FHA 203k Program Overview Sagamore Home Mortgage LLC

Program Overview Sagamore Home Mortgage LLC Presented by – Tom Connors Account")

Program")

? § A fully disbursed 1 st Mortgage with escrow")

Loans §Purchase and refinance §Fixed and Adj. rates §Standard FHA loan limits")

§ Two formats: Standard 203(k) & Streamlined 203(k) (Limited Repair)")

§ Not all lenders offer FHA 203(k) Standard § With a consultant")

§Limited Repairs § 1 to 3 Specialized Contractors §Fixed remodeling plans §No")

§ Consultants: Partners in")

?")

? § Consultants are the key to a successful program")

• Discuss desired repairs &")

§Credit is credit §Maximum Mortgage Worksheet – includes all the renovation")

- Slides: 27

FHA 203(k) Program Overview Sagamore Home Mortgage LLC Presented by – Tom Connors Account Manager February 19, 2015

Today’s Overview 1 • Where does it fit in today’s market? 2 • What is the FHA 203(k)? 3 • How do we start Originating 203(k)’s

Today’s Market Always a Market

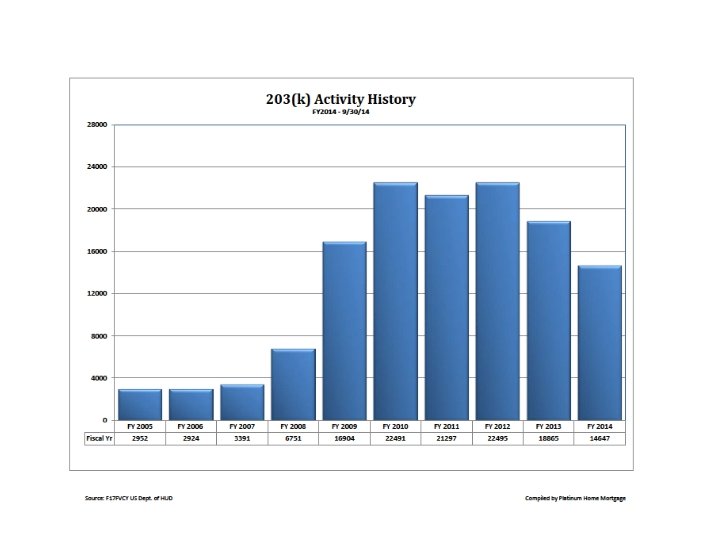

In the News § Harvard’s Joint Center for Housing is projecting a steady growth in remodeling this year § National Mortgage News article points to double digit growth § Continued low interest rates for first mortgages encourage renovation.

Where is the market? § Any home completed for at least one year § Foreclosures and short sales § Older neighborhoods – outdated homes § Refinance Stated Purpose – Home Improvements § Borrowers with Limited to No Equity

Benefits to Borrowers § Can buy location and make the house the way they want it – now § One closing for the mortgage and improvements § Borrower chooses the improvements that are done after closing § Create Equity on Purchase or leverage

Advantages to you §Differentiate yourself from or eliminate competition §Attract or Retain more Realtors, Customers or builder/remodeler referral sources §Larger loans with better collateral

More advantages to you ! §Less rate/price sensitive than “commodity” products §Close more loans – nearly every major or minor project imaginable is allowed §Only new swimming pools, hot tubs and other “luxury items” are ineligible

203(k) Program

What is the FHA 203(k)? § A fully disbursed 1 st Mortgage with escrow established for repairs and improvements § Fixed Home Improvement Plan in place at closing § Not an open ended Equity Loan/Line § Escrow Funds Disbursed at or after closing

All 203(k) Loans §Purchase and refinance §Fixed and Adj. rates §Standard FHA loan limits and MIP §HUD REO & $100 Down §GNND § 1 -4 Family Owner Occupied. Conversions

Eligible Improvements? § Additions-expansions -unfinished space § Functional Obsolescence–Deferred Maintenance § Remodel kitchens & baths – flooring § Replace Mechanical Systems or appliances § Windows-siding-roofing - garages, decks

Standard vs. Streamlined 203(k) § Two formats: Standard 203(k) & Streamlined 203(k) (Limited Repair) § Regular FHA loan which incorporates a remodeling plan as part of the mortgage § Loan is saleable and insurable right after closing § Up to six months to complete the renovation

Standard 203(k) § Not all lenders offer FHA 203(k) Standard § With a consultant and a general contractor, the loan moves more quickly § More projects can be done – Bigger Loans!

Streamlined 203(k) §Limited Repairs § 1 to 3 Specialized Contractors §Fixed remodeling plans §No changes or extensions §Simple uncomplicated projects

Extended Benefits § Reputation and referrals for success with 203(k) § Consultants: Partners in a successful program § Realtors: Sell more homes faster § Contractors: Better projects with assured

Ready to start with 203(k)?

How do we add 203(k)? § Consultants are the key to a successful program § Required for Standard & recommended for Streamlined § Lender Locates FHA Consultants in your lending areas (Lender Select) § Interview and get samples of Work Write-

Consultant = Great Resource for you and your customer! § Evaluates the property for required work, suggested work and borrower’s wish list § Does a feasibility study or work write-up and cost estimate or evaluates bids for Streamlined 203(k) § Fee can be financed in the mortgage § Helps the appraiser to “see” the after- improved value for better appraised value

What happens next? • Pre-Qualify Borrower (Credit is Credit) • Discuss desired repairs & improvements • Educate Borrower on Loan Product via the 203(k) Borrower’s Acknowledgment • Complete the Maximum Mortgage Worksheet • Are they ready for a consultant?

Underwriting the 203(k) §Credit is credit §Maximum Mortgage Worksheet – includes all the renovation and fees into the loan §After-improved Appraisal includes the project

Closing §Loan close in normal time frames §Obtain Building Permits and Contractor begins work on the project §Loan is purchased & escrow established at Platinum Home Mortgage

Managed Draw = Platinum § Your Borrower, Consultant, Contractor and other vendors contact or are contacted by Platinum Home Mortgage § We order inspections, title updates etc……. § Anticipate checks – 5 to 7 business days from inspection § Checks sent directly to customer same day request is complete

Managed Draw – Continued § We post and pay interest on escrow at. 10% § Any financed mortgage payments are automatically applied when due § We provide the customer and you with ongoing accounting § We manage towards final completion, final accounting and case close out

PHMC Customer Focus §Our Turn Around Times are always same day or next day on each step in the process §Our goal is a completed project and a satisfied customer, Realtor, Builder/Remodeler

Questions? § Tom Connors Account Manager § tom. connors@phmc. com § Direct: 518. 280. 0188 x 213 855. 847. 7462 x 213 § Doug Woodley Toll Free: Product Support Representative § douglas. woodley@phmc. com § Direct: 518. 280. 0188 x 212 Toll Free: