VAT PAYE RETURNS All VAT and PAYE returns

number, please provide your Passport or")

• Removal of the withholding tax on the interest")

- Slides: 20

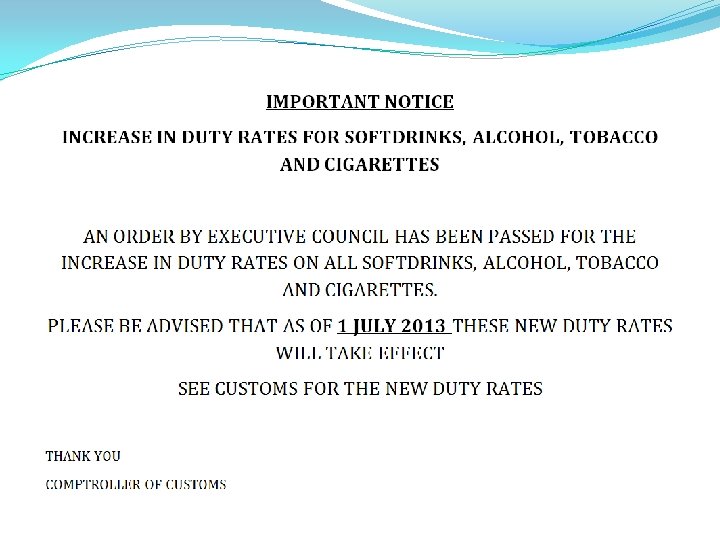

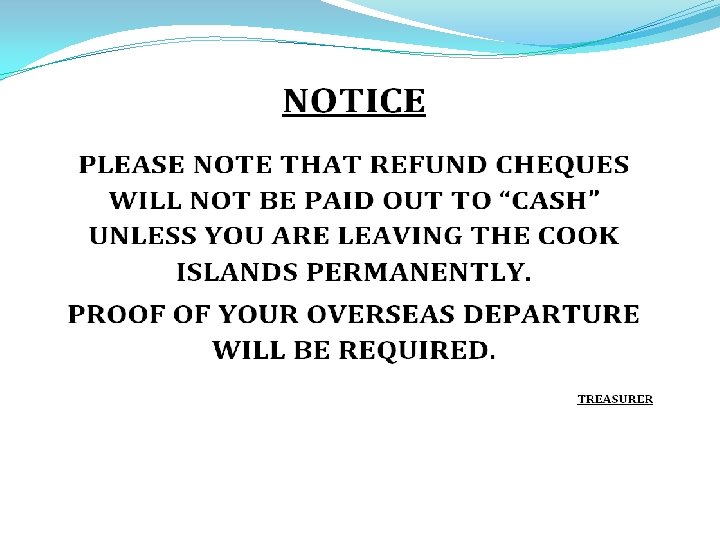

VAT & PAYE RETURNS All VAT and PAYE returns must be furnished on or before the 20 th of the month following the period the return covers. If you fail to make payment for VAT or PAYE on time, an additional tax will be charged as follows: Ø 5% on the amount not paid by the due date Ø 1% on the total outstanding one month after the due date Ø 1% of the total outstanding at the end of each month thereafter If the 20 th of the month falls on a weekend or public holiday, your return and payment are due on the next business day. If a business has not operated, not earned income and/or did not deduct PAYE in a particular month a NIL Return must be furnished.

RMD APPLICATION When applying for a RMD (tax) number, please provide your Passport or Birth Certificate as proof of identification. Me ka retita koe iakoe no tetai numero tero noou, ka anoanoia kia omai koe i tetai tutu nenei o toou Passport e pera katoa toou peapa ra anau anga ei akapapu i taau retita anga iakoe.

We will act without fear or favour to collect revenue which pays for our Cook Islands way of life

For your convenience and to avoid the queues a drop-box has been placed at the new Immigration Office in the NZ High Commission Building. This box may be used to furnish your tax returns and cheque payments (please do not put cash in the box). Once your payments have been processed we will mail a receipt to you. Kia mama i koe i te retita anga e pera kia akapoto i te tuatau, e pia meere tetai tei akatakaia i roto ite opati-iti ote Immigration i raro mai i te opati o te Niu Tireni Kumitiona teitei. Ka rauka katoa ia koe ite tuku mai i taau peapa tutakianga tero na roto i teia pia meere. Auraka e tuku i te moni ki roto i teia pia, mari ua ko ke moni tata peapa (cheque) ua. Ka tuku i atu taau (reciept) ritiiti na roto i te meere kia koe.

Your Taxes are helping to contribute to our country’s economic growth

Summary of Tax Changes in the Cook Islands Gove Import Taxes • Maintain the planned increases to health related excises as outlined in the 2012/13 Budget; • Commit to further refinements of the alcohol and sugary drinks excise regime to allow for greater simplicity, with the changes being effective as of 1 July 2014. • Switch the current ad valorem (price-based) levy on sugary drinks to a specific (quantity-based) levy from 1 January 2014. • Increase the annual indexation of specific (quantity based) levies to 5 per cent per annum after the initial increase periods for the respective products from 1 July 2014. • Eliminate the import levies on pork, sea freighted eggs, ice cream, and seasonal vegetables from 1 January 2014.

Value Added Tax • Increase the VAT rate to 15 per cent. • Increase threshold for mandatory VAT registration from $30, 000 to $40, 000 in gross turnover a year. • Increase threshold for voluntary VAT registration from $15, 000 to $20, 000 in gross turnover a year.

Personal Income Tax • Decrease the personal income tax rates and adjust the tax income bands to the following schedule from 1 January 2014: 2013 personal income tax rates 2014 personal income tax rates Threshold / Income band Marginal tax rates Up to $10, 000 Nil Up to $11, 000 Nil $10, 000 to $30, 000 25 per cent $11, 000 to $30, 000 18. 5 per cent $30, 000 upwards 30 per cent $30, 000 to $80, 000 27. 5 per cent $80, 000 upwards 30 per cent • Remove the differential rates of non-residents to ensure an equal treatment of income with resident taxpayers from 1 January 2014, with incomes assessed by the number of days spent in country. • Remove the differential tax rate on secondary employment from 1 January 2014;

Personal Income Tax • Add a 183 day rule to the determination of tax resident status. • Increase both pensions by 25 per cent, and increase all other ongoing social welfare payments by 10 per cent. • Remove the exemption on the taxation of the pensions and allowances paid under the Welfare Act 1989 (or revised Act) from 1 January 2014

Company Income Tax • Leave the current company tax rates unchanged. • Do not implement a general capital gains tax. • Eliminate the tax exemption afforded to international airlines from 1 January 2014, with airlines being charge the same company tax rates as other companies carrying on business in the Cook Islands.

Local Trusts • Amend the current schedule of taxation on local trusts from 1 January 2014 to reflect a single flat tax on all trust income equivalent to the highest personal income tax (currently 30 per cent).

Withholding Tax (on domestic holdings) • Removal of the withholding tax on the interest earned on domestic deposits from 1 January 2014. • Include interest earnings as part of personal income from 1 January 2014 by removing the exemption on interest earnings in the Income Tax Act 1997. • Retain the treatment of interest earned on bank deposits as business income. • From 1 January 2015, bank accounts without a linked RMD number attract the highest personal tax rate until such time as an RMD number is obtained.

Other Administrative Changes • Establish a Financial Outreach Office position within RMD to provide tax and financial literacy assistance to local businesses and the general public from 1 January 2014. • E-filing of tax returns to be made available from 1 January 2015. • Strengthen the requirement of employers to charge the nondeclaration rate for employees who do not present an RMD number from 1 January 2015.