Econ 134 A Final Exam Solutions John Hartman

- Slides: 13

Econ 134 A Final Exam Solutions John Hartman Form A Summer 2019 Session B

#1 • A stock is expected to pay a $10 dividend every 12 months, starting in 12 months. The risk-free in the market is 10%, and the market rate of return is 13%. Suppose that Boris own a European call option with an expiration date of today, and an exercise price of $82. For this stock, determine which beta (β) values will benefit Boris from exercising the option. • Boris should exercise the option if the price of the stock is greater than $82. The present value of the stock is 10/r. Thus, we have • 10/r > 82, or 10 > 82 r • By CAPM, we have r = Rf + β(Rm-Rf) = 0. 1 + 0. 03β • Therefore, the price of the stock is greater than 82 if: • 10 > 82(0. 1 + 0. 03β) = 8. 2 + 2. 46β • 1. 8 > 2. 46β • 0. 7317 > β

#2 • Christiana is planning her retirement. She must make a single deposit 20 years from today into an account and will be able to withdraw $200, 000 per year in the future. The first of these withdrawals will occur 30 years from today and the final one will occur 45 years from today. How much must the deposit be in order to have a balance of $0 after the final withdrawal occurs? Assume an effective annual interest rate of 14%. • PV(deposit) = PV(withdrawals) • 16 withdrawals, with the first one being in 30 years • X/(1. 14)^20 = (200, 000/0. 14)*(1 – 1/(1. 14^16))*(1/1. 14)^29 • X/(1. 14)^20 = 28, 035. 90 • X = 385, 311

#3 • The cost of capital for an all-equity firm is 15%, while the cost of debt for the same firm is 11%. Assume this company currently has 70% of its value in bonds and 30% in stocks. Assuming the relevant assumptions from the Modigliani and Miller propositions, what is the current cost of equity? • RWACC = (S/S+B)RS + (B/S+B)RB • 0. 15 = 0. 3 RS + 0. 7(0. 11) • 0. 15 – 0. 077 = 0. 3 RS • 0. 73/0. 3 = RS = 0. 2433

#4 • Eric has just won a contest that offers two prizes, but he can only claim one. He can receive a single payment of $20, 000 in one year, OR he can receive $3, 000 every year (forever) starting in one year. If he accepts the single payment, what can you say about his effective annual discount rate? • Eric accepts the single payment, which implies the following: • 20, 000/(1+r) > 3, 000/r • 20, 000 r > 3, 000(1+r) = 3, 000 + 3, 000 r • 17, 000 > 3, 000 • r > 3, 000/17, 000 • r > 0. 1765

#5 • Horse Frame Pictures, Inc. is expected to pay a dividend of $2 later today. The annual growth rate for the dividend over the next 5 years will be 40%. This will be followed by a constant growth rate of 12% forever after. If the effective annual discount rate for the company is 23%, what is the present value of the stock? • Growing annuity (r = 0. 4) + growing perpetuity (r = 0. 12) • Growing annuity starts today, includes five payments • PV = (2/(0. 23 -0. 4))*[1 – ((1. 4)/(1. 23))^5]*(1. 23) = 13. 17 • Growing perpetuity starts in five years, right after the last year of 40% growth • First payment = 2*(1. 4)^5 = 10. 76 • PV = (10. 76 /(0. 23 -0. 12))*(1. 23)^4 = 42. 72 • PV = 13. 17 + 42. 72 = 55. 896

