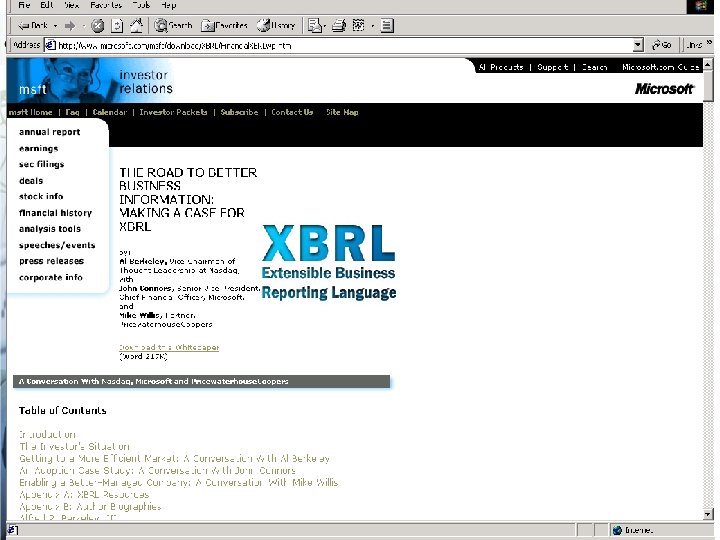

XBRL The Extensible Business Reporting Language Rhode Island

XBRL: The Extensible Business Reporting Language Rhode Island Society of CPA’s 13 -May-2002 Dr. Saeed Roohani Chairman, Accounting Department Bryant College Neal J. Hannon XBRL International Education Work Group Chair XBRL Educational Resource Center at Bryant College sroohani@bryant. edu nhannon@bryant. edu

Agenda • • • XBRL Update – who talks about it XML XBRL General Ledger Government XBRL Reporting The Future of Digital Reporting

XBRL UPDATE • FDIC to run pilot program for Call Sheets – Proof of concept is complete – RFQ in second quarter of 2002 – Pilot program for 2003 • APRA: XBRL in use for all required filings in banking and insurance industry in Australia • Microsoft and Reuters publish in XBRL

XBRL Update • • The Bank of America/ Moody’s Connection Dressner and Deutsche Bank GE Financial (consolidations) Inland Revenue • 260 people attended Berlin, Germany conference • Over 50 Japanese companies members of XBRLJapan • Total consortium membership projected to exceed 200 by 2003

")

XBRL – The Organization – History • Founded by the AICPA in 1998 (13) • Spin Out into International Organization in 2002 (>140) – Organizational Matters • Structure of XBRL • Liaison work • Next International Meeting in Toronto June 17 – 21, 2002 – Jurisdictional Growth • Active: Australia, Canada, Germany, IASB, Japan, UK, US, Singapore • Development: Belgium, Hong Kong, India, Ireland, Netherlands, New Zealand, South Africa, Spain, Sweden, Taiwan

Finance/Audit Committee International Steering Committee Chair At Large")

Executive Committee Board of Directors (Trustees) Finance/Audit Committee International Steering Committee Chair At Large ISC Members 1 st 3 rd 2 nd Nominating Committee 4 th Web site Committee XBRL Management CEO Jurisdictions 1 st Vice Chair Sitting Members AU IASB* JP SG US Liaison 2 nd VC Preparer, Private Sector Accounting Intermediaries Software & Services Mktg & Comm Provisional Spain Netherlands …Hong Kong… * Standing Specification Developers CA DE UK Members International Working Groups Supply Chain Participants Investors/Creditors Education Analyst Research Regulators Grants General Ledger Academic Public Sector Preparers

Finance/Audit Committee")

XBRL International Governance & Operational Structure Executive Committee Board of Directors (Trustees) Finance/Audit Committee Chair - Ramin International Steering Committee Chair - Hamscher At Large ISC Members Coffin Hamscher OPEN XBRL Management CEO (Acting) – Louis Matherne Jurisdictions 1 st Vice Chair – Kurt Ramin Sitting Members AU -Hardidge Specification - Hampton Developers - OPEN CA Cuthbertson Liaison – Coffin (Acting) DE Fuhrmann IASB* - Ramin JP Watanabe SG - Tang UK - Rodgers Members International Working Groups Nominating Committee Chair - Cuthbertson Web site Committee Chair - Watson Supply Chain 2 nd VC – Schnitzer Participants Preparer, Private Sector - OPEN Accounting - Willis Intermediaries - Watson Software & Services - Blake Mktg & Comm. - Colgren Investors/Creditors - Flickinger Provisional Education - Hannon US - Matherne Spain Analyst - Schnitzer Research - Srivastava Regulators - Walenga * Standing Netherlands Grants - Watson Hong Kong GL - Cohen Academic - OPEN Public Sector Preparers - OPEN

XBRL – Taxonomies • • • IASB Commercial & Industrial for AU, NZ, SG, UK, HK, Japan Statutory Accounts Germany Statutory Accounts International General Ledger U. S. Commercial & Industrial U. S. Investment Management U. S. Federal Government General Ledger (KPMG developed) U. S. Non-Profit Form 990 Other specific sector based taxonomies under development.

