48 Fundamentals wc 261118 Domestic Sentiment Monday Events

- Slides: 6

48 Fundamentals w/c 26/11/18 Domestic Sentiment Monday Events Risk On Themes Tuesday Wednesday Thursday Friday Trump aggressive with China prior to G 20 US China rhetoric continues - increase in sanctions scheduled Trump cancels Putin mtg G 20 On On Neutral Prelim GDP; Powell - dovish “rates just below neutral”; Trumps says Fed bigger problem than China Core PCE; FOMC Mtg Mins - emphasising data dependency and a few members alluding to risk of slowing the economy too much Equities, oil, GBP USD Strong Interest rate hiking, Mueller, trade wars EUR Strong? ? Italian budget concerns JPY Swing GBP Strong CAD Comm AUD Comm NZD Comm Equities Strong Gold Swing Oil Crazy Hope of Italian Budget breakthrough; Draghi Sanctions (Excessive Deficit Procedure) on Italy to begin before Xmas Tokyo Core CPI Ongoing Brexit uncertainty EU Approves Withdrawal Bill; Carney Trump weighs in on Brexit; PM May apparently to allow changes to Withdrawal Bill by Parliament Retail Sales Financial Stability Report Saudi reported to be considering “clandestine” oil production cut API Inventories +3. 45 m vs exp +0. 8 m. Financial Stability Report all Brexit scenarios worse for GDP than staying in EU QE, Tax bill, earnings: all +ve Iran sanctions, GS predicting Brent at USD 80/bbl by end 2018; OPEC+ discussing production hike EIA Inventories +3. 6 m vs exp +0. 6 m

49 Fundamentals w/c 26/11/18 Domestic Sentiment Events Risk Themes Tuesday Wednesday US/China agree 90 day truce as of 1/12 in trade war Trade War “truce” concerns; China’s Mofcom later more bullish and +ve elsewhere; yield inversion; Brexit defeats Canada arrests Huawei’s CFO at US request Off On Fed’s Kaplan concerned about global growth and says US economy may look very different by mid 2019. Fed Chair Powell before the JECC - postponed; National Day of Mourning Thursday Friday Off Mixed Equities; oil; CAD USD Strong Interest rate hiking, Mueller, trade wars EUR Strong? ? Italian budget concerns JPY Swing GBP Strong CAD Comm AUD Comm NZD Comm Equities Strong Gold Swing Oil Monday Crazy Ongoing Brexit uncertainty Manufacturing PMI Bo. E Gov Carney - TSC on Withdrawal Bill; Construction PMI; Gov defeated x 3 in Commons. Services PMI Earnings and NFP PM May being urged to delay next Tuesday’s vote, EU said to offer extension to Article 50 deadline if vote lost. Bo. C Rate and Statement dovish RBA Rate and Statement GDP Retail Sales QE, Tax bill, earnings: all +ve Iran sanctions, GS predicting Brent at USD 80/bbl by end 2018; OPEC+ discussing production cut Qatar pulls out of OPEC; Saudi/Russia agree to extend OPEC+ pact; Canada orders production cut. API Inventories +5. 36 m vs exp -0. 9 m; Oil Ministers giving mixed messages EIA Inventories; -7. 3 m vs exp -1. 3 m; OPEC Meeting - no decision, continue Friday OPEC agree 1. 2 m bpd cut

50 Domestic Sentiment Monday Tuesday Wednesday Thursday Events Gloomy - Japan, US/China, Italy, France, Brexit, Huawai, US data Brexit vote postponed; May heads to Juncker meeting; Macron folds China make trade proposal, start buying soya beans from US. Looks like a confidence vote in PM May US Senate pass 2 nd vote saying Saudi MBS responsible for Khashoggi murder Markets GBPUSD hits 20 month low; slight tech recovery in US equities Intraday gains lost by the close. Good start in Asia for equities. GBP dropping on confidence vote rumours. Off On Fundamentals w/c 10/12/18 Risk Themes USD On then off Friday Off Monday - observing the markets Strong EUR Strong? ? JPY Swing GBP Strong CAD Comm AUD Comm NZD Comm Equities Strong Gold Swing Interest rate hiking, Mueller, trade wars CPI Refinancing Rate: QE ends at end 2018; reinvestment to continue for as long as required; rate on hold to at least end summer 2019. ECB change growth forecast from “risks balanced” to “downside risk”. Italian budget concerns Ongoing Brexit uncertainty Retail Sales GDP Average Earnings Index; (Brexit Vote - postponed) PM May wins no-confidence vote: 200 vs 117 Slew of poor EZ data PM May savaged by E 27 “what do you want? ” Bad China data QE, Tax bill, earnings: all +ve API Inventories:

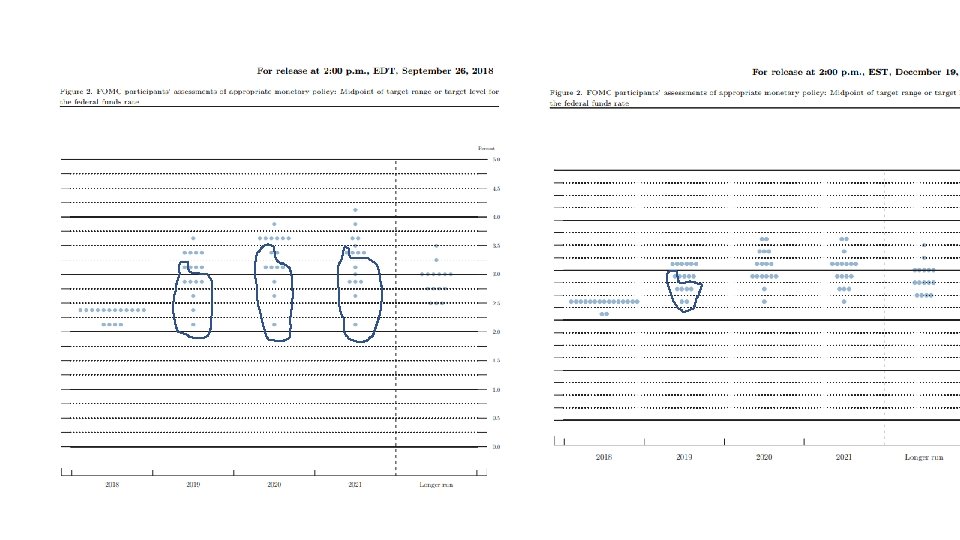

51 Fundamentals w/c 17/12/18 Domestic Sentiment Monday Tuesday Wednesday Thursday Friday Equities rising and USD falling in run up to expected “dovish hike” at Fed mtg today Fed was less dovish than expected, but USD falls and GOLD rises anyway. Equities do not rise, as global slowdown outweighs benefit of fewer rate hikes. Defence Sec Mattis resigns; US shutdown weighing on equities On Off Events Markets Risk Off Themes Off USD (Fed mtg), FX trading; Equities at support; WTI, Gold at resistance USD Strong Interest rate hiking, Mueller, trade wars Fed Funds Rate and Statement, Press Conf - raised rates, forecast fewer and lowered neutral rate (2. 8% vs prior 3. 0%), 2019 slowdown and uncertainty on future rate hikes. EUR Strong? ? Italian budget concerns EU/Italy reach agreement on budget JPY Swing GBP Strong CAD Comm AUD Comm NZD Comm Equities Strong Gold Swing Oil Crazy Core Durable Goods; Final GDP; Core PCE Policy Rate: no drama CPI Ongoing Brexit uncertainty CPI Retail Sales; Super Thursday: no drama Current Account; Final GDP Retail Sales GDP QT, Tax bill, earnings Iran sanctions, GS predicting Brent at USD 80/bbl by end 2018; OPEC+ production cut; concerns about global growth API Inventories: +3. 452 m vs -2. 4 m EIA Inventories: -0. 5 m vs -2. 7 m Concerns of glut, ineffective supply cuts due next month and global slow down.

1 Fundamentals w/c 31/12/18 Domestic Sentiment Monday Tuesday Wednesday Thursday Trump “great jobs numbers”; Kudlow “no recession in sight”; Powell bullish on economy and “listening carefully to markets” Trump says China talks coming along well Events Friday Apple cuts quarterly rev guidance for first time citing weaker Chinese sales; Overnight surge in JPY Markets Off – global growth fears remain Risk Themes Off Improving It’s all about sentiment. USD Strong Interest rate hiking, Mueller, trade wars EUR Strong? ? Italian budget concerns JPY Swing GBP Strong CAD Comm AUD Comm NZD Comm Equities Strong Gold Swing Oil Crazy Average Hourly Earnings; Non-Farm Payroll Holiday Ongoing Brexit uncertainty Manufacturing PMI QT, Tax bill, earnings Iran sanctions, GS predicting Brent at USD 80/bbl by end 2018; OPEC+ production cut; concerns about global growth API Inventories: -4. 5 m vs exp -3. 1 m EIA Inventories: 0. 0 m vs exp -2. 8 m