Strategic performance measurement systems Henri Teittinen Agenda Performance

")

What is the")

• Practice, Innovation • Future")

")

• MCS")

• Difficulty")

- Slides: 18

Strategic performance measurement systems Henri Teittinen

Agenda • • • Performance measurement systems Performance measurement, by August Simons Levers of Control Kaplan & Norton, Balanced scorecard KCI Konecranes DAP BSC • • Malmi & Brown, Control Package Alvesson et al. Teittinen et al. Public listed companies vs. SME’s vs. Start Up’s vs. Public Organizations • Summarizing the course

• Basic levers of control (Simons 1995)

Ferreira & Otley 2009

Key issues in performance measurement How to measure? (formula, to calculate) What is the target level in measure? Who is responsible to reach the target? Where the data will be gathered? To whom the measure will be reported? How often the measure will be reported? Where the measure will be (officially) discussed? (Board of Directors? Weekly? Monthly? ) • How is it able reach the target level? (Cause and effect) • How to avoid manipulation? • •

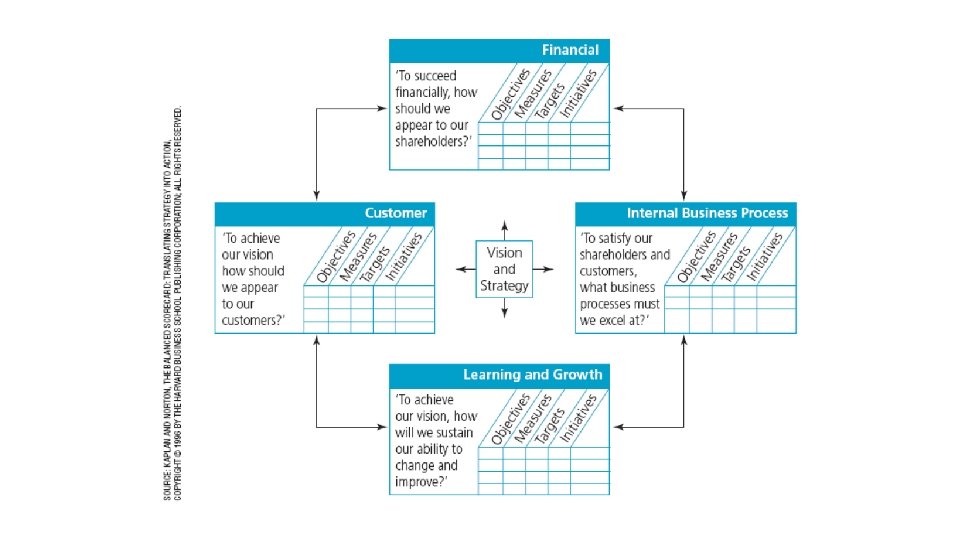

Balanced Scorecard • BSC, Background (Kaplan & Norton, 1992) • Practice, Innovation • Future oriented, Financial and Non-financial measures, Internal and external measures • A tool for strategic management • Different perspectives • • Financial Customer Internal processes Learning and growth • BSC seeks to link performance measures to an organization’s strategy • Should be used to clarify, communicate and manage strategy. 6

BSC • BSC Advocates looking at the business from four different perspectives by seeking to provide answers to the following four basic questions: • • How do our customers see us? (customer perspective) What must we excel at? (internal business process perspective) Can we continue to improve and create value? (learning and growth perspective) How do we look to shareholders? (financial perspective) • A critical assumption of BSC is that each performance measure is part of a cause-and -effect relationship. • The BSC consists of two types of performance measures: • Lagging measures • Leading measures

Designing BSC 1. 2. 3. 4. 5. 6. Vision Strategy Financial targets Critical success measures in Customer perspective Critical success measures in Internal processes Critical success measures in Learning and Growth

Atkinson & Kaplan (2007)

Balancing the measurement • Financial and Non-financial, appr. 20/80%. • Leading measures and performance measures • External measures (shareholders, customers) and internal measures. • Shot and long term measures Yrityksen taloudellinen johtaminen 12

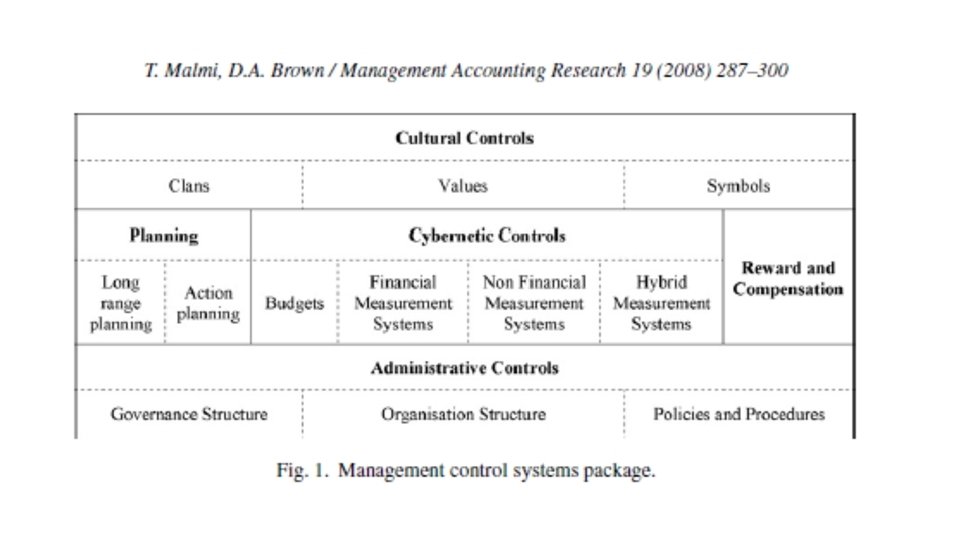

Why study management control systems as a package? Malmi & Brown (2008) • MCS do not operate in isolation. • The use and impact of a new MCS element is related to the functioning of the existing broader MCS package. • Limited understanding of the impact of other types of control (such as administrative or cultural) and whether/how they complement or substitute for each other in different contexts. • Broader package approach to the study of MCS • Better theory: How to design MCS packages.

Why study management control systems as a package? Malmi & Brown (2008) • Difficulty to clearly define the concept of MCS. • Distinction between MCS and information/decision-support systems. • What is supposed to control; is it human behaviour or artefacts, such as cash or material flows; and at what level, the organisation, business unit, management, or individual?

Management control frame for flexibility • http: //www. doria. fi/bitstream/handle/10024/143715/Juhlakirja_Gra nlund_2017. pdf? sequence=2&is. Allowed=y • Teittinen et al. p. 205 • Taipaleenmäki p. 175

Management control frame for expertize / consulting organization

Benchmarking Performance • Benchmarking • External, Internal, Target level of performance, Innovations • Internal benchmarking: BU competitions, Rankings, Bonuses • Divide one BU to two BU’s • Performance audit • Coordinated, Criteria, Competitions: Quality