SelfEmployed Womens Association SEWA 2007 SEWA is a

- 2007 SEWA is a trade union of 959, 698")

4. Insurance by and for poor women, encourages")

Comprehensive protection b) Cost efficient marketing 2.")

5. Database of member and claimant information 6. Programme-related research")

4. Maintaining good member data 5. Containing cost of selling and")

and NGOs 6. Appropriate, affordable products")

- Slides: 24

Self-Employed Women’s Association (SEWA) - 2007 SEWA is a trade union of 959, 698 women workers in the informal economy in Gujarat and 7 other states. It was founded by Elaben Bhatt.

Our Members Four major categories a. Home-based workers b. Vendors (of all types of wares) c. Manual labourers and service providers d. Producers

SEWA’s MAIN GOALS • Full Employment • Work Security • Income Security • Food Security • Social Security — insurance, healthcare, childcare, shelter, pension. Self-Reliance • Economically • Decision-making and control

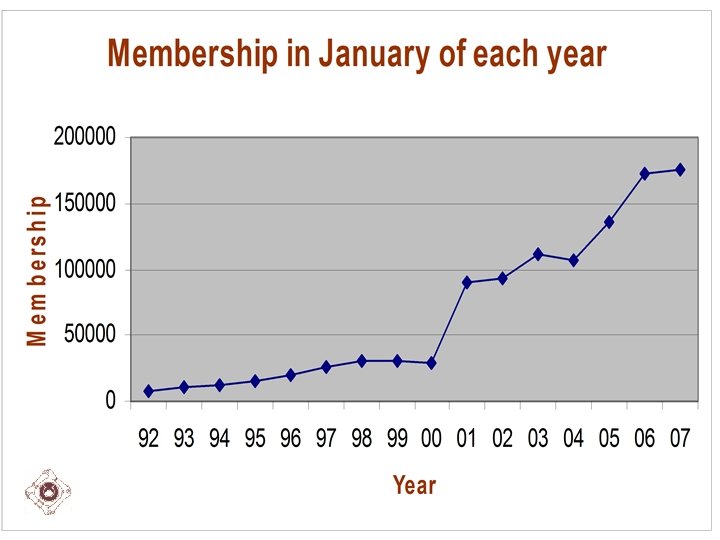

Vimo. SEWA • Started in 1992 in SEWA Bank • Vimo. SEWA separate unit in 2000 • Membership (Jan 1, 2007): 1, 75, 390 • Centered in Gujarat – plus six states

Current insurance package Product Scheme I coverage Wome n Health Asset Life 2000 Men 2000 Children 2500* 10000 7500 Women 6000 Men 6000 Children 2500* 20000 7500 Accidental Death (Member) 40000 Accidental Death (Husband) 15000 25000 Premium for the entire package 125 100 Family Discount Scheme II coverage 20000 65000 100 25 150000 275 225 100 50

Main Players MEMBER VIMO SEWA INSURANCE COMPANY • Marketing • Premium collection • Claims servicing • Data management • Research & Monitoring Risk carrier

Premium Collection - House-to-house - Through self-help groups Fixed deposit -Annual – quarterly – monthly Annual pay

Claims Servicing Documents AAGEWAN MEMBER Cheque INSURANCE CO. Documents VIMO SEWA CLAIMS COMMITTEE Bulk reimbursement

Lessons Learned - General 1. The poor are willing to pay for insurance 2. Linking insurance to other financial services provides payment options, e. g. SHGs, SEWA Bank 3. Insurance promotion can be a source of employment

Lessons Learned – General (contd. ) 4. Insurance by and for poor women, encourages organizing and contributes to economic empowerment 5. Premiums can be increased gradually, but services must be appropriate and timely

Lessons Learned – Product 1. Integrated a) Comprehensive protection b) Cost efficient marketing 2. Affordable 3. Family package

Lessons Learned – Services 1. Clear communication about reasons for decisions taken 2. At the doorstep 3. Regular member contact 4. Open-door policy

Successes 1. Acceptance of insurance as risk mgmt 2. Building grassroots cadres to market and service insurance 3. Responsive to member needs 4. Policy level recognition of insurability of poor

Successes (2) 5. Database of member and claimant information 6. Programme-related research

Challenges 1. Providing adequate protection 2. Ensuring that members understand retain information about insurance 3. Retaining members

Challenges (contd. ) 4. Maintaining good member data 5. Containing cost of selling and servicing insurance to the poor a. Issues of financial viability

Policy Recommendations 1. Integrated insurance package 2. Enabling environment — flexible regulations to encourage new, pro-poor initiatives 3. Removal of service tax (currently 12%) for micro insurance 4. Government contribution to match people’s contributions

Policy Recommendations 5. Implementation by people’s organisations (POs) and NGOs 6. Appropriate, affordable products developed with insurers, POs and NGOs 7. Reduce capital requirement from Rs. 100 crores to Rs. 30 crores for insurance cooperatives by/for the poor

Other Initiatives 1. Prompt Reimbursement System in Health Insurance 2. Weather Insurance pilot. 3. Programme Related Research.

Thank you Visit us at www. sewainsurance. org Contact us: social@sewass. org