Taxing Services James Alm Grant Driessen and Trey

- Slides: 12

Taxing Services James Alm, Grant Driessen, and Trey Dronyk-Trosper

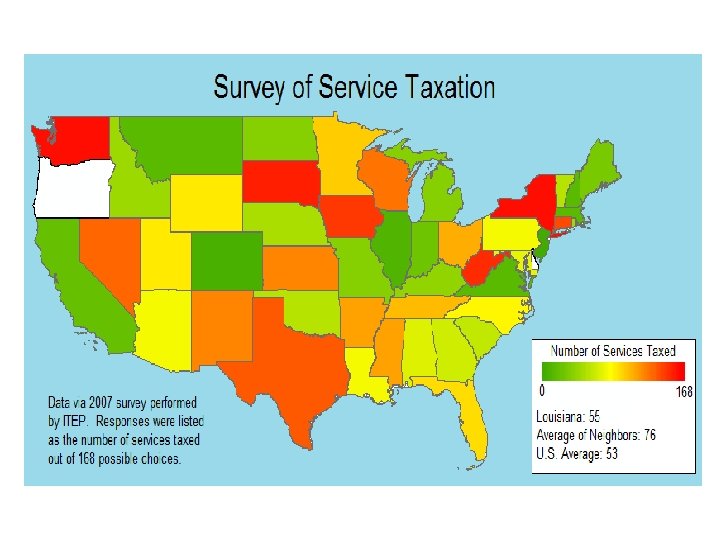

Louisiana’s Taxation of Services Louisiana Revised Statute 47: 3014 the furnishing of sleeping rooms by hotels the furnishing of printing and over printing the furnishing of cold storage space and the preparation of property for such storage the furnishing of telecommunications services the furnishing of storage or parking privileges by auto hotels and parking lots the sale of admissions to places of amusement and to athletic and recreational events, and the furnishing of privileges of access to amusement, entertainment, athletic, or recreational facilities the furnishing of laundry, cleaning, pressing, and dyeing services the furnishing of repairs to tangible personal property

Categories of Services Taxed in Texas Taxable Services in Texas Non-residential Real Property Repair, Amusement Services Restoration, or Remodeling Services Personal Property Maintenance, Cable and Satellite Television Services Remodeling, or Repair Services Credit Reporting Services Personal Services Data Processing Services Reporting and Collecting Services Debt Collections Services Security Services Information Services Telecommunications Services Insurance Services Telephone Answering Services Utility Transmission and Distribution Internet Access Services Taxable Labor--Photographers, Draftsmen, Motor Vehicle Parking and Storage Services Artists, Tailors, etc. See Book on Taxable Services in Texas Comptroller of Public Accounts

Scenario #1 – Taxing Services with estimates from 2013 Estimate: Tax Base 2013 Tax Estimate (at 4%) Adjustment for CY 2015 $1, 080, 872, 150 $43, 234, 886 $47, 329, 167 Veterinary services $207, 122, 851 $8, 284, 914 $9, 069, 484 Cable and other subscription services $221, 854, 739 $8, 874, 190 $9, 714, 563 Performing arts Promotional services for performing arts and sports and public figures Independent artists, writers, and performers Museum, heritage, zoo, and recreational services $44, 550, 187 $1, 782, 007 $1, 950, 761 $229, 732, 279 $9, 189, 291 $10, 059, 504 $57, 663, 899 $2, 306, 556 $2, 524, 983 $169, 553, 541 $6, 782, 141 $7, 424, 400 Personal care services $631, 267, 683 $25, 250, 707 $27, 641, 913 Other personal services $663, 683, 918 $26, 547, 356 $29, 061, 353 $3, 306, 301, 247 $132, 252, 050 $144, 776, 127 Included Items Scenic and sightseeing transportation services and support activities for transportation Total

Scenario #2 – Taxing Services: Expanded Base Tax Base Estimate 2013 Tax Estimate (at 4%) Adjustment for CY 2015 $3, 306, 301, 247 $132, 252, 050 $144, 776, 127 $367, 811, 060 $14, 712, 442 $16, 105, 689 $707, 881, 040 $28, 315, 242 $30, 996, 654 $1, 577, 445, 934 $63, 097, 837 $69, 073, 111 $3, 455, 246, 566 $138, 209, 863 $151, 298, 136 $70, 201, 160 $2, 808, 046 $3, 073, 964 $827, 151, 371 $33, 086, 055 $36, 219, 257 $555, 398, 097 $22, 215, 924 $24, 319, 740 Other information services $81, 956, 833 $3, 278, 273 $3, 588, 721 Insurance-related support services $338, 513, 160 $13, 540, 527 $14, 822, 795 $11, 287, 906, 468 $451, 516, 259 $494, 274, 194 Included Items From Scenario #1 Other Personal Services: Transit and ground passenger transportation services Couriers and messenger services Accounting, tax preparation, bookkeeping, and payroll services Architectural, engineering, and related services Photographic services All other miscellaneous professional, scientific, and technical services Data processing-hosting-ISP-web search portals Total

Scenario #3 – Taxing Services Not Taxed in LA But Taxed in TX and TN Included Items Comparable Item in Jindal 2013 Plan Jindal Tax Base 2013 Tax Estimate (at 4%) Adjustment for CY 2015 $1, 294, 951, 601 $51, 798, 064 $56, 703, 266 $151, 093, 676 $6, 043, 747 $6, 616, 081 $3, 455, 246, 566 $138, 209, 863 $151, 298, 136 $169, 553, 541 $5, 070, 845, 384 $6, 782, 142 $202, 833, 815 $7, 424, 400 $222, 041, 884 Pet grooming Landscaping/lawn care Swimming pool cleaning Cable TV Personal care services and other personal services Health clubs Auto road services Parimutuel racing Exterminating Labor charges and remodeling Marina services Total Facilities support services Architectural, engineering, and related services Museum, heritage, zoo, and recreational services

See Tax Foundation, Chapter 3

Overall, then… • Taxing services in the sales tax will likely increase the progressivity of the tax system. • There is significant revenue potential from taxing services. • But: taxing services will likely add to administrative complexity.