Welcome to Economics Topic 1 Fundamentals of Economics

- Slides: 20

+ Welcome to Economics Topic 1: Fundamentals of Economics

+ Topic Objectives Students will be able to n Explain why scarcity and choice are the basis of economics in every society. n Describe three economic factors of production and the differences b/w physical and human capital. n Explain how scarcity affects the factors of production n Identify why every decision involves basic trade-offs n Explain the concept of opportunity cost. n Describe how people make decisions by thinking at the margin. n Interpret a production possibilities curve.

+ What is Economics? n Economics- the study of how individuals, businesses and governments make choices when faced with a limited supply of resources

+ Scarcity and it’s impact on economics n Scarcity forces us to make choices, we cannot have everything n Needs n Wants

+ Businesses have goods and services n There is no way to solve the scarcity problem n Businesses provide either goods or services

+ Entrepreneurs Impact on Economics n Entrepreneurs are people who decide how to combine resources to create new goods and services n Entrepreneurs have different tasks: n Factors of production- resources needed/used to make all goods and services n Land n Labor n Capital n Physical capital n Human capital

+ Section 2: Opportunity Cost and Trade-Offs

+ What is an Opportunity Cost? n Opportunity Cost- the most desirable alternative somebody gives up as the result of a decision n Example: Going to Sports Night practice or going to a teacher’s extra help- which would be the best decision for you?

+ What is a trade-off? n A trade off is the act of giving up on one benefit to gain another, greater benefit n Usually involve things that can be easily measured, such as money, property, or time n Can also include things that cannot be easily measured n Can be applied to individuals and businesses n Guns or butter- describes one of the common choices facing government: the choice between spending money on military or domestic needs

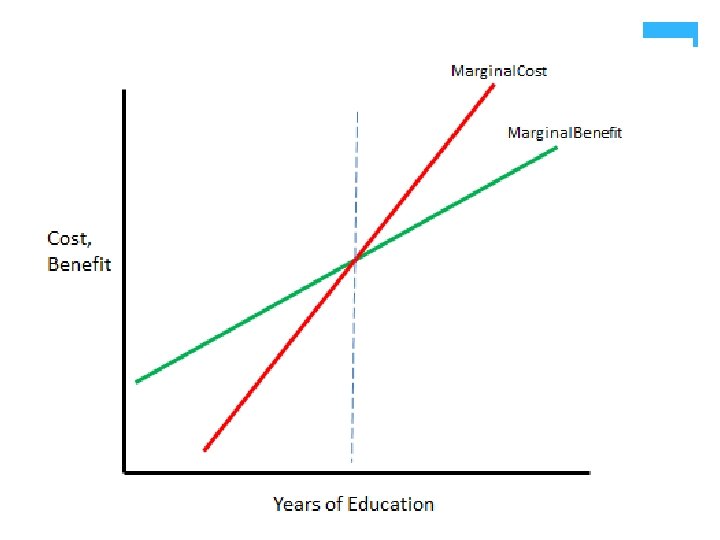

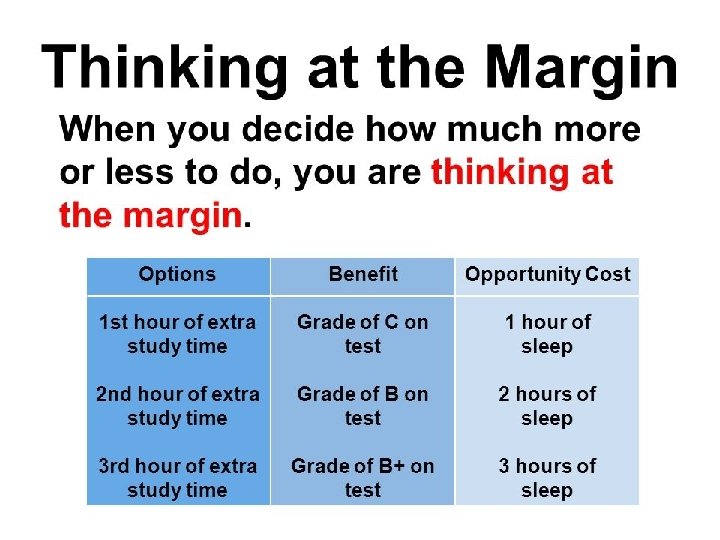

+ Thinking at the Margin n Thinking at the margin: the process of deciding how much more or less to do n People have to decide the opportunity costs and benefits n Thinking at the margin applies to not only businesses but also to individuals and government n Example: Legislatures think at the margin when deciding how much to increase spending on a government program n Decision makers have to compare the opportunity costs and benefits: what will sacrifice and what will gain n Decision making process is sometimes called cost/benefit analysis

+ Cost/benefit analysis n Cost/benefit analysis is the examination of what will be sacrificed and what will be gained n A decision making process in which you compare what you will sacrifice and gain by a specific action. n Marginal cost- the extra cost of adding one unit n Marginal benefit- the extra benefit of adding the same unit n **As long as the marginal benefit exceed the marginal cost, it pays to add more units

