Critical Impacts of COVID19 on Employer Sponsored Retirement

Waiver Suspends RMD requirement for certain participants Ø For participants")

How to treat pay")

- Slides: 29

Critical Impacts of COVID-19 on Employer Sponsored Retirement Plans

WE ARE HERE TO HELP! • We know there’s a lot of information to understand. • Thank you for trusting us to share our knowledge with you. • We are presenting details as they stand today. Information presented could be changed in the near future. • If you have a question, add it to the Q&A chat located at the bottom of your screen. We have turned off raising hands and anonymous questions. • We will try to address questions at the end of the presentation. Please reach out to your professional for additional assistance. • Presentation is being recorded and will be available on our website.

TODAY’S PRESENTERS Diane Nesbit, CPA CARES Act impact on retirement plans Grant Halverson, CPC, QPA, QKA, CPFA Impact of COVID-19 on economy and retirement plans Scott Czaja, CPA EBSA and other regulatory updates

DIANE NESBIT, CPA SENIOR MANAGER LARSON & COMPANY CARES Act Impact on Employer Sponsored Retirement Plans Overview: 1. Adoption and eligibility 2. Coronavirus-related distribution 3. Plan loan availability 4. Waiver of RMDs 5. Funding relief for certain DB plans

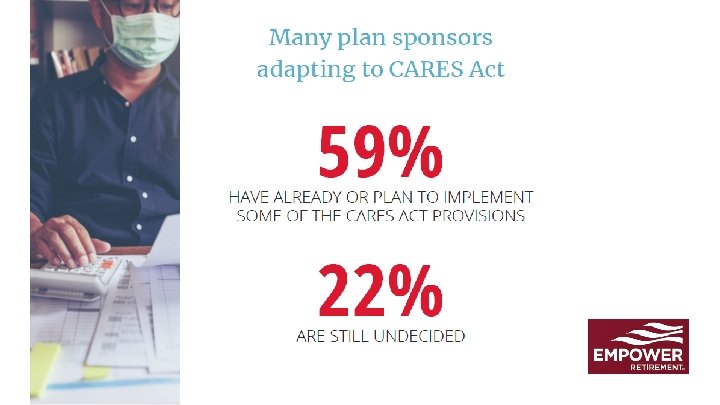

CARES Act Provisions Adoption Requirements Ø Employer sponsored retirement plan provisions of the CARES Act are optional Ø Plan sponsors can pick and choose which provisions to adopt Ø If adopted, provision must be offered to all plan participants Ø A plan amendment is required for each provision that is adopted by end of plan year 2022 Ø Plan service providers have defaulted to auto-adopt Ø National Association of Plan Advisors has put together a list of service providers and the defaults for each provider

Plan Service Providers – CARES Act Adoption Defaults https: //www. napa-net. org/sites/napa-net. org/files/CARES_Act_TABLE_0420. pdf

Plan Participant Eligibility for Relief Eligibility for relief is available to any participant: Ø Who is diagnosed with the virus Ø Whose spouse or dependent is diagnosed with the virus Ø Who is unable to work due to loss of childcare related to the virus Ø Who experiences financial hardship due to being: Ø Quarantined, furloughed, laid off, or forced to reduce work hours due to the virus Plan sponsor can rely on participant representation: Ø No doctor note or other specific documentation is required Ø Doesn’t specify if representation has to be in writing Ø Best practice recommendation is to get it in writing

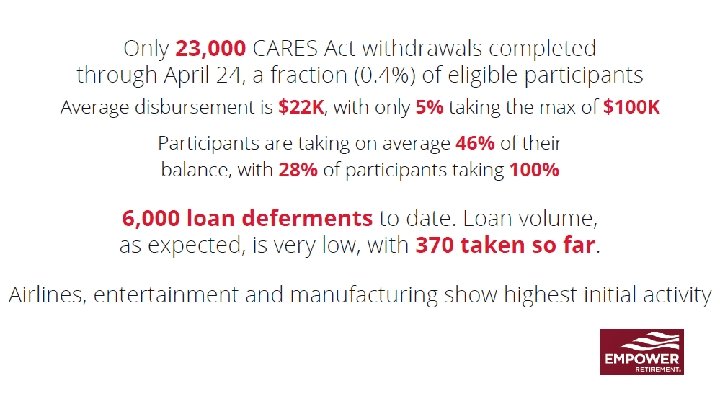

Coronavirus-Related Distribution Participants who meet the criteria are eligible for a new type of distribution Ø Intended to help with negative tax consequences Ø Waives the early withdrawal 10% penalty Ø Waives the required 20% federal tax withholding at the time of distribution Ø Distribution is still taxable, but can be spread across up to three years in equal installments Ø Distributions can be taken by the participant from multiple plans Ø Applies to distributions taken during calendar year up to $100, 000 Ø Retroactive to January 1, 2020 Ø Applicable to IRAs

