Unit 10 Classified Financial Statements Purpose of Financial

- Slides: 10

Unit 10 – Classified Financial Statements

Purpose of Financial Statements • Is to provide financial information about a company to owners, investors, management, creditors, and government. • Provide more information/in a way that is more easily interpreted: – Classifying items on statements into special categories. • Which debts must be paid within a year? • Is there sufficient cash (or assets) on hand to pay debts? • Which debts must be paid in future years? (Figure 5. 6 – Page 173)

Assets • Current Assets – Is cash or some other asset that, in the normal course of operations, will be converted to cash or sold or consumed within the year. – Listed in order of liquidity. Current Assets Cash Government Bonds (easily converted to cash) Marketable Securities (easily converted to cash) Accounts Receivable (due within 30 days) Prepaid Expenses (expense payments made in advance) Ex: prepaid insurance and prepaid rent

Assets • Fixed Assets – Are assets that have a long life (over one year). – “plant and equipment” or “capital assets” – Longest life fixed assets listed first – Recorded using the price at which they were purchased (cost principle) Fixed Assets Land Building Equipment Delivery Trucks

Liabilities • Current Liabilities – Are liabilities due to be paid within a year. – Listed in order that they are to be paid Current Liabilities Accounts payable Taxes payable Salaries payable Loans payable • Long-Term Liabilities – Are liabilities that are not due to be paid for more than one year. – Examples: Loan payable in 2 years Mortgage payable in 25 years

Owner’s Equity • Increases – Net income • Decreases – Net loss – Owner withdraws assets from the business ** See 2 examples (Pages 178 -179) …Fig. 5. 7, 5. 8

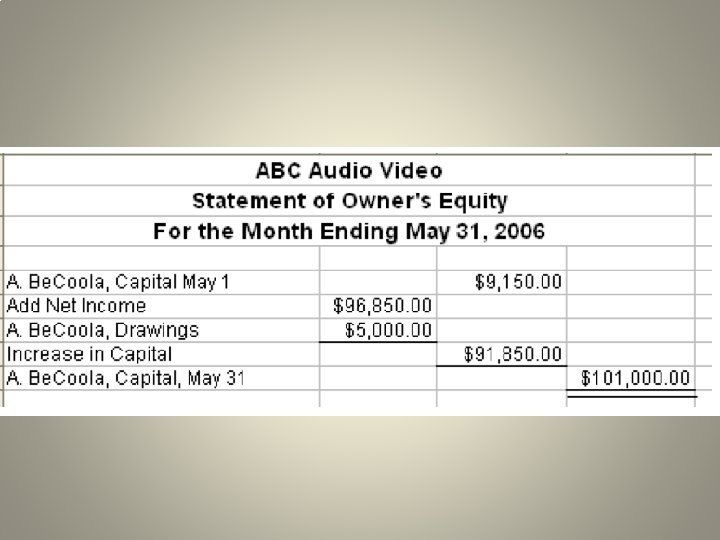

Supporting Statements & Schedules • Statement of Owner’s Equity – describes the changes in owner’s equity for the accounting period. – Gives details of owner’s equity – Prepared separately from the balance sheet – Date (for month ended) – Figure 5. 9 (Page 179)

Schedule of Accounts Receivable • Supporting schedule – provides details about an item on a main statement. – Example: Schedule of Accounts Receivable • List of the individual accounts receivable and the amounts owed. ** Supporting schedules and statements may be prepared whenever the accountant feels they would provide additional useful information for the readers of the financial statements.

Goldman’s Gym Schedule of Accounts Receivable November 30, 20 R. Getzlaf J. Benn E. Kane J. Van Riemsdyk C. Perry R. Nash E. Karlsson A. Pietrangelo D. Phaneuf M. Giordano J. Franzen C. Schneider $ 250 200 300 100 250 250 300 100 200 Total Accounts Receivable $ 2 600