Four cornerstones of your financial future Investment advisory

")

Defined benefit (Pension) Qualified under")

Used by business owners with no employees • • • Advantages over")

Example Contributions SEP SIMPLE Individual(k) Salary Deferral N/A $12, 000 $17, 500")

- Slides: 25

Four cornerstones of your financial future Investment advisory products and services are made available through Ameriprise Financial Services, Inc. , a registered investment adviser. Ameriprise Financial Services, Inc. Member FINRA and SIPC. © 2014 Ameriprise Financial Inc. All rights reserved. Vance P. Lahey, CFP® Financial Advisor Business Financial Advisor A financial advisory practice of Ameriprise Financial Services, Inc. May 13, 2015

The only constant is change ®

Solutions that work for you and your business The financial decisions you make as a business owner can affect the bottom line for your business and your personal goals. That’s why you need a plan that can help you identify what makes sense for both aspects of your life. To gain a comprehensive view of your situation, you should look at all aspects of your personal and business finances, including your: • • Cash flow Investment needs (equipment & facility improvement, personal investments) Retirement goals Business insurance and protection Estate property and hard-earned assets Taxes Exit strategy Employee benefits Focus on creating an integrated business and personal financial plan solutions tailored to your unique goals.

Solutions that work for you and your business Retirement plans and other benefits The right plans can provide tax benefits. Business protection Protecting your business means being prepared for unexpected situations. Business valuation Your business is important to you, but do you know how much it’s really worth? Business succession planning How will you transfer your business when it’s time to move on? Managing taxes As your goals and financial situation change, there may be new opportunities to reduce your taxable income. Managing personal cash flow Setting up a cash flow strategy may help you manage cash flow for business needs and meet your family’s needs and plan for your goals. Cash reserve Building adequate reserves for your business and personal needs can provide for planned or unexpected situations. Debt management Having a plan to pay off business and personal debt will help create a strong financial foundation. Saving for your goals Whether you want to buy a home, save for kid’s college or for your retirement, you need a savings plan for each goal.

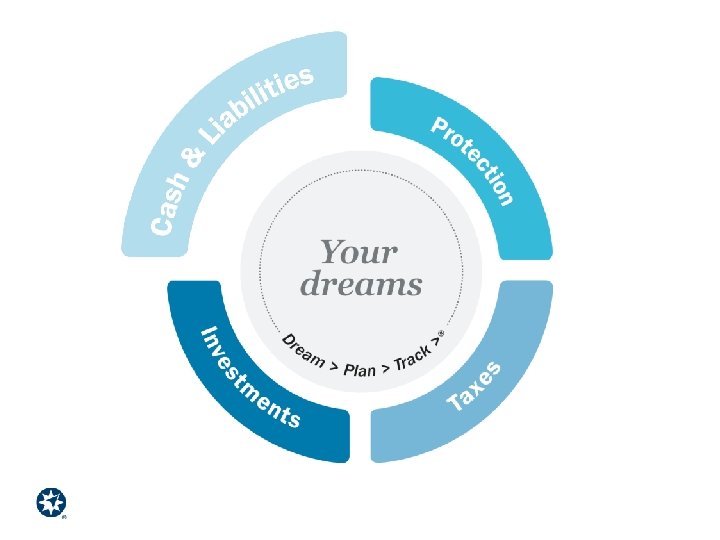

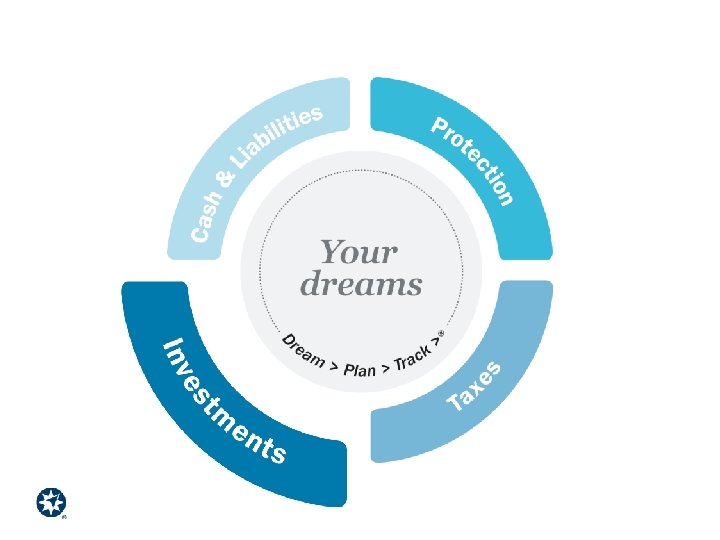

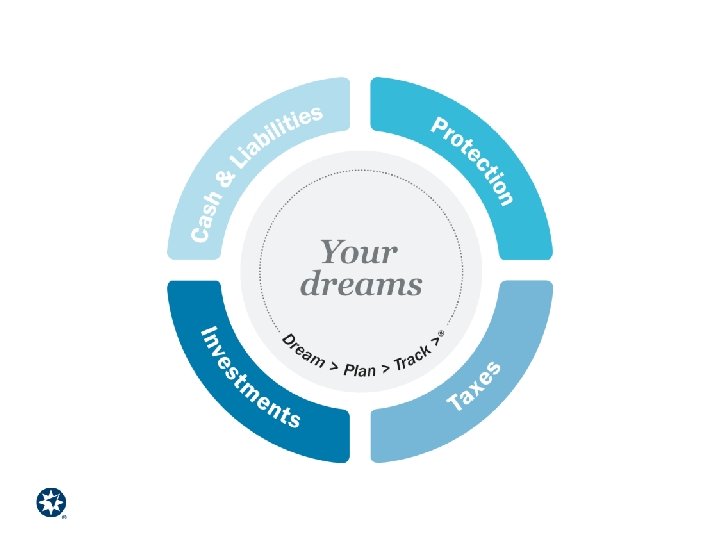

Four cornerstones of your financial life

Money in, money out Cash & liabilities

Money in, money out – planning your business and personal cash flow Separate your business and personal finances Business Income $ Business Account - Business expenses Operating expense Loan payment(s) Business cash reserve Equipment and facility improvement Personal Account - Your “paycheck” - Living expenses Personal loans & mortgage Personal cash reserve Savings for your goals Money for income taxes

