COM2 PRODUCT DEVELOPMENT CAS Ratemaking Seminar New Orleans

: • Lack of familiarity with product")

• Are they able to grow and")

• Track semi-reliable early indicators – PD frequency/industry severity")

- Slides: 22

COM-2 PRODUCT DEVELOPMENT CAS Ratemaking Seminar, New Orleans March 11, 2005 Dave Mc. Laughry, FCAS, MAAA Senior Actuary and Product Manager Farmers Insurance Group

Entering New Personal Lines Markets • Expanding into a new state • Launching a new product line • Entering a new distribution channel

Outline • The challenges • Laying the groundwork • • Claims/Underwriting/Marketing Pricing/Reserving Implementation Tracking Early Experience

Entering New Markets - The Challenges: • Lack of applicable premium/loss experience • Untested data collection processes • Weak understanding of competition • Nonexistent/immature claims organization • Underwriters inexperienced in the new market

Entering New Markets - The Challenges (cont. ): • Lack of familiarity with product nuances • Local peculiarities: legal venue, weather, construction practices, etc. • New regulatory environment! • Knowledge gained from other markets is easy to misapply

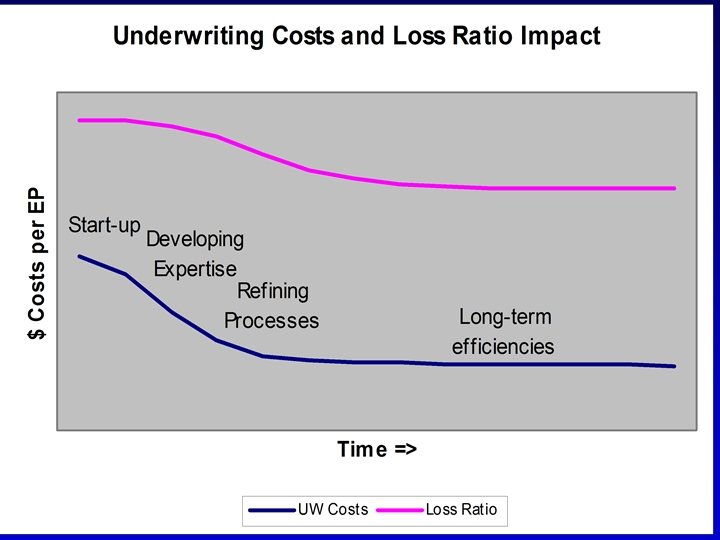

Laying the Groundwork • Build a model including all costs, allow for contingencies • Develop clear expectations and reasonable timeframes • Test using pilot program before making large investment • Build processes for accurate data collection • Measure everything

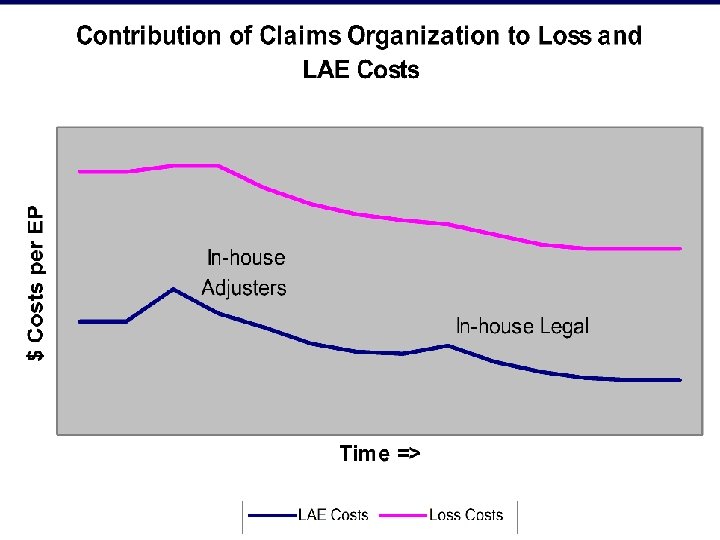

You mean we have to pay Claims? • Major cause of poor early performance indemnity and expense • Build staff in-house or outsource? • Experienced staff and market-specific knowledge is key • Establish clear standards of performance early on • Document retrieval process

Underwriting - Friend or Foe? • Staff adequately; allow for low efficiency early on • Keep a firewall between underwriting and marketing • Be generous with investigative reports you need all the help you can get • Fully research market specific requirements

Marketing with Restraint • Know what your target market is • Don’t sell on price • Overly aggressive sales goals are a recipe for failure • Cap production to stay in line with u/w, claims capacity • Beware of the underwriting cycle!

Pricing in a Partial Vacuum • Experience from similar markets may be considered, if applicable • If you have no historical experience Why not use competitor data to set rates?

The Perils of Competitor Rates What could go wrong? • • Credit models Underwriting Black box tiering Driver assignment • • Customer base Contract differences Product bundles Data validation

The Perils of Competitor Rates (cont. ) • Are they able to grow and make money? • How closely can you mirror a responsible competitor? • Be at least as sophisticated as they are its their neighborhood! • High conversion rates are a leading indicator of trouble ahead

Reserving in a Total Vacuum • Use pegged loss ratios to start with • Key considerations as experience unfolds – Earned premium growth pattern – Stated claims procedures – Maturation of claims organization – Market peculiarities (reporting patterns, severity, tort thresholds, UM statutes) – Applicability of related markets – Reserve-to-paid ratios • Take the heat for high IBNR loads

Implementation - taking the plunge. . . • Have an exit plan - avoid the Roach Motel syndrome • Have a plan to revise rates before experience is available • If possible, pilot on a small scale first – Utilize manual processes – File and use state – Limited distribution

Tracking Early Experience • Ignore calendar period results • Understand growth patterns – Earned premium – Reported claims – Paid Severity – Case reserves – Front-loaded expenses (commissions) – Costs that lag (residual market, LAE, some taxes) – Accounting practices for O. A. and G. E. vary

Tracking Early Experience (cont. ) • Track semi-reliable early indicators – PD frequency/industry severity – # claims/$1, 000 premium – Short-tailed coverages (PD, coll, PIP) • Impact of “new business penalty” • Skewed distribution of early customer base

Entering New Markets Measuring Success • Identify which metrics are reliable • Measure vs. model, not traditional financial indicators • Exceeding early growth goals is usually a bad sign

Questions? ?