XBRL Support “I would like to see you develop valuation models that result in consistent, comparable and fair values of assets and liabilities. I would like to see you hone specific, but plain English definitions for the types of information you believe should be included in public disclosure. I would like to see you take your XBRL project a step further, providing account classifications for companies in common industries. In short, I challenge you to turn all of this data into meaningful information for investors. ” - Arthur Levitt, Chairman, U. S. Securities & Exchange Commission October 24, 2000, at the Fall Council of the AICPA (Las Vegas, Nevada)

Microsoft CFO on XBRL • "Through Internet delivery, XBRL will also provide analysts and investors with extensible financial data to make informed decisions about the company. We see XBRL as not only the future standard for publishing, delivery and use of financial information over the Web, but also as a logical business choice. " John Connors, Chief Financial Officer, Microsoft

The Capital Markets • “NASDAQ joins shoulder to shoulder in the effort of the XBRL Consortium to adopt this new, freely available technology because it feels that improving the distribution and analysis of corporate results, especially for the 10, 000 companies not covered by Wall Street analysts will broaden the market for NASDAQ’s own trading services” Michael Sanderson, CEO NASDAQ Europe

Transparency in Financial Reporting • “Reuters’ reputation stands on its ability to communicate and the extensible business reporting language standard it has employed this week to publish accounts online is amongst the most significant of developments in promoting transparency in financial information” Accountancy Age, 1 November 2001

Message to Congress on Post Enron Environment • “One large scale and potentially revolutionary private sector initiative that already is underway is a collaboration of growing companies, accounting firms and the AICPA to develop a common “tagging” system for various financial accounts, which goes under the acronym “XBRL”. … I would urge the SEC (and if necessary, urge the Committee to urge the SEC) to encourage this project… One possibility: require EDGAR submissions to be in XBRL by a specific date. ” • Bob Litan, Brookings Institution & Bear Stearns testimony to U. S. Senate Banking Committee on post-Enron, March 14, 2002

Implementations/Vendors • APRA • FDIC • UK Inland § Revenue • GRE – Credit§ § & RM § • General § Electric Morgan Stanley Reuters Microsoft Edgar-On. Line Moody’s § Edgarscan § ACCPAC § Caseware § Creative Solutions § Enumerate § FRSolutions § MSFT/Great Plains/Navision § Fujitsu § Hitachi § Hyperion § KPMG Columbus § Moody’s § New. Tec § SAP § Semansys § Software AG § UBMatrix

XBRL is: –NOT a new accounting standards but enhances the distribution and usability of existing financial statement information

• ……is a meta markup language the World Wide")

e. Xtensible Markup Language (XML) • ……is a meta markup language the World Wide Web Consortium (W 3 C) considers a universal standard for describing both structured data and the behavior of applications that process the language.

XML is Platform Independent Self-Describing • • • Example: Windows Unix Macintosh Mainframe Linux – <DATE>July 26, 1998</DATE> • Describes the information, not the presentation • Format neutral

XML Simplified DATA 1, 000 Context XML Net income: Company Currency Period Rounding Roll-up XBRL

XML Markup: What Does it Look Like? Michael M. Miller 8080 Hill Circle Lincoln, MA 01738 +1 (617) 515 -1424 Birthdate: 19 October 58 <name>Michael M. Miller</name> <address> <street>8080 Hill Circle</street> <city>Lincoln</city> <state>Massachusetts</state> <country>United States of America </country> <postcode>01738</postcode> Ordinary information </address> <telephone>6175151424</telephone> <birthdate>19/10/1958</birthdate> Metadata: Information about information

<cash> Chemical Industry <SYMBOL> Human Resources (HRML) Music Industry")

Industry Taxonomy Development Financial (XBRL) <cash> Chemical Industry <SYMBOL> Human Resources (HRML) Music Industry Aerospace Astronomy <resume> <RECORD-LABEL> <PROGRAM> <PLANET>

Who’s Building Taxonomies?

