Monetary Policy and the Transmission Mechanism in Thailand

analysis – Dynamic system of equations – Minimal assumption")

: 1. GDP displays U-shaped response, trough")

• Transmission primarily through interest rate and bank lending channels •")

- Slides: 30

Monetary Policy and the Transmission Mechanism in Thailand By Piti Disyatat Pinnarat Vongsinsirikul

Motivation • Understanding transmission mechanism key to successful conduct of monetary policy – Time lag – Channels of transmission • Compare with evidence from other countries • How has the crisis affected monetary transmission?

Presentation Outline • The main channels of monetary transmission • Interest rate pass-through • Response of key macro-variables to monetary shocks • Relative importance of each channel • Summary and conclusion

Monetary Transmission Mechanism Transmission Channels S-T Interest Rate Central Bank OMO Interest Rate Credit Exchange Rate Asset Price Output and Inflation

Interest Rate Pass-Through To Retail Rates Methodologies 1. Dynamic Multiplier Model 2. Error Correction Model (ECM)

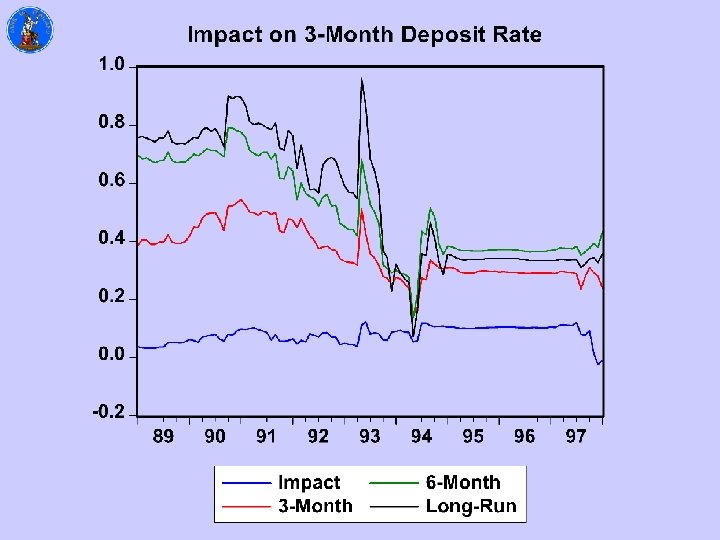

Pass Through of RP to 3 -Month Deposit Rate Methodology Period Impact Immediate 3 -Month 6 -Month Long-Run Multiplier Method 89 M 1 -95 M 12 0. 057 0. 402 0. 612 0. 7 89 M 1 -02 M 3 0. 059 0. 317 0. 399 0. 429 ECM Speed of Adjustment 89 M 1 -95 M 12 0. 5 0. 147 89 M 1 -02 M 3 0. 35 0. 07

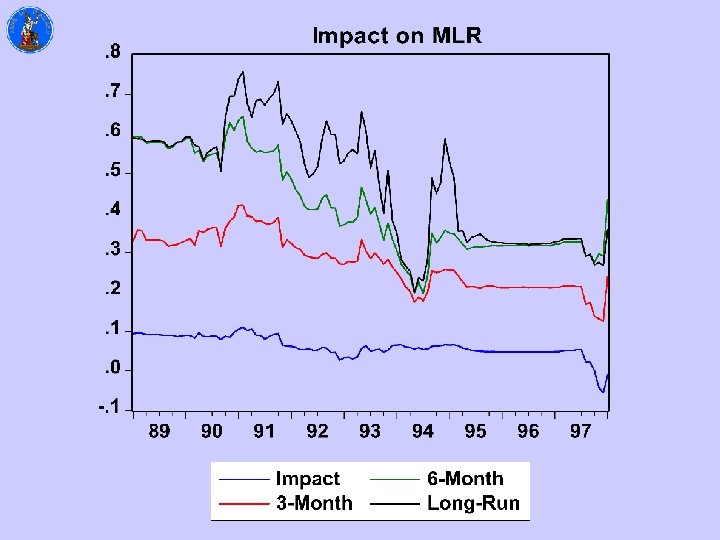

Pass Through of RP to Minimum Lending Rate Methodology Period Impact Immediate 3 -Month 6 -Month Long-Run Multiplier Method 89 M 1 -95 M 12 0. 089 9. 328 0. 521 0. 558 89 M 1 -02 M 3 0. 041 0. 239 0. 356 0. 389 ECM Speed of Adjustment 89 M 1 -95 M 12 0. 4 0. 101 89 M 1 -02 M 3 0. 356 0. 08

