What is Accounting The provision of information of

= Capital + (Resources Supplied by the")

10")

Traditional Format “T form” • • The left-hand")

Current Liabilities (Repayable within the")

1 May 2004 n Transaction w Started an engineering business putting $1,")

3 May 2004 n Transaction w Bought machinery on credit from Unique")

2004 $ May 3")

4 May 2004 n Transaction w Withdrew $200 cash from the bank")

7 May 2004 n Transaction w Bought a motor van paying in")

10 May 2004 n Transaction w Sold some of the machinery for")

2004 $ May 10 Machinery 15 Machinery 2004 May 3 Unique")

21 May 2004 n Transaction w Returned some of the machinery, value")

275 May 10 S. Au")

28 May 2004 n Transaction w S. Au paid the firm the")

2004 May 10 Machinery (E) $ 2004 15 May 28 Bank")

30 May 2004 n Transaction w Bought another motor van paying by")

31 May 2004 Transaction n Paid the amount of $248 to Unique")

2004 May 1 Capital (A)")

Dr. Purchases account Cr. Creditor/Supplier account")

2004 Aug 1")

Dr. Purchases account Cr. Cash")

Dr. Cash account Cr. Sales account")

2004 Aug 3 Sales $ 250 Sales 2004 Aug 3 K.")

Dr. Cash account Cr. Sales account")

2004 Aug")

2004 Aug 6 Return outwards $ 96 Returns Outwards 2004 Aug")

Purchases of goods where they are paid")

Cash Purchases Dr. Purchases account Cr. Cash account")

Credit Purchases The first part is: n n Dr. Purchases account Cr. Supplier’s/Creditor’s")

2006 Jun 5")

The different between the total “Debit” side and the total")

Any balance of an account brought from the last financial")

the “Debit” balance to next period and inserting the")

the “Debit” balance to next period and inserting the")

“Balance c/f” is the same meaning of “Balance c/d” except")

The “Balance b/f” should be appeared on the top of")

$ 2005 3, 850 Dec 31 Balance")

Purchases $ 2005 2, 900 Dec 31 Trading")

$ 2005 240 Dec 31 Profit &")

- Slides: 150

What is Accounting The provision of information of an economic or financial nature. Enable to make better decision.

What is Bookkeeping Book-keeping is the process of recording the monetary worth of business transactions in the books of accounts. It is the record-making phase of accounting.

The Major Users of Accounting Information Owners Management Lenders Suppliers of Goods and Creditors Customers Competitors Government Employees The Public

Accounting Equation Assets (Resources in the business) = Capital + (Resources Supplied by the owner) Liabilities (Resources Supplied by outsiders)

The Balance Sheet The expression of the accounting equation

Example The introduction of capital 1 July 1997 Peter opened a bank account for this new business and paid in a cheque of $40, 000 as his investment in the business.

Example The purchase of stock by cheque 4 July 1997 The business bought goods for resale of $5, 000 by cheque.

Example The purchase of stock by incurring a liability (i. e. deferring payment) 10 July 1997 The business bought goods $10, 000 on credit from P. Tang.

Example Sale of stock for cash 20 July 1997 Sold goods for cash $4, 000.

Example Sale of stock on credit 22 July 1997 Sold goods on credit to ABC Ltd. $1, 000.

Example The settlement of a liability 25 July 1997 Paid money owing to P. Tang by cash $4, 000.

Double-Entry System Every transaction affects two items in the balance sheet.

The Format of an Account (i) Traditional Format “T form” • • The left-hand side is called the debit side. The right-hand side is called the credit side. (ii) Computerized Format

Assets They are economic resources which provide benefits to the business.

Assets Fixed Assets Current Assets

Fixed Assets Intangible Fixed Assets Tangible Fixed Assets

Intangible Fixed Assets E. g. Goodwill Patents Franchises Royalties Development Expenditures

Tangible Fixed Assets E. g. Land Buildings Premises Furniture & Fittings Office Equipment Machinery Motor Vehicles Long-term Investments

Current Assets E. g. Stock Debtors Current Investments Prepaid Expenses Bills Receivable Accrued Income Bank/Cash

Liabilities They are debts or obligations owed by the business to outside parties.

