Lecture 11 APT and Multifactor Models Investment Analysis

- Slides: 16

Lecture 11 APT and Multi-factor Models Investment Analysis and Portfolio Management Spring 2009 CAU Business School

Revisiting Single Factor Model Single factor model of security return Two sources of security return common economy-wide factor firm specific events Possible common economy-wide factors: macroeconomic variables Gross Domestic Product Growth Interest Rates

SFM in Equation Return on security i Expected return on security i Factor loading: sensitivity of security i to factor F Factor F: economy-wide risk factor Firm specific risk

Multi-factor Models Why one factor? Isn’t it better to allow multiple factors? SFM: market return을 factor로 사용 MFM: market return, GDP growth, interest rate etc. N-factor model Can estimate the factor loadings(betas) through multiple regression approach

Multi-factor SML Typical factors: risk premium for market portfolio, premium for GDP growth risk, premium for interest rate risk etc. Generalization of SFM SML

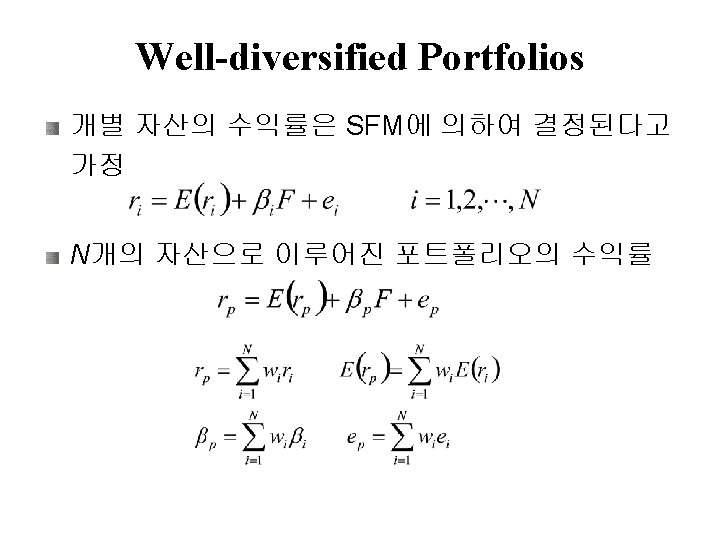

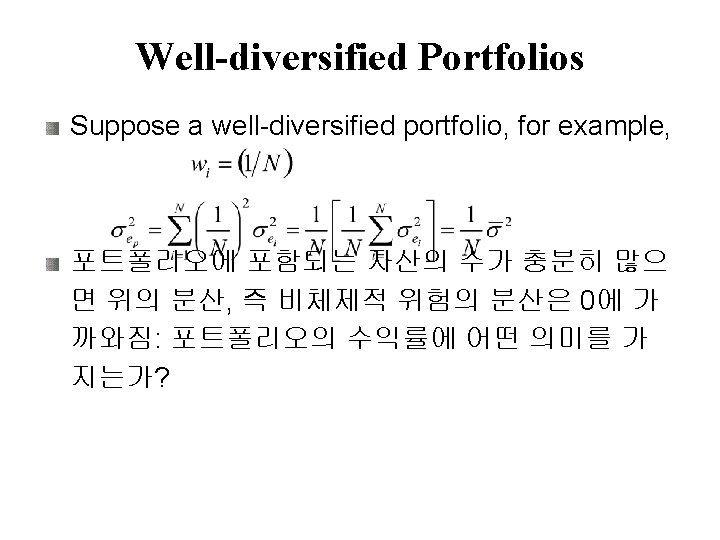

Well-diversified Portfolios Variance of the portfolio with N securities Note that Moreover,

Portfolio vs. Individual Stock

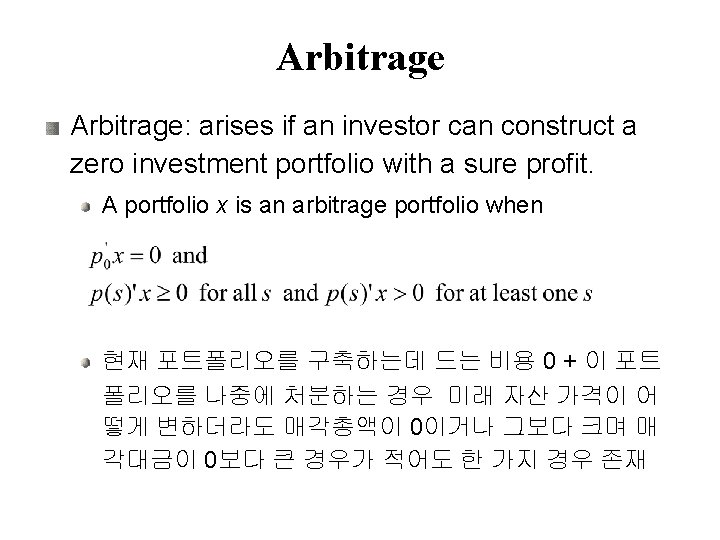

APT and Arbitrage

APT and CAPM APT applies to well diversified portfolios and not necessarily to individual stocks: CAPM applies to all individual stocks as well as portfolios. With APT it is possible for some individual stocks to be mispriced - not lie on the SML, which is not possible under CAPM. APT is more general in that it gets to an expected return and beta relationship without the assumption of the market portfolio. Market portfolio vs. well-diversified portfolio

Multi-factor APT can be easily extended to a multi-factor version. Return on security I is determined by the following MFM Then, the expected return on a well-diversified portfolio is proportional to a linear combination of its betas: APT

What are Factors? Chen, Roll, and Ross Chose a set of factors based on the ability of the factors to paint a broad picture of the macro-economy Fama and French: three factor model 3 factors: 시장포트폴리오의 수익률, 시가총액이 작은 기업의 수익률과 시가총액이 큰 기업의 수익률 차이, BTM이 큰 기업의 수익률과 낮은 기업의 수익률 차이 A well-accepted model The model includes CAPM as a subset.