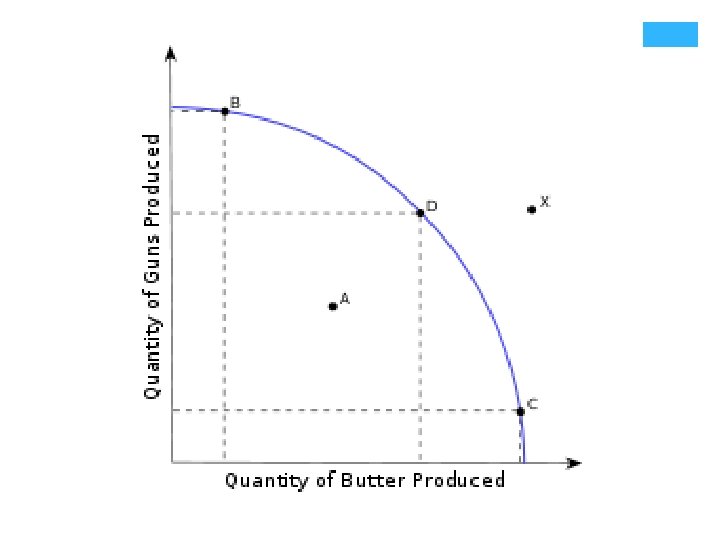

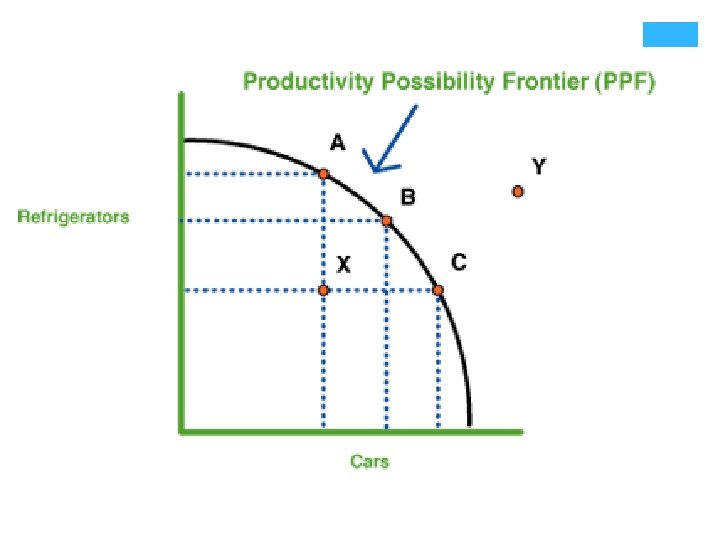

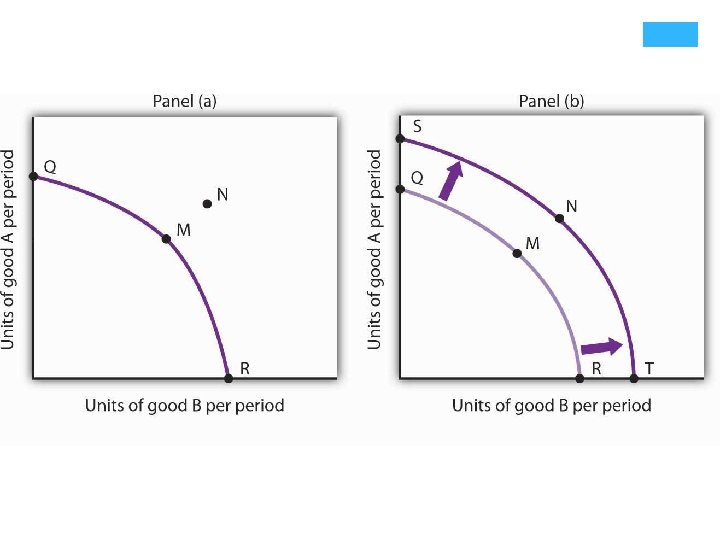

+ Section 3: The Production Possibilities Curve n The Production Possibilities Curve is used to decide what and how much to produce n It is a graph that shows alternative ways to use an economy’s productive resources n The graph can show effective an economy is, whether an economy is growing and the opportunity cost of producing more of one good or service

+ Production Possibilities Frontier n Production Possibilities Frontier is a line in the production possibilities curve that combines the production of two different products n Each point on the production possibilities curve frontier reflects a trade-off n These trade-offs are necessary because factors of production are scarce n Using land, labor, and capital to make one product means that fewer resources are left to make something else n Any point inside of the production possibilities frontier indicates underutilization n Underutilization- use of fewer resources than the economy is capable of using

+ Efficiency n Efficiency- the use of resources in such a way as to maximize the output of goods and services n Rise in a factor of production increases the maximum amount of goods the nation can produce n When the economy grows, economists say that the production possibilities frontier has “shifted to the right” n Law of increasing costs- principle that states that as production shifts from making one item to another, more and more resources are necessary to increase production of the second item n Opportunity cost increases

+ Enduring Understandings n Economics is the study of how people seek to satisfy their needs and wants by making choices among scarce resources. n Every economic decision involves trade-offs; the most desirable choice given up is the opportunity cost. n Production possibilities curves show efficiently an economy uses its resources.