Liabilities Long-term Liabilities (Repayable beyond the next accounting year) Current Liabilities (Repayable within the next 12 months)

Long-term Liabilities E. g. Debentures Bank Loans from Others

Current Liabilities E. g. Creditors Accrued Expenses Prepaid Income Bank Overdrafts

Capital is what the company owed to the owners. It is a liability of the business to its owners.

Any asset account Increase Decrease + Any liability account Decrease Increase - + Capital account Decrease Increase - +

Example (A) 1 May 2004 n Transaction w Started an engineering business putting $1, 000 into a bank account. n Effect w Increases asset of bank w Increases capital of owner n Action w Dr. Bank account w Cr. Capital account

Bank 2004 May 1 Capital $ 1000 Capital 2004 May 1 Bank $ 1000

Example (B) 3 May 2004 n Transaction w Bought machinery on credit from Unique Machines $275. n Effect w Increases asset of machinery w Increases liability to Unique Machines n Action w Dr. Machinery account w Cr. Unique Machines account

Machinery 2004 $ May 3 Unique 275 Unique Machines (Creditor) 2004 $ May 3 Machinery 275

Example (C) 4 May 2004 n Transaction w Withdrew $200 cash from the bank and placed it in the cash box. n Effect w Increases asset of cash w Decreases asset of bank n Action w Dr. Cash account w Cr. Bank account

Cash 2004 May 4 Bank $ 200 Bank 2004 $ May 1 Capital 1000 2004 May 4 Cash $ 200

Example (D) 7 May 2004 n Transaction w Bought a motor van paying in cash $180 n Effect w Increases asset of motor van w Decreases asset of cash n Action w Dr. Motor Van account w Cr. Cash account

2004 May 7 Cash 2004 May 4 Bank Motor van $ 180 Cash $ 2004 May 7 200 $ Motor van 180

Example (E) 10 May 2004 n Transaction w Sold some of the machinery for $15 on credit to S. Au. n Effect w Increases asset of money owing by S. Au w Decreases asset of machinery n Action w Dr. S. Au’s account w Cr. Machinery account

S Au (Debtor) 2004 $ May 10 Machinery 15 Machinery 2004 May 3 Unique $ 275 2004 May 10 S Au $ 15

Example (F) 21 May 2004 n Transaction w Returned some of the machinery, value $27, to Unique Machines. n Effect w Decreases liability to Unique Machines w Decreases asset of machinery n Action w Dr. Unique Machines w Cr. Machinery account

Machinery 2004 $ 2004 May 3 Unique Machines (B) 275 May 10 S. Au (E) $ 15 May 21 Unique Machines (F) Unique Machines (Creditor) 2004 May 21 Machinery $ 27 2004 May 3 Machinery $ 275 27

Example (G) 28 May 2004 n Transaction w S. Au paid the firm the amount owing, $15, by cheque. n Effect w Increases asset of bank w Decreases asset of money owing by S. Au. n Action w Dr. Bank account w Cr. S. Au’s account

S. Au (Debtor) 2004 May 10 Machinery (E) $ 2004 15 May 28 Bank (G) $ 15 Bank 2004 May 1 Capital May 28 S Au $ 1000 15 2004 May 4 Cash $ 200

Example (H) 30 May 2004 n Transaction w Bought another motor van paying by cheque $420. n Effect w Increases asset of motor vans w Decreases asset of bank n Action w Dr. Motor van account w Cr. Bank account

2004 May 7 Cash May 30 Bank Motor van $ 180 420 Bank 2004 May 1 Capital May 28 S Au $ 1000 15 2004 May 4 Cash May 30 Motor van $ 200 420

Example (I) 31 May 2004 Transaction n Paid the amount of $248 to Unique Machines by cheque. Effect n n Decrease liability to Unique Machines Decrease asset of bank Action n n Dr. Unique Machines Cr. Bank account

Bank $ 2004 1, 000 May 4 Cash (C) 2004 May 1 Capital (A) May 28 S. Au (G) 15 May 30 Motor Van(H) $ 200 420 May 31 Unique Machines (I) 248 Unique Machines (Creditor) 2004 May 21 Machinery $ 27 May 31 Bank 248 2004 May 3 Machinery $ 275

The double entry system: The treatment of stock The stock of goods in a business is constantly changing because some more of it is bought, some of it is sold, some is returned to the suppliers and some is returned by the customers.