Money in, money out – planning your business and personal cash flow Separate your business and personal finances Business Income $30, 000 (May Flock) Business Account - Estimated business expenses = $18, 000 Set aside $3, 000 for business cash reserve Pay yourself a “paycheck” of $4, 500 per month Personal Account - Your “paycheck” - Living expenses Personal loans & mortgage Personal cash reserve Savings for your goals Money for income taxes

Optimize your money - business Cash & liabilities Business Everyday cash Short-term cash reserve (known expenses) Long-term cash reserve (expansion or equipment replacement) High-interest balance (if any) Low-interest balance (Live Oak Loan) No-interest balance Income Business Debt

Optimize your money - personal Cash & liabilities “Personal Everyday cash Short-term cash reserve (safe & liquid) Long-term cash reserve (safe, but doesn’t have to be as liquid) High-interest balance Low-interest balance No-interest balance Income “ Personal Debts

Types of small business retirement plans IRA-based plans SEP IRA plans SIMPLE IRA plans 401(k) & Profit sharing plans Defined benefit plans Qualified retirement plans

An IRA-based plan What is it? SEP Simplified Employee Pension SIMPLE Savings Incentive Match Plan for Employees • Typically easier and more cost-effective than qualified plans • Employer-sponsored retirement plan funded through employee-owned IRAs

SIMPLE/SEP Comparison SEP Contributor & Annual Income Deferral Simple Employer Contribution Deferral Employer (Andrew) $50, 000 $0 $10, 000 $8500 $1, 500 Employee #1 $20, 000 $0 $4, 000 $600 Employee #2 $20, 000 $0 $4, 000 $600 Employee #3 $20, 000 $0 $4, 000 $600 Total employer funding cost $22, 000 $11, 800 Total employee funding cost $0 $1, 800 This example is hypothetical and does not represent an actual company or emploees.

A qualified plan What is it? Defined contribution 401(k) Defined benefit (Pension) Qualified under section IRC sec. 401(a) Typically more costly than IRA-based plans More features & larger deductions than IRA-based plans

Individual 401(k) Used by business owners with no employees • • • Advantages over SEP/SIMPLE plans Cost-savings over traditional multiparticipant 401(k) plans • • higher contribution limits plan loan feature Roth deferral option exempt from discrimination testing exempt from IRS form 5500 filing (until assets exceed $250, 000)

Individual 401(k) Example Contributions SEP SIMPLE Individual(k) Salary Deferral N/A $12, 000 $17, 500 Employer $25, 000 $3, 000 $25, 000 Total $25, 000 $15, 000 $42, 500 Assumptions: Objective: flexibility, large deduction Owner-only business $100, 000 OF W-2 income Corporate entity This hypothetical example is provided for illustrative purposes only.

Tax treatment matters Tax-free Taxable Tax-deferred Ameriprise Financial and its representatives do not provide tax or legal advice. Consult your tax advisor or attorney regarding specific tax issues.

Some attractive features… 1 After-tax dollars Tax-free withdrawals 2 No limits on conversions 4 Roth IRA 3 Limits on contributions A Roth IRA is tax free as long as you leave the money in the account for at least 5 years and are 59½ or older when you take distributions or meet another qualifying event, such as death, disability or purchase of a first home.

Take action now.

Disclosures Investment products, including shares of mutual funds, are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value. Before you purchase a life insurance policy or annuity contract, be sure to ask your financial advisor to explain the features, benefits, risks and fees, and whether the product is appropriate for you based upon your financial situation and objectives. Variable annuities and variable life insurance are complex investment vehicles that are subject to market risk, including the potential loss of principal invested. Annuities are longterm insurance products. You should consider the investment objectives, risks, charges and expenses of the variable annuity/life insurance and its underlying investment options carefully before investing. For a free copy of the annuity/life insurance prospectus and underlying investment's prospectus, which contains this and other information about variable annuities/life insurance, go to ameriprise. com or contact your financial advisor. Read the prospectus carefully before you invest. Stock investments have an element of risk. High-quality stocks may be appropriate for some investments strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with stocks before investing, as they can lose value. There are risks associated with fixed income investments, including credit risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced in longer-term securities. Investments in a narrowly focused sector such as real estate may exhibit higher volatility than investments with broader objectives. An investment in real estate is subject to market risk, economic risk, and mortgage rate risk. International investing involves increased risk and volatility due to potential political and economic instability, currency fluctuations, and differences in financial reporting and accounting standards and oversight. Risks are particularly significant in emerging markets. Funds held in an identified FDIC insurable account will be FDIC insured up to a maximum of $250, 000 per depositor at a member bank, and any amount deposited above $250, 000 will not be covered by FDIC deposit insurance You may incur a penalty for early withdrawal and withdrawals and fees may reduce earnings on a Certificate of Deposit. Investment advisory products and services are made available through Ameriprise Financial Services, Inc. , a registered investment adviser. Ameriprise Financial Services, Inc. , Member FINRA and SIPC. .