Companies Act 2013 An Insight into Latest Amendments

D.")

Third Amendment")

Appointment of RTA, Execution")

ORDER, 2019.")

ORDER, 2019.")

ORDER, 2019.")

ORDER,")

AMENDMENT RULES, 2014. AMENDED BY MCA NOTIFICATION NO. 42(E) DATED")

Every company, other")

RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th")

RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th")

RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th")

RULES, 2018 (‘SBO RULES’). FORMS TO BE FILLED Form BEN-1")

RULES, 2018 (‘SBO RULES’). FORMS TO BE FILLED Form BEN-3")

CSR: Section 135(1) has")

SECOND AMENDMENT RULES, 2018 MCA NOTIFIES AND SUBSTITUTED")

ORDINANCE, 2019 Section 2(41) read with Rule 40 of Companies (Incorporation) (Fourth")

ORDINANCE, 2019 NEW SECTION 10 A FOR COMMENCEMENT OF BUSINESS INC 22")

ORDINANCE, 2019 SECTION 12 REGISTERED OFFICE OF COMPANY If the Registrar has")

Ordinance, 2019 SECTION 14 READ WITH RULE 41 CONVERSION OF PUBLIC COMPANY")

ORDINANCE, 2019 SECTION 77 - DUTY TO FILE FORM CHG-1 FOR CREATION/MOFDIFICATION")

ORDINANCE, 2019 REVISION IN FORM CHG-4 For Satisfaction of Charge Filing Dealayed")

- Slides: 32

Companies Act, 2013 An Insight into Latest Amendments Presented By: CS (Dr. ) D. K. Jain Practising Company Secretary &

COMPULSORY REQUIREMENT FOR DEMATERIALISATION OF SECURITIES Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2018 (By Notification No. . GSR 853(E) dated 10 th Sept. , 2018 New Rule 9 A has been inserted, which requires that; 1. Every unlisted public company (except, WOS, Nidhi and Govt. Company) shall – (a) issue the securities only in dematerialized form; (b) facilitate Dematerialization of all its existing securities 2. Dematerialization is a pre-requisite condition to making any offer for issue of any securities; or buyback; or issue of bonus or rights offer, transfer or subscription of securities after 2 nd Oct. , 2018. Comments: Public company includes subsidiary of public company

COMPULSORY REQUIREMENT FOR DEMATERIALISATION OF SECURITIES 4. Other requirements: (a) Appointment of RTA, Execution of Triparty Agreement with DP, RTA and Company, and obtaining ISIN for each type of securities (b) Payment of security Deposit to RTA and DP for two years in advance (c) Filing of the Security Audit Report u/s 55 A of the Depository Rules on half yearly basis within 30 days of the end by PCS to Ro. C (Form not Prescribed) (Before 30. 04. 2019 and onwards) (d) In case of default in payment (deposit/fee) of the custodian fee and RTA fee, company shall not be eligible for Bonus and Right issue. (e) In case of any grievance the complaint can be made to IEPF

COMPULSORY REQUIREMENT FOR DEMATERIALISATION OF SECURITIES 5. Obligations: On Company to have connectivity for D-mat, but security holders are not bound to D-mat their holding until; (a) Do not wish to transfer the securities; (b) Do not wish to participate in rights, private placement, buy back, and bonus. (c) Fine: No fine prescribed for non compliances, however u/s 450 upto Rs. 1, 000/- per day. (d) It is likely that in the Form MGT-7, the new details for the ISIN/RTA may be added for review of compliance by the Ro. C (e) Entire promoters, directors and KMPs securities must be in D-mat Form before taking any corporate action 6. Recommendation: (a) To obtain ISIN; or (b) To Convert into Private Company; or (c) Get status of WOS