The treatment of stock In four accounts: Purchases account For the purchase of goods Sales account For the sales of goods Returns inwards account For goods returned to the firm by its customers Returns Outwards account For goods returned from the firm to its suppliers

As stock is an asset, §these four accounts are all connected with this asset, §the double entry rules for these four accounts are those used for assets.

Purchases of stock on credit (Credit Purchases) Dr. Purchases account Cr. Creditor/Supplier account

Example: 1 August 2004 Goods costing $165 were bought on credit from D. Hong. n The asset of stock is increased. n An increase in a liability

2004 Aug 1 D. Hong Purchases $ 165 D. Hong (Creditors) 2004 Aug 1 Purchases $ 165

Purchases of stock for cash (Cash Purchases) Dr. Purchases account Cr. Cash

Example 2 August 2004. Goods costing $22 were bought, cash being paid for them immediately. n n The asset of stock was increased. The asset of cash was decreased.

2004 Aug 4 Cash Purchases $ 22 Cash 2004 Aug 4 Purchases $ 22

Sales of stock on credit (Credit Sales) Dr. Cash account Cr. Sales account

Example 3 August 2004 Sold goods on credit for $250 to K. Lee. n n K. Lee is a debtor for the goods. The increase in the asset of debtors requires a debit. The asset of stock was decreased. For this a credit entry to reduce and asset is needed.

K. Lee (Debtors) 2004 Aug 3 Sales $ 250 Sales 2004 Aug 3 K. Lee $ 250

Sales of stock for cash (Cash Sales) Dr. Cash account Cr. Sales account

Example 4 August 2004 Goods were sold for $55, the cash being received at once upon sale. n n The asset of cash was increased. A debit in the Cash account is needed to show this. The asset of stock was reduced. The reduction of an asset requires a credit.

Cash 2004 Aug 4 Sales $ 55 Sales 2004 Aug 4 Cash $ 55

Return inwards represent goods sold which have now been returned by customer. n n Dr. Return Inwards account Cr. Debtors/Customers account

Example 5 August 2004 Goods which had previously been sold to F. Lo for $29 were returned by him. n n The asset of stock was increased by the goods returned. A decrease in an asset. The debt of F. Lo to the firm is now reduced.

Return Inwards 2004 Aug 5 F. Lo $ 29 F. Lo (Debtors) 2004 Aug 5 Return inwards $ 29

Returns Outwards Returns outwards represent goods which were purchased, and are now being returned to the supplier. n n Dr. Creditors/Suppliers account Cr. Return Outwards

Example 6 August 2004 Goods previously bought for $96 were returned by the firm to K. Ho. n n The liability of the firm to K. Ho was decreased The asset of stock is decreased by the goods sent out

K. Ho (Creditor) 2004 Aug 6 Return outwards $ 96 Returns Outwards 2004 Aug 6 K. Ho $ 96

Special meaning of “Purchases” and “Sales” Purchases in accounting means the purchase of those goods. With the prime intention of selling. If something else is bought, such as a motor van, such an item cannot be called a purchase The prime intention of buying the motor van is for use by the company and not for resale.

Comparison of cash and credit purchases/sales (1) Purchases of goods where they are paid for immediately by cash (Cash Purchases) (2) Purchase of goods on credit (Credit Purchases)

(1) Cash Purchases Dr. Purchases account Cr. Cash account

(2) Credit Purchases The first part is: n n Dr. Purchases account Cr. Supplier’s/Creditor’s account The second part is: n n Dr. Supplier’s/Creditor’s account Cr. Cash/Bank account

Cash Sales Complete entry: Credit Sales First part: Dr. Cash account Dr. Customer’s account Cr. Sales account Second part: Dr. Cash/Bank account Cr. Customer’s account

The double entry system: Expenses and Revenue n Sales value of goods and services that have been supplied to customers. Expense n Value of all the assets and costs that have been used up to obtain those revenue.