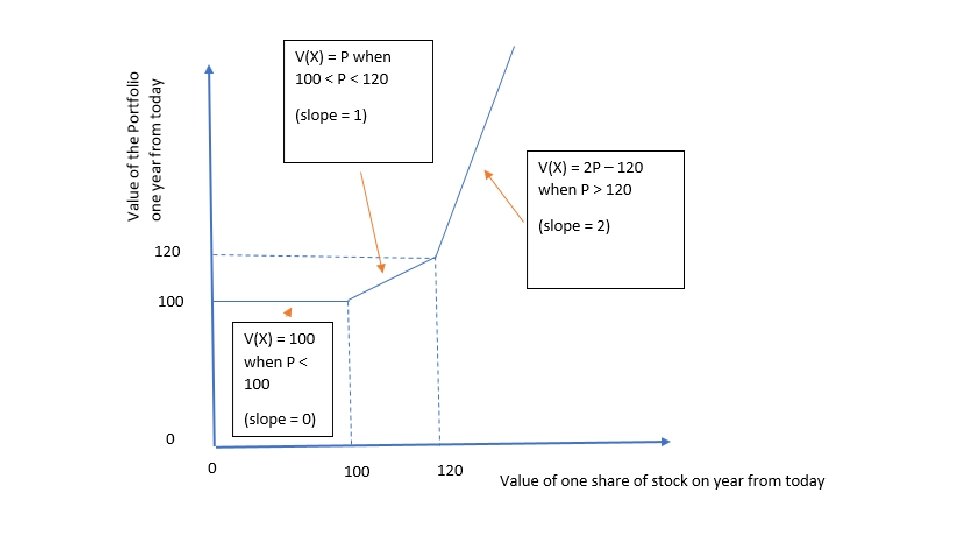

#6 • Tatia buys one put option with an exercise price of $100 (per share), one call option with an exercise price of $120 (per share), and one share of stock currently valued at $200. All three assets are purchased today. The expiration date of all of the options purchased is one year from now. Each option is for buying or selling one share of stock. For simplicity in this problem, you can assume that the discount rate is 0%. Draw a well-labeled graph that shows the value of a combination of the two options and one share of stock, as a function of the value of the stock at expiration. The vertical intercept should have the value of the combination of the assets. The horizontal intercept should have the value of the stock on the expiration date. Make sure to label your intercepts and other relevant numbers on each axis, where relevant. (Hint: You may want to look at the front page of the test to see a well-labeled graph. ) Explain your answer in words, math, and/or using additional graphs. Include enough detail so that everything on the graph is unambiguous.

#6 cont. • Put option is exercised when the price of the stock is below 100 • Call option is exercised when the price of the stock is above 120 • P < 100 • Value(P) = share price + surplus from exercising put option • Value(P) = P + (100 -P) = 100 • 100 < P < 120 • Value(P) = share price • Value(P) = P • 120 < P • Value(P) = share price + surplus from exercising call option • Value(P) = P + (P = 120) = 2 P - 120

#7 • Everywhat Delivery Services, Inc. is currently a cash cow. Without any re-investment of their earnings, they will earn $17. 50 per share every year forever. The effective annual discount rate for owning this stock is 35%. Assume that the next dividend payment will be made in 9 months. Subsequent dividend payments will be made every 12 months after the payment in 9 months. Suppose that Everywhat Delivery Services could retain all of its earnings 6. 75 years from today, and earn 30% on these earnings the following year. (In other words, no dividend would be paid 6. 75 years from today if the company retains all of its earnings, and would continue to act as a cash cow in later years. )

#7 a • What is the present value of each share of stock if it continues to act as a cash cow? • No reinvestment, so the present value of the stock is just a standard perpetuity starting in nine months • PV = (17. 50/0. 35)*(1. 35^0. 25) • (1. 35^0. 25) because the payments need to be shifted sooner by 3 months, or one fourth of a year • PV = 53. 90

#7 b • Should the company retain its earnings 6. 75 years from today? Why/why not? • No the company should not retain earnings. The rate of return is less than the annual discount rate. Similarly, the NPV of retaining the dividend is less than 0

#7 c • How much does the stock’s present value change if the company retains its earnings 6. 75 years from today? • Change in present value has two components: • a dividend 6. 75 years from today is given up • in exchange, shareholders receive an extra payment 7. 75 years from today • amount of the payment is the normal dividend plus 30% return • ΔPV = -17. 50/(1. 35^6. 75) + (17. 50*1. 3)/(1. 35^7. 75) • ΔPV = -2. 308 + 2. 223 • ΔPV = -0. 085