Distribution Repayment Participants who meet the criteria are eligible for a new type of distribution Ø Option to repay to the plan over time Ø Window is three years from the date distribution is received Ø Can repay all or some in installments or a lump sum Ø Repayments are treated as rollovers into the plan Ø Not necessary to break out repayments between deferral, match, etc. Ø Plan sponsor responsibilities for tracking distributions and repayments Ø Don’t allow any participant to receive more than $100, 000 in distributions from the company’s plan Ø Repayments don’t have to be paid in to the same plan distributions were taken from Ø It is the participant’s obligation, not the plan sponsor’s, to ensure repayments do not exceed the total distribution amount

Loan Availability and Postponed Payments Loan Availability Ø Loans are not capped at lesser of $50, 000 or 50% of vested balance Ø Cap is now lesser of $100, 000 or 100% of vested balance Postponed Payments Ø Applicable to new or existing loans Ø Any payments due between March 27, 2020 and December 31, 2020 can be postponed for up to one year Ø Interest continues to accrue Ø Extends the 5 year cap on repayment by one year

Require Minimum Distribution (RMD) Waiver Suspends RMD requirement for certain participants Ø For participants who had reached age 70 ½ prior to 2020 Ø Secure Act changed the age to 72 beginning in 2020 Ø Available to all participants required to take an RMD – do not have to meet Coronavirus eligibility requirements Why suspend RMDs? Ø RMDs are based on participant balance as of last day of the previous year Ø Due to the significant market drops, the 2020 RMD calculation would be a larger percentage of the participant’s plan balance Ø If an RMD was already taken, it can be put back into the plan as a rollover to defer taxes (RMDs are not usually eligible to be rolled over) Ø NOTE: Also suspended initial RMDs that were due by April 1, 2020

Defined Benefit Plan Funding Relief Funding relief is provided in two ways Ø Due date for 2020 contributions is extended to January 2021 Ø Companies can use their plan’s funded percentage (AFTAP) for the immediately preceding plan year to determine the plan’s funded status for the 2020 plan year. Ø This provides relief from the current market volatility

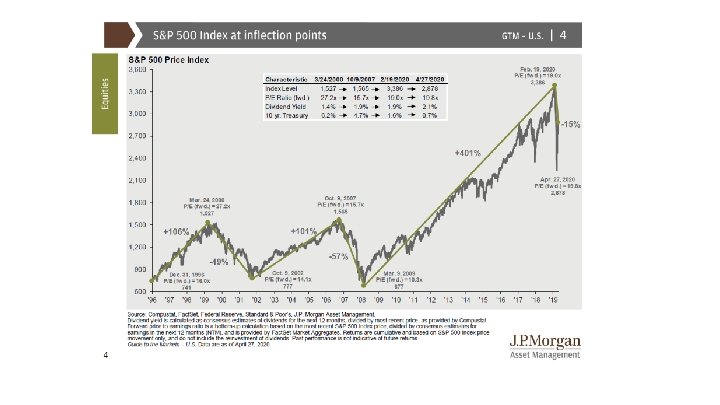

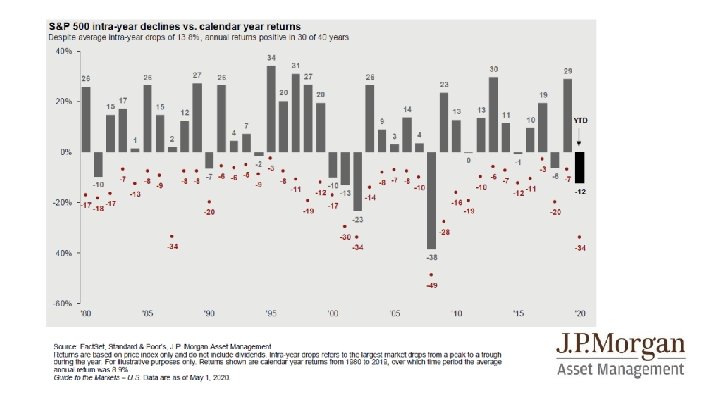

GRANT HALVORSEN, CPC, QPA, QKA, CPFA VP RETIREMENT PLAN CONSULTING HUB INTERNATIONAL Impact of COVID-19 on economy and retirement plans

How has your recordkeeper/TPA handled the implementation process of CVD and CVL? Did your employer adopt these provisions?

Has your employer eliminated your match?

Consequences of removing the match • Safe harbor plans – ADP and Top Heavy testing • Discretionary match • Plan year match funded per pay period • Match calculation period • Plan document wording

Administration Questions • • Families First Coronavirus Response Act (FFCRA) How to treat pay while on furlough Temporary layoff’s Partial plan terminations Do Furloughs and Temporary Layoff’s create distributable events beyond Covid-19 distributions?

What should plan fiduciaries be doing differently? • Follow your investment policy statement o Asset allocation of target date funds • Understand if you opted into the distribution and loan provisions without knowing it.

SCOTT CZAJA, CPA TAX PARTNER WSRP EBSA and other regulatory updates

EBSA IRS PBGC FORM 5500 1. EBSA Disaster Relief Notice 2020 -01 2. IRS COVID-19 Emergency Website 3. IRS Rev. Proc. 2018 -58 4. IRS Notice 2020 -23 Form 5500 will be extended through October 15 for a calendar-year plan.

QUESTIONS? Check out our COVID-19 resources page: https: //larsco. com/covid-19 -resources/