Income Revenue Capital Income

Revenue E. g. Sales Rent Received Interest Received

Capital Income E. g. Profit on Disposal of Fixed Assets

Expenses Trading Expenses Selling and Distribution Expenses Administrative Expenses Financial Expenses

Trading Expenses E. g. Purchases

Selling and Distribution Expenses E. g. Carriage Salaries Commission Delivery Charges Bad Debts Discounts Allowed

Administrative Expenses E. g. Rent and Rates Office Salaries Electricity and Utilities Telephone Charges Insurance Premiums

Financial Expenses Discounting Charges Interest on Loans Debenture Interest

Expense & Revenue account An expense account is opened for each type of expense. Since assets involve expenditure and are shown as debit entries, expenses are also shown as debit entries.

Example 1 June 2006 Paid for postage stamps by cash $5 Effect: n n Increase expense of postage Decease asset of cash Action: n n Dr. Postage Cr. Cash

Cash 2006 Jun 1 Postage 2006 Jun 1 Cash $ 5 Postage $ 5

Example 2 June 2006 Paid for advertising by cheque $29 Effect: n n Increase expense of advertising Decrease asset of Bank Action: n n Dr. Advertising Cr. Bank

Bank 2006 Jun 2 Advertising 2006 Jun 2 Bank $ 29

Example 5 June 2006 n Part of our premises were not needed by us. We let someone else use them and received rent of $40 by cheque. w The asset of bank is increased. w The total of the revenue of rent received is increased.

Bank 2006 Jun 5 Rent received $ 40 Rent received (revenue) 2006 Jun 5 Bank $ 40

The Nature of Profit or Loss Profit n Revenues are greater than expenses for a set of transaction. Loss n Our expenses may exceed our revenues

The effect of profit/Loss on capital After making profit: Assets = Liabilities + Capital + Profit (i. e revenue – expenses)

Example On 1 January n n Assets: Fixtures $10, 000, stock $7, 000, cash at bank $3, 000 Liabilities: Creditors $2, 000 Assets $10, 000 + $7, 000 + $3, 000 – Liabilities $2, 000 = $18, 000

On 2 January The whole of the $7, 000 stock was sold for $11, 000 cash. n n Asset: Fixtures $10, 000, stock nil, cash at bank $14, 000 Liabilities: Creditors $2, 000 Assets $10, 000 + $14, 000 – Liabilities $2, 000 = $22, 000 Capital has increased from $18, 000 to $22, 000 = $4, 000. Because the $7, 000 stock was sold for $11, 000, which represents a profit of $4, 000. Profit increase capital. Loss would reduce the capital

Drawings The owner will want to take cash out of the business for his private use. Drawings will reduce capital Each item of drawings is not entered in the capital account A drawings account is opened, and the debits are entered there.

Accounting entries: Drawings account to be opened: n n n Dr. Drawings Cr. Cash/Purchases/Assets (the owner may take firm’s cash/assets/goods for private use. ) Drawings account to be closed: n n Dr. Capital Cr. Drawings

Example 25 August 2006 Proprietor took $50 cash out of the business for his own use. 30 August 2006 Drawings account was to be closed.

2006 Aug 25 Cash Drawings $ 2006 50 Aug 30 Capital $ 50 Cash 2006 Aug 25 Drawings $ 50 Capital 2006 Aug 30 Drawings $ 50 2006 Aug 1 Bal b/d $ 500

Balance off The balance of each ledger account can be calculated at the end of each financial period by balancing off the accounts. In computerized accounts, the balance will be calculated after the posting of ‘each transaction’.

Debit balance Debit Balance = Total amount of the “Debit” side > Total amount of the “Credit” side

Credit balance = Total amount of the “Credit” side > Total amount of the “Debit” side

Balance Carried Down (c/d) The different between the total “Debit” side and the total “Credit” side at the end of each financial period will be carried to the beginning of next financial period.