SPECIFIED COMPANIES (FURNISHING OF INFORMATION ABOUT PAYMENT TO MICRO AND SMALL ENTERPRISE) ORDER, 2019. MCA NOTIFICATION NO. GSR 368(E) DATED 22. 01. 2019 READ WITH THE NOTIFICATION SO 5622(E) DATED 2 ND NOV. , 2018 Meaning of Specified Company: All companies, who get supplies of goods or services from micro and small enterprises and whose non payments to them exceed forty five days from the date of acceptance or the date of deemed acceptance of the goods or services (as at 22. 01. 2019) as per the provisions of section 9 of the MSMED Act, 2006. Criteria of Micro and Small Enterprises: Section 9 of the MSMED Act, 2006 defines them as per investment In P & M /Equipment's: Type of Enterprise Manufacturing Industry Service Industry Micro Does Not Exceed Rs. 25 Lakhs Does Not Exceed Rs. 10 Lakhs Small Exceeds Rs. 25 Lakhs but does not exceed Exceeds Rs. 10 Lakhs but does Rs. 5 Crore not exceed Rs. 2 Crore Medium Exceeds Rs. 5 Crore but does not exceed Rs. 10 Crore Exceeds Rs. 2 Crore but does not exceed Rs. 5 Crore

SPECIFIED COMPANIES (FURNISHING OF INFORMATION ABOUT PAYMENT TO MICRO AND SMALL ENTERPRISE) ORDER, 2019. Whether Registration of Micro/ Small enterprises is mandatory: No, Section 8(1)(a) provides discretion to get registration, means there is no mandatory requirement for having any such registration certificate, only confirmation of them is sufficient. Requirement to make payment & Interest if any Section 15 provides the maximum period of 45 days to make payment irrespective of the agreed period exceeding 45 days. Section 16 make obligations to pay monthly compounding interest for delayed period @ 3 times of the Bank Rates of the RBI. Requirement for reporting to the Ro. C in Form MSME-1 Required u/s 405 of the CA for providing information of statics - 1 st Time position of out standing as at 22. 01. 2019 (within 30 days, i. e. on or before 20. 02. 2019) - Half yearly on 31 st March and 30 th Sept. , within 30 days of the end of period - The form needs to be signed by the director/ cs of the Company, No certification of professional.

SPECIFIED COMPANIES (FURNISHING OF INFORMATION ABOUT PAYMENT TO MICRO AND SMALL ENTERPRISE) ORDER, 2019. Difficulties: 1. Finalizations of the list of creditors exceeding 45 days before Audit 2. Obtaining details of the Micro and Small enterprises 3. Providing interest for the default period in the books. 4. Ro. C may ask further details and inspect u/s 405(3) 5. No. of multiple transactions with the same entity, disputes in quality/ quantity, running work. Mis-use of information: for IBC or otherwise by Micro/ Small enterprises Fine: On company upto 25, 000 and on Directors Rs. 25, 000 to Rs. 3, 000 or imprisonment upto 6 months or both (Compoundable)

SPECIFIED COMPANIES (FURNISHING OF INFORMATION ABOUT PAYMENT TO MICRO AND SMALL ENTERPRISE SUPPLIERS) ORDER, 2019. Advisable Steps by Companies ØPrepare list of creditors after verifying and recording all invoices for outstanding more than 45 days from the date of receipt of goods or services from all the creditors as at 22. 01. 2019. ØInterduce KYC system/ vendors registration for the first time contracts/ arrangement ØSend email to all such creditors having credit balance exceeding 45 days as on 22. 01. 2019, requesting them to confirm their status and to provide Copy of the Registration Certificate of MSME (if any) and PAN ØThe above activities should be completed before 18 th Feb. , 2019 positively, so that you may be able to make proper and timely compliance before the last date on or before 20 th Feb. , 2019. ØIf possible make payment of all such dues before 21. 01. 2019 to avoid providing details. ØMake provisions for interest @ three times of the Bank rate of RBI for the default period if any ØThe similar exercise needs to be repeated for 30 th Sept. , and 31 st March, however, once details of the status once received, need not to take repeated confirmation