International Comparison of MLR Pass-Through

Justification for Interest Rate Stickiness in Thailand • High switching cost during economic downturn and fewer alternative sources of funds • Credit rationing due to asymmetric information • High liquidity • Social pressure • Posted rate

Response to Monetary Shocks • Time lags • Channels of transmission

Methodology • Vector Autoregressions (VARs) analysis – Dynamic system of equations – Minimal assumption about structure of economy – Evidence for other countries readily available • RP 14 indicator of monetary policy • Sample: 1993 Q 1 to 2001 Q 4

Basic Model: GDP, CPI, RP 14: 2 Lags • U-shaped output response, maximum impact after 4 -5 quarters

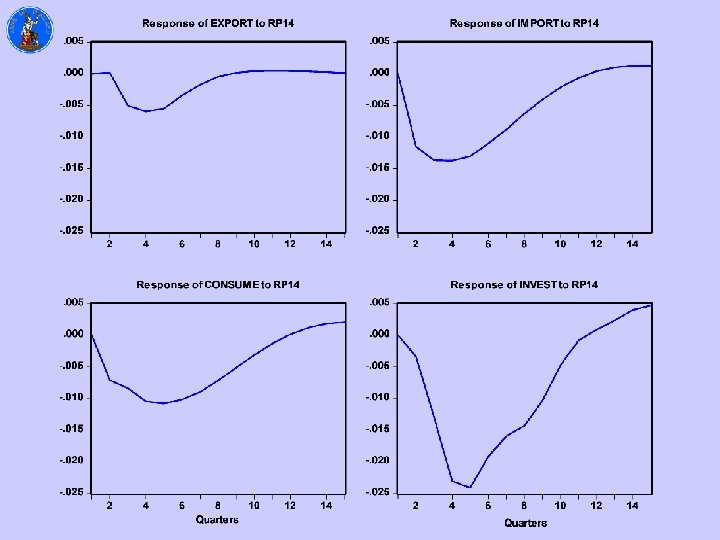

Components of Aggregate Demand • Private Consumption • Investment • Export • Import

Channels of Monetary Transmission • Augment basic model with variable that represents each channel • Compare output response with and without the relevant channel operating

Bank Lending Channel • Heavy reliance on bank finance in Thailand Private credit to GDP ratio (average for 1995 -2000)

Bank Lending Model • GDP response larger • LOANS fall after 3 quarters • PRICE falls after 4 quarters

Bank Lending Channel

Credit intensity of production has fallen Re-estimate over 1993 Q 1 to 1999 Q 1: • Impact of RP 14 on GDP and LOANS larger • Impact of LOANS on GDP larger

Bank Lending Channel: 1993 Q 1 -1999 Q 1

Exchange Rate Channel

Asset Price Channel

Direct Interest Rate Channel

Summary Model

Conclusion Stylized Facts (In Response to a Tightening): 1. GDP displays U-shaped response, trough after 4 -5 quarters and dissipating after 11 quarters 2. GDP displays U-shaped response, trough after 4 -5 quarters and dissipating after 11 quarters 3. Investment most sensitive component of GDP

Conclusion (cont. ) • Transmission primarily through interest rate and bank lending channels • Role of banks declined in recent years - Lower interest rate pass-through - Weaker bank lending channel

Looking Forward • Bank health and corporate balance sheets • More sensitivity of retail rates • Wider share ownership • Greater access to credit: Financial Master Plan • Resolution of FIDF problems

Implications for Monetary Policy • Significant lags involved in monetary transmission • These lags change over time • Must be forward-looking – Rely on accurate forecasts – Constantly look out for structural changes in the economy