Balance Brought Down (b/d) Any balance of an account brought from the last financial period to the beginning of the current financial period will be named as “Balance b/d”

Debit Balance

Step 1 Posting the transactions to the account

Step 2 Calculate and compare the total amount of “Debit” side “Credit” side * A debit balance of $68 will be carried down to the next period.

Step 3 Carried down (c/d) the “Debit” balance to next period and inserting the total amount on each side

Credit Balance

Step 1 Posting the transactions to the account

Step 2 Calculate and compare the total amount of “Debit” side “Credit” side * A credit balance of $90 will be carried down to the next period.

Step 3 Carried down (c/d) the “Debit” balance to next period and inserting the total amount on each side

Balance Carried Forward (c/f) “Balance c/f” is the same meaning of “Balance c/d” except the balance will be carried to the next page of the account.

Balance Brought Forward (b/f) The “Balance b/f” should be appeared on the top of a new page of an account.

Trial Balance At the end of the accounting period Find errors (If there is no error, total debit entries = total credit entries) Facilitate the preparation of the trading and profit and loss account, and also the balance sheet.

Purpose of trading and profit and loss accounts To see how profitably the business is being run. Trading account n Gross profit is calculated. Profit and loss account n n n Net profit is calculated One account called a trading account, and another called a profit and loss account Combined together to form on e account called the trading and profit and loss account These accounts can therefore be seen as part of the double entry system

Trading account Gross profit is calculated. Gross profit = Sales – Cost of goods sold Gross profit = Sales – ( Purchases – Closing stock)

In Trading Account Step 1 Transfer the credit balance of the Sales account to the credit of the Trading account n n Dr. Sales account Cr. Trading account

Step 2 Transfer the debit balance of the Purchases account to the debit of the Trading account. n n Dr. Trading account Cr. Purchases account

Step 3 Remember, in this case there is no stock of unsold goods. This means that: Purchases = Cost of Goods Sold. Some of the goods bought (purchases) have not been sold by the end of the accounting period. The record the stock we have entered the following: n n Dr. Stock account Cr. Trading account

Purchases - Closing Stock = Cost of Goods Sold (what we bought in the period) (Goods bought but not sold in the period)

Step 4 If sales are greater than the cost of goods sold, the difference is gross profit. If not, the answer would be a gross loss. Sales – Cost of Goods Sold = Gross Profit

Profit and loss account Net profit is calculated. Net profit =Gross profit + income – expenses

In Profit and Loss Account Step 1 Carry this gross profit figure from the Trading account part down to the profit and loss part. n n Dr. Trading account Cr. Profit and Loss account

Step 2 Transfer the debit balances on Expenses accounts to the debit of the Profit and Loss Account. n n Dr. Profit and Loss account Cr. Expenses account

Step 3 Transfer the credit balance on revenue account to the credit side of the profit and loss account. n n Dr. Revenue account Cr. Profit and Loss account

Step 4 Transfer the net profit, when found, to the Capital account to show the increase in capital n n Dr. Profit and Loss account Cr. Capital account Gross Profit – Expenses = Net Profit

Sales 2005 Dec 31 Trading a/c (2) $ 2005 3, 850 Dec 31 Balance b/d (1) $ 3, 850 L. Sang Trading and Profit and loss account for the year ended 31 Dec 2005 Sales $ 3850

2005 Dec 31 Balance b/d (3) Purchases $ 2005 2, 900 Dec 31 Trading a/c (4) $ 2, 900 L. Sang Trading and Profit and loss account for the year ended 31 Dec 2005 Purchases $ 2900 Sales $ 3850

2005 Dec 31 Trading a/c Stock $ 300 L. Sang Trading and Profit and loss account for the year ended 31 Dec 2005 $ Purchases 2900 Less: Closing stock 300 Cost of goods sold 2600 Gross profit c/d 1250 3850 Sales Closing stock $ 3850 300 3850