COMPANIES (ACCEPTANCE OF DEPOSITS) AMENDMENT RULES, 2014. AMENDED BY MCA NOTIFICATION NO. 42(E) DATED 22. 01. 2019 • In the Rule 2(1)(c)(xviii) in the exempted category of deposits “any amount received by a company from Alternate Investment Funds, Domestic Venture Funds, Infrastructure Investment Trusts, (Real Estate Investment Trusts) and Mutual Funds registered with SEBI in accordance with regulations made by it. ” has been inserted. • In Rule 16 which provides that every company to which deposits rules apply, shall on or before the 30 th day of June, of every year, file with the Ro. C, a return in Form DPT-3 and furnish the information contained therein as on the 31 st day of March of that year duly audited by the auditor of the company. In the said rule the following explanation has been inserted: “It is hereby clarified that Form DPT-3 shall be used for filing return of deposit or particulars of transaction not considered as deposit or both by every company other than Government company”

AMENDMENT IN RULE 16 A DISCLOSURES IN THE FINANCIAL STATEMENT. (1) Every company, other than a private company, shall disclose in its financial statement, by way of notes, about the money received from the director. (2) Every private company shall disclose in its financial statement, by way of notes, about the money received from the directors, or relatives of directors. (3) Every company other than Govt. company shall file a onetime return of outstanding receipt of money or loan by a company but not considered as deposits, in terms of clause (c) of sub-rule 1 of rule 2 from the 1 st April, 2014 to the date of publication of this notification in Form DPT-3 within Ninety days along with fee Revised Form DPT-3 is inserted (Not available for e-filing till now) • Form has 3 options • (o) One Time Return for disclosure of details of outstanding money or loan received by company but not considered as deposits u/r 2(1)(c) • (o) Return of Deposit or Return for Disclosures of money or loan received by the company but not considered as deposits u/s 2(1)(c) of the Rules • (o) Return or Deposit

AMENDMENT IN RULE 16 A DISCLOSURES IN THE FINANCIAL STATEMENT. Therefore, • For each types of return a separate form DPT-3 would required to be filed • Every company except Govt. , Company needs to file the form • One time return needs to be filed for status as at 22. 01. 2019 within 90 days on or before, 21 st April, 2019 • The particulars from 1 st April, 2014 to 31 st March, 2018 also needs to be filed on or before 21 st April, 2019 • Thereafter it is assumed that the amount not considered as deposits may be required to be filed on each years as at 31 st March, on or before 30 th June. • List of Deposits and Auditors Certificate is required to be attached with the Form DPT -3, however no requirement for certification of the Form by Professionals • All the exempted items needs to be reported in the Form

EXEMPTIONS TO PRIVATE COMPANIES FOR AMOUNT/DEPOSITS OBTAINED FROM DIRECTORS AND THEIR RELATIVES & MEMBERS • Amount received from the Directors and their relatives are fully exempted subject to compliances of: (a) At the time of receipt of the amount he must be a director in the Board (b) Disclosure in the Annual Report for the amount received from the Directors (c) Disclosure in the Annual Report for the amount received from the relatives Directors (d) Have furnished a declaration in writing at the time of providing money that the amount is not given out of the funds acquired by him by borrowings or accepting loans or deposits from others • Amount received from the members (Shareholders are exempted subject to compliances of; (a) Which accept money from members not exceeding hundrend percent of paid up share capital, free reserves and Security Premium; or (b) Which is start up (Registered) for 5 years; or (c) Which fulfills all the following three conditions (i) Which is not an associate or subsidiary of other company; and (ii) If the borrowing from Banks /FIs or Company less than twice of paid up capital or Rs. 50 Crores which even is lower; and (iii) Not defaulted in repayment of such borrowings (ii) above at the time of accepting deposits

