Merchandising Companies Accounting for Sales and Purchases USING

Gross profit is calculated")

- Slides: 26

Merchandising Companies Accounting for Sales and Purchases USING VARIOUS EXAMPLES FROM A FICTITIOUS COMPANY, WE WILL WALK THROUGH SALES AND PURCHASES OF MERCHANDISE

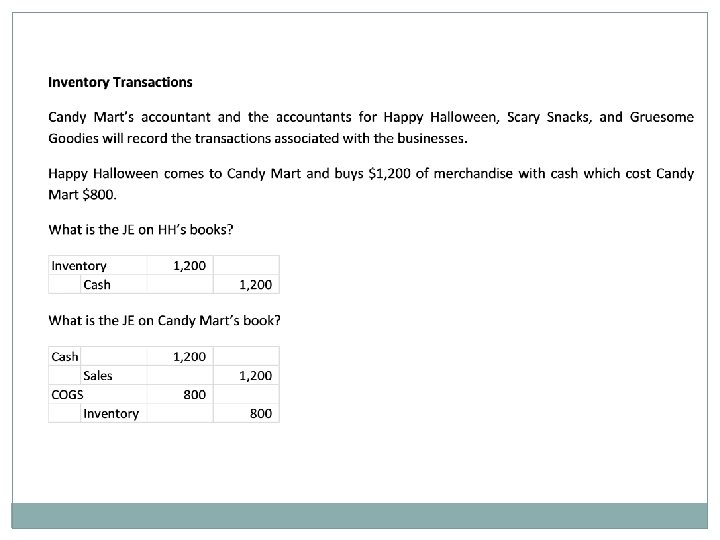

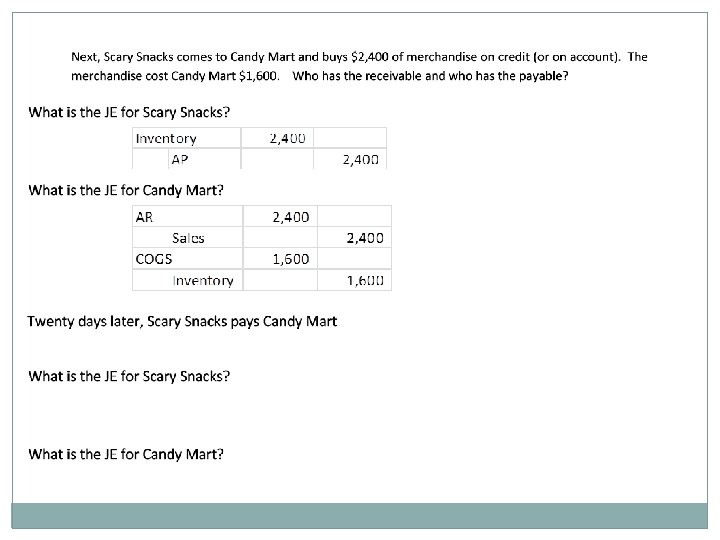

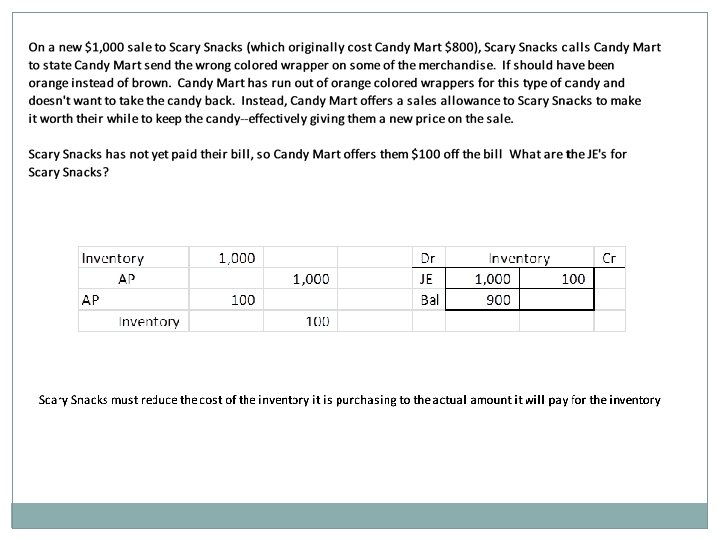

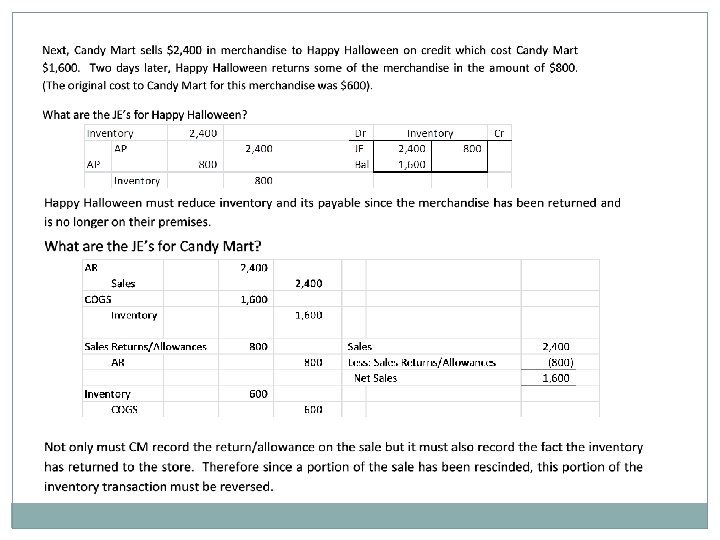

Merchandising Companies This chapter is about a new type of company which sells merchandise and not services. We will learn about this type of company by looking at various transactions for a seller and purchaser of merchandise. Merchandising companies are either 1) wholesalers who buy from manufacturers and sell to retailers or 2) retailers who buy from either manufacturers or wholesalers and sell to the final customer. We will use a local retail company named “Candy Mart” which purchases from the large candy manufacturers and sells to local candy stores for Halloween baskets. The store’s clients are Happy Halloween, Scary Snacks, and Gruesome Goodies.

As a merchandiser, Candy Mart has this amount of candy at October 1, 20 xx.

At the end of the month: What can happen to Goods Available for Sale (GAFS) during the month? Usually COGS is calculated as: Cost of Goods Sold represents the costs of buying and preparing merchandise for sale