Rent 2005 Dec 31 Balance b/d (6) $ 2005 240 Dec 31 Profit & loss a/c (7) $ 240 L. Sang Trading and Profit and loss account for the year ended 31 Dec 2005 Purchases Less: Closing stock Cost of goods sold Gross profit c/d Rent Lighting General expenses Net profit $ 2900 300 Sales Closing stock 2600 1250 3850 240 150 60 800 1250 $ 3850 300 3850 Gross profit b/d 1250

Vertical Style:

The Balance Sheet It is a statement showing the assets, capital and liabilities of a business at a particular date. Not part of the double entry system To list the closing balance on assets, capital and liabilities

Balance Sheet Layout Assets n n Fixed Assets Current Assets

Fixed Assets Are of long life Are to be used in the business, and Were not bought only for the purpose of resale Fixed assets are listed starting with those the business will keep the longest, down to those which will not be kept so long.

Current Assets Cash in hand, cash at bank, debtors, items held for resale at a profit (i. e. stock) or items that have a short life These are listed starting with the asset furthest away from being turned into cash, finishing with cash itself

Long-term Liabilities Repayable beyond the next accounting year E. g. Loan, Debentures

Current Liabilities Repayable within the next 12 months E. g. n n Creditors Bank overdraft

Completion of capital account Old Capital + Net Profit – Drawings = New Capital

Horizontal Style

Vertical Style

Trading and profit and loss account and balance sheet: Further Considerations Adjustments needed for stock Return inwards Return outwards Carriage inwards Carriage outwards