EXEMPTIONS TO PRIVATE COMPANIES FOR AMOUNT/DEPOSITS OBTAINED FROM DIRECTORS AND THEIR RELATIVES & MEMBERS • Amount received from the members (Shareholders are exempted subject to compliances of; - Filing of Form DPT-3 to Ro. C Particulars Exempted Pvt. Ltd. Co. Other than exempted Pvt. Co. Restriction on amount of deposits Interest Maximum as per RBI Rate Upto 35% of PC + FR Maximum as per RBI Rate Deposit into Liquid Asses Period Filing of Form DPT-3 Register of Deposits Special Resolution 6/36 months Yes Yes 20% of out standing Balance 6/36 months Yes Yes

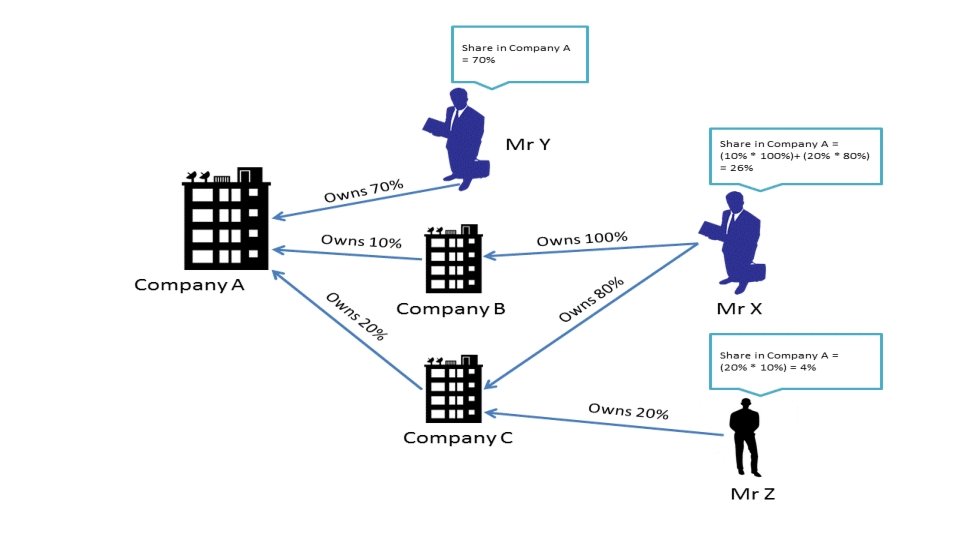

COMPANIES (SIGNIFICANT BENEFICIAL OWNERS) RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th June, 2018 (Anended on 08. 02. 2019 Rule 2(1)(h) Meaning Significant Beneficial Ownership In relation to reporting company means an individual referred to in section 90(1) (holding ultimate beneficial interest of not less than 10%) who acting alone or together with one or more persons or trust, posses one or more of the right or entitlement in reporting company namely; (a) Holds directly or indirectly not less than 10% of the shares; (b) Holds directly or indirectly not less than 10% of the voting rights; (c) Right to receive and participant directly or indirectly in dividend of not less than 10% in a financial year; (d) Has right to exercise or actually exercises significant influence or control in any manner other than through direct holding,

COMPANIES (SIGNIFICANT BENEFICIAL OWNERS) RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th June, 2018 Calculation of Significant Beneficial Ownership (1) Holding of shares in the name of Individual; and (2) Beneficial ownership in the shares not registered in his name (u/s 89(2) (3) Hold majority stake in the member company of Reporting Company; or (4) Holds majority stake in the holding company of that member; (5) Karta- Where the member is HUF of the reporting company; (6) Partner- Where the member is a partnership / LLP (7) Trustee or beneficiary or author - Where the member is discretionary or charitable trust; (8) Is a general partner or is an investment manager or CEO of Entity controlled pooled investment vehicle

COMPANIES (SIGNIFICANT BENEFICIAL OWNERS) RULES, 2018 (‘SBO RULES’). MCA vide notification dated 13 th June, 2018 Meaning of shares – Explanation VI Shares includes: 1. GDR, 2. Compulsorily Convertible Preference shares 3. Compulsorily convertible Debentures Meaning of Significant Influence (Section 2(1)(i); includes power to participate (directly or indirectly) in Financial and operating policy decision but not control of those policy

