The Accounting Cycle Capturing Economic Events Lecture 2

Increase Credit (Cr. ) Decrease Contra Assets Decrease")

- Slides: 25

The Accounting Cycle: Capturing Economic Events Lecture 2

The Concept of Business Entity � Entity Principle �A business entity is an economic unit that engages in identifiable business activities � Separate owner from the personal affairs of its

Assets � Current ◦ ◦ ◦ Assets Cash and cash equivalents Accounts receivables, trade receivables Prepaids and advances Inventory Financial assets such as trading securities, investment securities � Non-Current/Fixed Assets ◦ Property, Plant and Equipment ◦ Investment property ◦ Intangible assets (patents, trademarks, licenses, copyright, goodwill) ◦ Loans receivables

Asset Valuation � The Cost Principle ◦ The Going Concern Assumption ◦ The Objectivity Principle ◦ The Stable-Dollar Assumption

Liabilities � Short Term/Current Liabilities � Long Term/Non-Current Liabilities ◦ Accounts payable – Generally payable to suppliers/vendors ◦ Notes Payable – Interest bearing loan, less than a year maturity ◦ Provisions or accrued liabilities ◦ Unearned revenue ◦ Interest payable ◦ Notes Payable – Short term, interest bearing loan ◦ Debt payable/Long term loan ◦ Bonds/Debentures ◦ Notes Payable – Interest bearing loan, more than a year maturity

Owner’s Equity � Increases through ◦ Investments of cash or other assets by the owner ◦ Earnings from profitable operation of the business � Decreases through ◦ Withdrawals of cash or other assets by the owner ◦ Losses from unprofitable operation of the business

Owner’s Equity � Sole Proprietorship � Partnership � Corporation

Statement of Financial Position – Balance Sheet

Practice Questions � Exercise 2. 3 � Exercise 2. 8

The Accounting Equation � Assets � The = Liabilities + Owner’s Equity effects of Business Transactions ◦ Exercise 2. 6

Net Income � Revenues ◦ Revenue, sales ◦ Gains ◦ Investment income (e. g. , interest and dividends) � Expenses ◦ ◦ ◦ ◦ Cost of Goods Sold Selling, general, and administrative expenses (‘SG&A’) Rent, utilities, salaries and advertising expenses Depreciation and amortization Interest expense Tax expense Losses

Net Income � Net income is an increase in owners’ equity resulting from the profitable operation of the business � Net Income always results in the increase of Owner’s Equity

Income Statement

How is Income Statement related to Balance Sheet � Net Income is reported to the Owner’s Equity Section of the Balance Sheet

The Accounting Cycle � The sequence of accounting procedures used to record, classify, and summarize accounting information in financial reports at regular intervals is often termed the accounting cycle

The Accounting Cycle � Analyzing and recording transactions via journal entries � Posting journal entries to ledger accounts � Preparing unadjusted trial balance � Preparing adjusting entries at the end of the period � Preparing adjusted trial balance � Preparing financial statements � Closing temporary accounts via closing entries � Preparing post-closing trial balance

The Use of Accounts � An account is a means of accumulating in one place all the information about changes in specific financial statement items, such as a particular asset or liability e. g. Cash, Notes Payable

Debit and Credit Entries � Debits refer to the left side of an account, and credits refer to the right side of an account

Debit/Credit Relationships Account Debit (Dr. ) Increase Credit (Cr. ) Decrease Contra Assets Decrease Increase Liabilities Decrease Increase Equity Decrease Increase Revenue Decrease Increase Expenses Increase Decrease Distributions Increase Decrease Assets

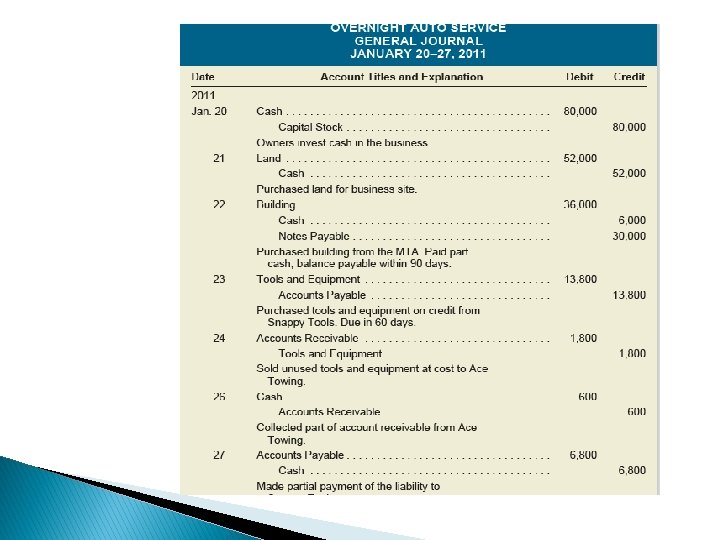

The Journal � The information about each business transaction is initially recorded in an accounting record called the journal information is later transferred to the appropriate accounts in the general ledger � This � The journal is a chronological (day-by-day) record of business transactions � Example

General Journal Basic characteristics of the general journal entry: 1. The name of the account debited is written first, and the dollar amount to be debited appears in the left-hand money column. 2. The name of the account credited appears below the account debited and is indented to the right. The dollar amount appears in the right-hand money column. 3. A brief description of the transaction appears immediately below the journal entry.

The Ledger � The entire group of accounts is kept together in an accounting record called a ledger � The transactions from the journal are posted in separate accounts and are accumulated to form a ledger � Example

Determining the Balance of a TAccount � If the debit total exceeds the credit total, the account has a debit balance; if the credit total exceeds the debit total, the account has a credit balance � Debit Balances in Asset Accounts � Credit Balances in Liability and Owners’ Equity Accounts

DOUBLE-ENTRY ACCOUNTING—THE EQUALITY OF DEBITS AND CREDITS � Every transaction is recorded by equal dollar amounts of debits and credits