Typically, revenues refer to service companies; whereas sales refer to merchandising companies.

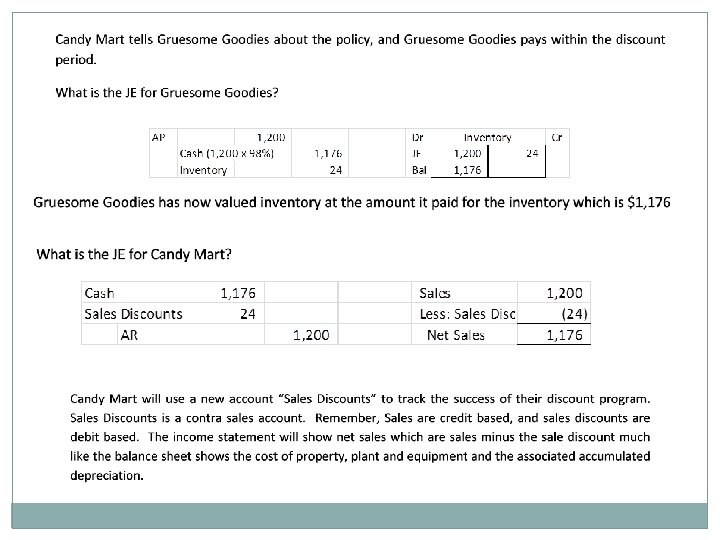

This is a representation of the gross method of sales discount

How do returns and allowances affect the purchase discount when the bill is ultimately paid?

Multi-Step Income Statement Note: Gross Profit (Net sales minus COGS) Gross profit is calculated as GP/Net Sales which yields 27%. This means there is 27% of income available for other expenses after paying the costs of inventory (GOGS). Inherently, the computation is saying 73% of net sales is spent on purchasing inventory.

Classified Balance Sheet for Merchandisers • Operating cycles for companies are usually one year—the definition is a year or the company’s operating cycle which ever is longer. • The company’s operating cycle is defined as the time span from which cash is used to acquire goods/services until cash is received from the sales of goods/services. • Operating cycles determine which assets are expected to be used up in the current period and are classified as “current. ” • If an item is not deemed “current, ” it is considered to be long-term. • Operating cycles for merchandisers are usually less than a year. • Inventory is always a current asset.