more than 45 days, the enterprise is eligible to charge compound interest which is 3 times the rate notified by RBI. 47, 421 Application has been filled by MSEs and Rs. 13, 953 Cr amount involved in application • *Source: - https: //samadhaan. msme. gov. in

TRe. DS-Trade Receivable e-Discounting system Scheme was introduced on 2014 then amended two time in 2017 and 2018. Object: -Electronic plat form for facilitating the financing/ discounting of trade receivable of MSMEs from corporate and other buyers, including Government Departments and Public Sector Undertakings (PSUs), through multiple financiers. Eligible All Micro, Small and Medium Enterprises. All companies having turnover more than Rs. 500 Cr. All Govt. Department and PSU. Instance money available T+1 /3. No collateral required. No fault of defaulter. Minimal cost or charge *Benefit: -2018 -19 -7000 Cr *2019 -20; -25000 to 30000 Cr *Source: -https: //www. treds. in

Restructuring of loan Introduced on Jan 2019 Applicable to unit with aggregate exposure, including non-fund based facilities, of banks and NBFCs to the borrower does not exceed Rs. 25 Cr as on January 1, 2019. The borrower’s account is in default but is a ‘standard asset’ as on January 1, 2019 and continues to be classified as a ‘standard asset’ till the date of implementation of the restructuring. The borrowing entity should be GST-registered on the date of implementation of the restructuring. However, this condition will not apply to MSMEs that are exempt from GST-registered.

. Restructuring will not change the assets classification of the loan. One time restructuring is allowed. Restructuring of Standard assets under the scheme to be implemented by December 31, 2020 without downgrading of assets classification. 6 lac account been restructured of Rs. 22, 560 Cr

ü Scheme applicable on Oct 2019. ü Loan to MSME sector linked to RBI Repo rate.

ISO Certification charges reimbursement(ISO 9000/ISO 14001) - Object : -MSME business is challenging in the face of intense competition prevalent in the market. To survive this competition MSMEs need to ensure that their products meet international quality standards so that they can be easily marketed. The ISO 9000/ISO 14001 Certification Reimbursement Scheme helps MSEs acquire the specified ISO certification by providing them with financial aid. The charges incurred in availing ISO-9000/ISO-14001 certification are reimbursed under the scheme. The limit of reimbursement is up to 75% of the cost incurred in availing the certification subject to a maximum of Rs 75, 000 The reimbursement is done only one time. *Eligible-Micro and Small Industries. *Source: -Apply through dcmsme. gov. in

Marketing Support/Assistance to MSMEs (Bar Code): Motivating and encouraging MSEs for use of bar codes. Under this scheme, the Ministry of MSME will reimburse 75% of the one-time registration fees for bar coding and 75% of the annual renewal fees incurred for the first three years. Eligible-Micro and Small Industries. *www. dcmsme. gov. in

Facilitation of establishment and operation Scheme was proposed by the State Govt. of Rajasthan in 2019. Objective was to promote livelihood, inclusive economic growth and entrepreneurship in the state approvals under any rajasthan law and inspection for establishment and operation of enterprise. New MSMEs whose date of commencement of commercial operation is proposed on or after the date of 4 th March, 2019 No prior approval required under any state law for establishment and operation of MSMEs. Exemption from inspection under all state law for three years. No document number is required. No fees for applying under this scheme. • https: //rajudyogmitra. rajasthan. gov. in

EXEMPTIONS FROM THE APPROVALS AND INSPECTIONS MENTIONED IN THE ACT? (a) Rajasthan Tenancy Act, 1955 (Act No. 3 of 1955); (b) Rajasthan Land Revenue Act, 1956 (Act No. 15 of 1956); (c) Rajasthan Urban Improvement Act, 1959(Act No. 35 of 1959); (d) Rajasthan Gram Dan Act, 1971(Act No. 12 of 1971); (e) Jaipur Development Authority Act, 1982 (Act No. 25 of 1982); (f) Rajasthan Panchayati Raj Act, 1994 (Act No. 13 of 1994); (g) Rajasthan Municipalities Act, 2009 (Act No. 18 of 2009); (h) Jodhpur Development Authority Act, 2009 (Act No. 2 of 2009); (i) Ajmer Development Authority Act, 2013 (Act No. 39 of 2013);

Concession in Stamp Duty: q For falling under MSME stamp duty is charge of Rs. 500. q Other than MSMEs duty is 0. 25% on the loan agreement. Subsidy on Patent Registration: q Business enterprises registered under the MSME Act are given a hefty subsidy of 50 per cent for patent registration. This can be availed by sending an application to the respective ministry. Concession on Electricity: q One of the simplest MSME registration benefits, businesses registered under the MSME Act can avail a concession on electricity bills. All they have to do is submit the bills along with an application and a copy of the registered certificate by MSME.

Other Scheme: GEMS-The Government e-marketplace (Ge. M) is an online portal for Government officials and agencies to buy and procure products and services from an end-to-end online marketplace Champion-Creation and Harmonious Application of Modern Processes for Increasing the Output and National Strength. National SC/ST Hub PMEGP Mudra Loan Training Programme.