COMPANIES (SIGNIFICANT BENEFICIAL OWNERSHIP) RULES, 2018 (‘SBO RULES’). FORMS TO BE FILLED Form BEN-1 (Physical) Significant Beneficial [Declaration] On Owner shall file to the commencement of the Reporting company Rules or any time where holding occurs more than 10% thereafter REMARKS Within 90 days from commencement of these Rules - First time on or before 9 th May, 2019) According to Notification dated 08. 02. 2019 Form No. BEN-1 has been revised and needs to be submitted physically to the reporting company Form BEN-1 SBO shall file to the Within 30 days in case of [Declaration] In case of company change in his SBO any change Form BEN-2 (E-Form) Company to file with the by Company Registrar online Within a period of 30 days Advantage of 90+30 days from the date of receipt of time cannot be taken. Declaration with filing fee Form needs Certification Declaration needs on stamp paper

COMPANIES (SIGNIFICANT BENEFICIAL OWNERSHIP) RULES, 2018 (‘SBO RULES’). FORMS TO BE FILLED Form BEN-3 By the Company (Physical) Register of SBO REMARKS No time limit is Register is available for Inspection prescribed, then should be by the members updated simultaneously the filing of Form BEN-2 Form BEN-4 By Company to the 30 days time is specified [Physical] for notice person who is u/s 90(6) to give for disclosure presumed to have SBO declaration if any ownership within 3 years In case of failure the Company shall apply to NCLT within 15 days of expiry of notice period for (a) Restrictions of Transfer (b) Suspension of rights of dividend and voting rights (c) Other restrictions Fine: Defaults are separately for; (1) Non filing Form BEN-2 (2) Non maintain register (3) Fails to deny inspection On SBO: Not less than Rs. 1 Lakh but may extend to Rs. 10 Lakhs further fine of Rs. 1000/- for per day of On Company and every officer: Not less than Rs. 10 Lakh but may extend to Rs. 50 Lakhs further fine of Rs. 1000/- for per day

OTHER IMPORTANT CHANGES IN THE COMPANIES ACT NEEDS TO BE CONSIDERED • Section 139: Appointment/ Re-appointment of Auditors: No requirement for ratification of the Auditors at every AGM • Section 185: Loan to directors : Can be given to a company in which director is a director or member subject to the previous approval of members by SR • Section 196/197: No need for approval of Managerial Remuneration or waiver of the excess remuneration paid by public company: • Section 403: Filing fee of delayed documents @ Rs. 100/- per day on Form MGT-7 and AOC-4 (For previous year upto 1 st July, 2018 the Normal + Additional and Rs. 100/- per day for the period till the actual date of filing will be liable to be paid • KYC of the Director after 1 st April- but before 30 th April by filing of the Form DIR-3 KYC

OTHER IMPORTANT CHANGES NEEDS TO BE CONSIDERED • Section 135(1) CSR: Section 135(1) has been amended by inserting “[the immediately preceding financial year] for "any financial year" by Companies (Amendment) Act, 2017, w. e. f. 19 -9 -2018, vide Notification No. SO 4907(E), dated 19 -9 -2018 for requirements for constitution of the CSR Committee. Whereas section 135(5) provides that the Board of every company referred to in sub-section (1), shall ensure that the company spends, in every financial year, at least two per cent. of the average net profits of the company made during the three immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy: Provided that the company shall give preference to the local area and areas around it where it operates, for spending the amount earmarked for Corporate Social Responsibility activities: Provided further that if the company fails to spend such amount, the Board shall, in its report made under clause (o) of sub-section (3) of section 134, specify the reasons for not spending the amount. [Explanation. —For the purposes of this section "net profit" shall not include such sums as may be

