Personal Financial Literacy Developing a Financial Plan ESSENTIAL

- Slides: 15

Personal Financial Literacy: Developing a Financial Plan ESSENTIAL QUESTION: HOW CAN EDUCATION, INCOME, CAREER, AND LIFE CHOICES IMPACT AN INDIVIDUAL’S FINANCIAL PLAN AND GOALS?

Education = $

� The sooner you begin saving, the more your individual investments are worth. � The longer the money is invested before you begin pulling it out to spend, the longer it has to mature. � Financially wise individuals begin investing in their retirement in their early 20 s.

Chart assumes a 12% ROI

Pathways to Success �Responsible citizens should plan for their future and choose a pathway that will lead them to a financially secure life. �There are many different options for students beyond high school: Entering the workforce immediately Going into the military Enrolling in a community college or technical training program Attending a 4 year college or university

�Individuals must choose between earning money now, and earning more money later. �Entering the workforce now, for example, is cheaper and you earn money immediately, however, your earning power over your lifetime is statistically decreased compared to someone who continues their education.

Increasing Student Debt

Gettin’ Paid �Workers can either earn wages or a salary. �Wages = paid by the hour Example: “I make $10 an hour as a secretary. ” �Salary = normally stated in a yearly amount Example: “I make $35, 000 a year as a teacher. ”

Creating a Personal Budget �Budget: A plan for how a person, family, or organization will raise and spend money. �Fixed Costs: Charges/costs that will be the same every month, no matter how often something is used. - - Rent/Mortgage payments: The money you owe for housing will be the same every month whether you spend one night or every night there. Car payments: Same as rent. �Variable Costs: Charges/costs that will change depending on how much of something is used. Food: eating more or buying more expensive foods will cost more. Travel: Driving more will require more gas, meaning more money. Entertainment: Choosing to go out to eat, to movies, buy video games, etc. Everything costs money. The more stuff you want to buy, the more money you will need.

Planning for your Financial Future

Social Security � The Federal Government Full retirement age is the age at which a person may first become entitled to full or unreduced retirement benefits. � No matter what your full retirement age (also called "normal retirement age") is, you may start receiving benefits as early as age 62 or as late as age 70. � If You Retire Early - You can retire at any time between age 62 and full retirement age. However, if you start benefits early, your benefits are reduced a fraction of a percent for each month before your full retirement age. � http: //www. bloomberg. com/news/articles/2016 -06 -22/social -security-will-be-there-for-you-millennials � https: //www. youtube. com/watch? v=mlx. LX 8 Fto_A

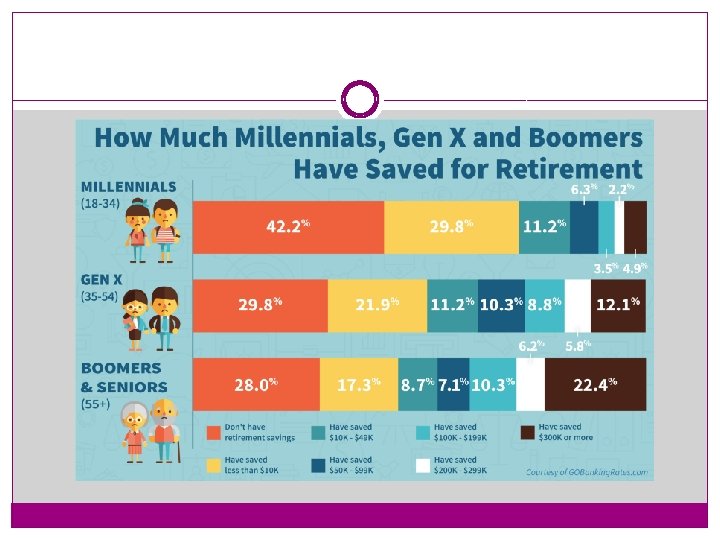

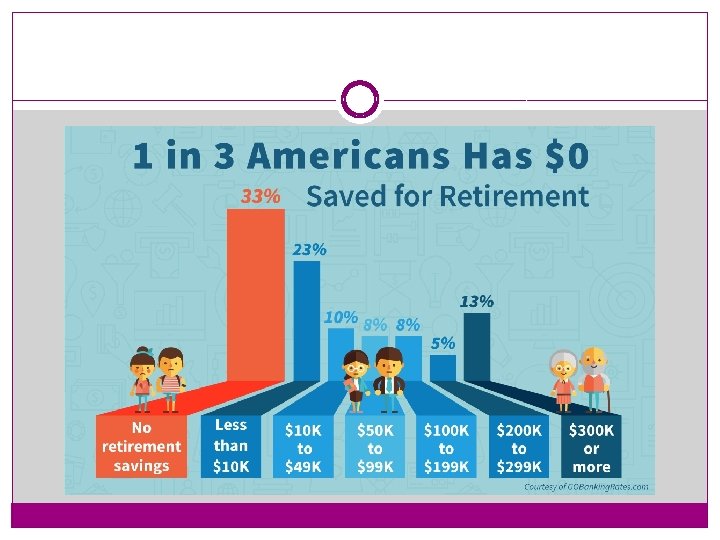

Supplemental Income �In addition to Social Security, you will most likely want/need supplemental income to maintain the lifestyle you had while working. �Social Security payments range from $1, 287 ($15, 444/year) to $2, 663 ($31, 956/year) per month. �Many people wisely choose to invest in retirement accounts which will give them additional money to spend each month.

Occupational Outlook �https: //www. bls. gov/ooh/a-z-index. htm