Youtube https www youtube comwatch vAj RUB c

Youtube • https: //www. youtube. com/watch? v=Aj. RUB c. Aj. Tww&list=PL 109714 D 44 FDEFF 61

Process Costing How to Make Lots of Potato Chips

What Is Process Costing? • A costing system used in situations where large quantities of the same item are manufactured.

Who Uses It • Companies that make large amounts of the same product: • • • Proctor & Gamble - Bounty Lays - Potato Chips Crest - Toothpaste Kellogg's - Corn Flakes Exxon - Gasoline

How to do it • Accumulate the cost of a large number of units produced, and allocate the entire cost over all units produced. Thus, every unit created has exactly the same cost as every other unit produced. Track the costs for the entire production process, and divide by the number of units produced to determine unit costs.

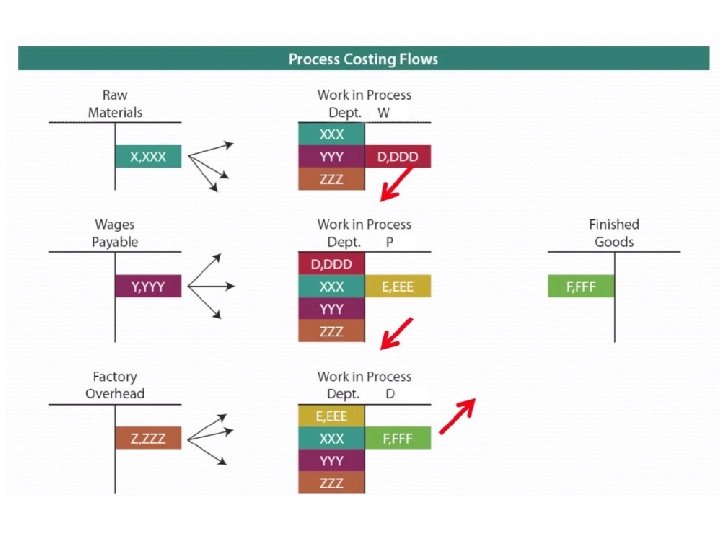

Product goes through various Processing Departments

• Process Costing also gives a way to calculate costs per unit at each stage of the process.

Overview Typical Situation • Direct material costs are added at the beginning of the process. • Other costs (direct labor and overhead) are added over the course of the production process. • In a food processing operation, the direct material (potato) is added at the beginning of the operation. Various rendering operations gradually convert the direct material into finished products (potato chips).

that is in")

Work in Process • That part of a manufacturer's inventory (Asset) that is in the production process and has not yet been completed and transferred to the finished goods inventory. • NB = DR, so adding to Wi. P is a DEBIT • Contains the cost of: – direct material, – direct labor, – factory overhead.

Cutting (potatoes) 1, 000 500, 000 Heating (oil,")

Units of material input Value ($$) Cutting (potatoes) 1, 000 500, 000 Heating (oil, spices) 500, 000 300, 000 Cutting Heating Direct Labor Costs Overhead Costs 200, 000 150, 000

T-Accounts Work in Process Cutting Materials Labor Overhead Inputs to Cutting Units $$ 1, 000 500, 000 ------200, 000 1, 000 900, 000 Outputs to Heating Units $$ 1, 000, 000 900, 000

Work in Process Heating Inputs to Heating Units $$ Output Cutting 1, 000 900, 000 Materials 500, 000 300, 000 Labor ------150, 000 Overhead ------150, 000 1, 500, 000 Outputs to Finished Goods Units $$ 1, 500, 000

Cost per Unit is: $1, 500, 000 = $1 per potato chip.

- Slides: 15