COMPANIES (PROSPECTUS AND ALLOTMENT OF SECURITIES) SECOND AMENDMENT RULES, 2018 MCA NOTIFIES AND SUBSTITUTED EXISTING RULE 14 RELATED TO PRIVATE PLACEMENT OF COMPANIES (PROSPECTUS AND ALLOTMENT OF SECURITIES) RULES, 2014 VIDE NOTIFICATION DATED 7 TH AUGUST, 2018 • Utilisation of funds: The most significant change is that an issuer is not permitted to utilise any monies raised through private placement till the allotment is complete and (PAS 3) is filed with the ROC within 15 days of allotment. The timelines for filing the return on allotment has been reduced to 15 days unlike the erstwhile provision of 30 days. • Relaxation in filing of PAS-4 and PAS-5 with ROC: Offer Letter in Form PAS-4 and record of persons to whom the Offer Letter is issued in Form PAS-5 were required to be maintained by the Company and are no longer required to be filed with the ROC. • Resolutions to be filed prior to issue of Offer Letter: Prior to issuing the Offer Letter, the SR approving issuance of securities and/or BMR for issue of securities has to be filed with the ROC. In this regard, it has also been clarified that private companies (which were earlier exempted from filing of BMR) will have to file BMR passed for issue of securities. • There is change in format of Form PAS-4

COMPANY (AMENDMENT) ORDINANCE, 2019 Section 2(41) read with Rule 40 of Companies (Incorporation) (Fourth Amendment) Rules, 2018: (W. e. f. 02. 11. 2018 ) Rules Notified on 18. 12. 2018) 1. “Financial year”, in general Financial year means the period ending on the 31 st day of March every year and where it has been incorporated on or after the 1 st day of January of a year, the period ending on the 31 st day of March of the following year. 2. Existing proviso has been substituted as; Provided that where a company or body corporate, which is a holding company or a subsidiary or Associate of a company incorporated outside India and is required to follow a different financial year for consolidation of its accounts outside India, the Central Government may, on an application made to Regional Director in Form RD-1, allow any period as its financial year, whether or not that period is a year; 3. All the applications pending before the Tribunal on the date 02. 11. 2018 shall be disposed by Tribunal in accordance with the previous rules

COMPANY (AMENDMENT) ORDINANCE, 2019 NEW SECTION 10 A FOR COMMENCEMENT OF BUSINESS INC 22 A to be filed

COMPANY (AMENDMENT) ORDINANCE, 2019 SECTION 12 REGISTERED OFFICE OF COMPANY If the Registrar has reasonable cause to believe that the company is not carrying on any business or operations, he may cause a physical verification of the registered office of the company and if any default is found he may initiate action for the removal of the name of the company by ROC

COMPANY (Amendment) Ordinance, 2019 SECTION 14 READ WITH RULE 41 CONVERSION OF PUBLIC COMPANY INTO PRIVATE COMPANY. Any application pending before Tribunal shall be disposed off by it in accordance with the provisions applicable to it before such commencement. - Now Application needs to be made within 60 days of SR to the RD with fee as per CG Rules along with; - Declaration of two directors for No. of members and Deposits, - Declaration by KMP/Director for compliance of sec. 73 -76 A, 177, 178, 179(3)185, 186, 188 - List of Creditors, Debenture holders not older than 30 days of filing application to RD - Publication of Advertisement in Form 25 A at least 21 days before application - Service of notice by Regd. Post to creditors, debenture holders, Ro. C and regulating authority if any. - RD may ask further information (upto 2 resubmission) in the Form RD-GNL 5 within 15 days - RD shall approve the application within 30 days of submission of all information, he may call hearing in person

COMPANY (AMENDMENT) ORDINANCE, 2019 SECTION 77 - DUTY TO FILE FORM CHG-1 FOR CREATION/MOFDIFICATION OF CHARGES For Creation / Modification of Charge Filing within days Delayed filing Further application Fee payable Form CHG-1 for charge created after 02. 11. 2018 30 - - Normal filing fee 31 -60 Upto 30 - Normal+ Additional fee as may be prescribed 61+ 120 date of filing As the case may be As above From to the RD/Central Govt Normal+ Ad volarem fee Filing of Form INC-28 - Normal+ additional fee up to 12 times Further 6 months provided without applying for condonation of delay 120 days + For Charges created before 02. 11. 2018 30 270 300+ actual date As the case As may be ordered Form CHG-8 As may be ordered