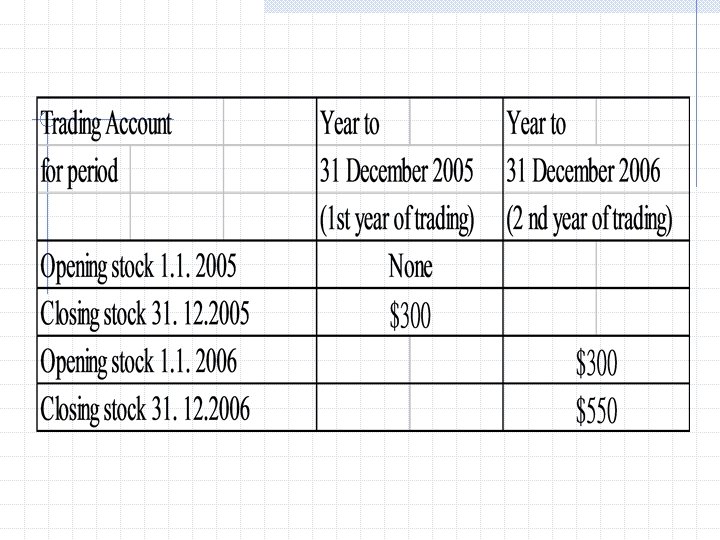

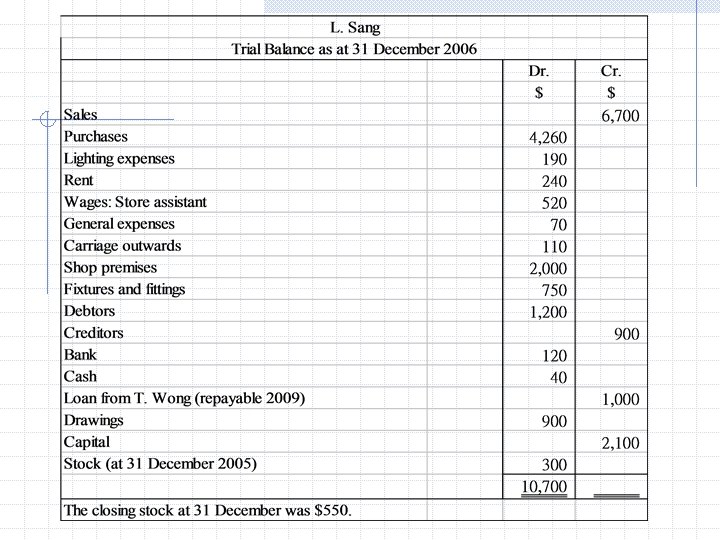

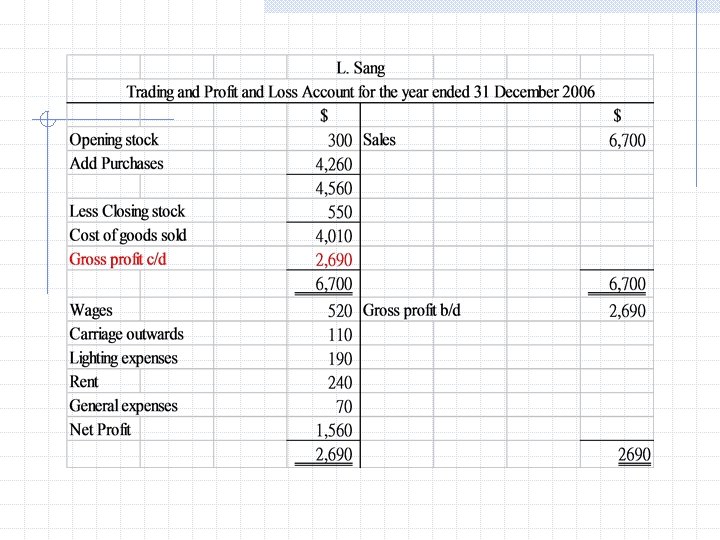

Adjustments needed for stock For new businesses only, they started without stock and therefore had closing stock only For the second year of trading, to 31 December 2006, both opening stock and closing stock figures will be in the calculations.

2005 Jan 1 Bal b/d Stock $ 2005 X Jan 1 Trading a/c $ X Trading and profit and loss account for the year ended 31 Dec 2005 Opening stock Purchase $ X Sales X $ X

Return inwards represent goods sold which have now been returned by customer To keep the actual sales of goods, return inwards is always deducted from sales in the trading account (1) (2) Dr. Return inwards a/c Cr. Debtor Dr. Trading a/c Cr. Return inwards a/c

Return inwards 2005 $ 2005 Dec 31 Bal b/d X Dec 31 Trading a/c $ X Trading and profit and loss account for the year ended 31 Dec 2005 $ Return inwards X Sales Less: Return inwards $ X X X

Carriage inwards is the cost of transport of goods into a business Suppose one supplier might sell the goods to you for $95, but you would have to pay $5 to a haulage firm for carriage inwards – a total cost of $100 Cost of buying goods Carriage inwards is always added to purchases in the trading account. The transfer is made (1) (2) Dr. Carriage inward a/c Cr. Bank Dr. Trading a/c Cr. Carriage inward a/c

Carriage inwards 2005 $ 2005 Dec 31 Bal b/d X Dec 31 Trading a/c $ X Trading and profit and loss account for the year ended 31 Dec 2005 $ Opening stock X Purchase X Add: Carriage inwards X $ Sales Less: Return inwards X X X

Return outwards represent goods which were purchasing and are now being returned to the supplier To keep the actual cost of buying goods, return outwards is always deducted from purchases in the trading account (1) (2) Dr. Creditor a/c Cr. Return outward a/c Dr. Return outward a/c Cr. Trading

Return outwards 2005 $ 2005 Dec 31 Trading a/ c X Dec 31 Bal b/d $ X Trading and profit and loss account for the year ended 31 Dec 2005 $ Opening stock X Purchase X Add: Carriage inwards Less: Return outwards $ Sales Less: Return inwards X X X Return outwards X

Carriage outwards is the cost of transport of goods to the customer of a business This is always treated as an expense to be transferred to the debit of the profit and loss account (1) (2) Dr. Carriage outward a/c Cr. Bank Dr. Profit and loss a/c Cr. Carriage outwards a/c

Carriage outwards 2005 $ 2005 Dec 31 Bal b/d X Dec 31 P/L a/c $ X Trading and profit and loss account for the year ended 31 Dec 2005 $ $ Sales X X Rent X Carriage outwards X X Gross profit b/d X

Final Accounts Final accounts are often used to mean the trading and profit loss account and the balance sheet.