COMPANY (AMENDMENT) ORDINANCE, 2019 REVISION IN FORM CHG-4 For Satisfaction of Charge Filing Dealayed filing Further within days application Fee payable Form CHG-4 for charge created after 02. 11. 2018 30 - Normal filing fee 31 -300 As the case may be Normal+ Additional fee as may be prescribed 300+ As the case may From to the be Central Govt As may be ordered 30 Upto 30 Normal+ additional fee without applying for condonation of delay 60+ actual date of filing As the case may Form CHG-8 to be RD For satisfied before 02. 11. 2018 - - As may be ordered Filing of Form INC-28

NATIONAL FINANCIAL REPORTING AUTHORITY RULES, 2018 MCA notification dated 13 TH NOV. , 2018 Key aspects specified by the NFRA rules are Classes of companies and bodies corporate governed by the NFRA Authority, Functions and duties of the NFRA Authority, Annual return, Recommending accounting standards and auditing standards, Monitoring and enforcing compliance with accounting standards and auditing standards, Overseeing the quality of Audit service and suggesting measures for improvement, Power to investigate, . Disciplinary proceedings, Punishment in case of non-compliance etc. Classes of Companies and Body corporate governed by the Authority – a. Listed Companies in or outside India b. Public Companies having paid-up of not less than Rs. 500 Cr. or annual turnover not less than Rs. 1000 Cr. or having an aggregate outstanding loans, debentures and deposits of not less than Rs. 500 Cr. as on the 31 st March of immediately preceding financial year; c. insurance companies, banking companies, companies engaged in the generation or supply of electricity, companies governed by any special Act; d. any body corporate or company or person, or any class of bodies corporate or companies or persons, on a reference made to the Authority by the Central Government in public interest; and

CLASSES OF COMPANIES AND BODY CORPORATE GOVERNED BY THE AUTHORITY e. a body corporate incorporated or registered outside India, which is a subsidiary or associate company of any company or body corporate incorporated or registered in India as referred to in clauses (a) to (d), if the income or net worth of such subsidiary or associate company exceeds twenty per cent. of the consolidated income or consolidated net worth of such company or the body corporate, as the case may be, referred to in clauses (a) to (d). 2. Every existing body corporate other than a company governed by these rules, shall inform Authority within 30 days of commencement of these rules, in Form NFRA-1, the particulars of the auditor as on the date of commencement of these rules 3. Every body corporate, other than a company defined in clause (20) of section 2, formed in India and governed under this rule shall, within 15 days of appointment of an auditor under section 139(1), inform the Authority in Form NFRA-1, the particulars of the auditor appointed by such body corporate. Provided that a body corporate governed under clause (e) of sub-rule (1) shall provide details of appointment of its auditor in Form NFRA-1 4. A company or a body corporate other than a company governed by these rules shall continue to be governed by Authority for period of 3 years even if its limit fall below.

MAJOR AMENDMENT IN THE HEADINGS OF THE SCHEDULE III, BALANCE SHEET Sr. Previous Format No. Revised Format 1. In Current Liabilities “Trade Payables” Further Classification of Trade Payables: (i) Total outstanding dues of micro enterprises and small enterprises (ii) Total outstanding dues creditors other than micro enterprises and small enterprises 2. In Non-Current Assets (1) (a) Fixed Assets In Non-Current Assets (1) (2) Property, Plant and Equipment 3. In Non-Current Assets and Current Assets Trade Receivable and Loan Receivable Further classification of Trade Receivable and Loan Receivable: (i) Considered goods - secured (ii) Considered goods – unsecured (iii) Which have significant increase in credit risk (iv) Credit impaired

THANK YOU