Structured Content allows Data reuse, comparability, aggregation Regulatory filings Tax Return Explanatory text Accounting system Other information sources Schemas (Standard Definitions) Document Bank filings (Data with Metadata) Website Printed Financials

Structured Content allows Data reuse, comparability, aggregation Regulatory filings Explanatory text Tax Return Accounting system Other information sources Bank filings XBRL Instance Website Printed Financials XBRL Taxonomies Investor Analytics

XML is Expandable • Whereas – HTML has a fixed set of tags (<H 1>, <B>, <PRE>) aimed at data presentation • XML lets you create your own tags – <sugary-substance> – <Shakespearean-character> – <cash-equivalent> – The key focus is on content, not presentation

The XML Puzzle XML Document Core Schema Transformatio n Tools Industry Specific Vocabularies Company Specific Vocabulary

What is XBRL? • XBRL is a freely available electronic language for financial reporting • XML-Standards based method to : – – Prepare, Reliably Extract, Exchange on a system to system basis Publish company financial data • Potential for extensive use in government accounting

XBRL Builds on XML and SGML XBRL Industry Developed, Supported 2001 W 3 C Supported XML and XML enabling technologies X-Link, X-Schema 1998 ISO Standard SGML Standard Generalized Markup Language 1986

Evolution to Web Services Innovation Program the Web Browse the Web Services Text Files Web Pages FTP, E-Mail, Gopher Automation Presentation Connectivity TCP/IP Technology HTML XML

How XBRL Solves Problems Improves the way companies -- and applications -- share business reporting information 1. Client Specific Data Financial data; multiple systems 3. XBRL information flows freely across the Internet or VPN, LAN and WAN XML/XBRL translator 5. XBRL data is used in the government application and/or other comparable programs FDIC Call Report Common XBRL Vocabulary Client COA to FDIC Taxonomy 2. Application data is selected, cleaned and tagged in XBRL FDIC Taxonomy 4. XBRL-tagged data is mapped into applications specific data such the FDIC’s Call Reports

What software ‘sees’ is the differentiator and drives benefits

Benefits • XBRL is: – NOT a new accounting standards but enhances the distribution and usability of existing financial statement information – Enabler and an extension for native-XML database functionality* for all financial statement information • *Can be stored as a form or a separate financial fact

Raw XBRL <numeric. Context id="rg. cy 00. jpy" cwa="false" precision="4"> Rock Gravel Corp. <entity> Period from 1 Jan 2000 <identifier to 31 Dec 2000, In Yen scheme=“Ticker">rg</identifier> Precise to 4 digits </entity> <period> <start. Date>2000 -01 -01</start. Date> <end. Date>2000 -12 -31</end. Date> </period> <unit> <measure>iso 4217: jpy</measure> </unit> </numeric. Context>

XBRL as a Translator • Accounting is fragmented – Hundreds of accounting software packages – Many correct ways to interpret GAAP and Governmental accounting • XBRL as common denominator – Each set of financial data can conform to a single taxonomy.

Who defines the tags? • Tags are defined by industry consortiums • Each industry’s standard tags are commonly referred to as a taxonomy

XBRL Taxonomies in 2002 • Best practices – e. g. ast. amz. goodwill = Amortization of Goodwill – e. g. Assets have “current” & “non current” children – e. g. Reusable common components taxonomy • Focused development efforts – – – IAS Taxonomy: Core financials, Core + Notes US GAAP C&I Taxonomy UK GAAP C&I Taxonomy Inland Revenue “Computation” Taxonomy FDIC Taxonomy (US) Canadian GAAP, others.

XBRL for General Ledger Developing an international core for reporting general ledger transactions

XBRL. org Specifications XBRL for Financial Statements XBRL for General Ledger Processes Business Operations XBRL for Business Event Reporting Internal Financial Reporting External Financial Reporting XBRL for Audit Schedules XBRL for Tax Filings Trading Partners Investment and Lending Analysis Financial Publishers and Data Aggregators Companies Participants XBRL for EDGAR Filings Management Accountants Auditors Software Vendors Regulators Investors

XBRL- General Ledger Goal • A cross-jurisdictional, cross-industry fact-gatherer for representing the information found in a “General Ledger”, internationally. Bringing “standardization” to Bombastic, Imperative and Clairvoyant, Inc. Initial EEC Payroll Journal Date 9. 1 Account Description 1005 Cash 7, 232. 96 2300 FICA Payable 1, 053. 56 2800 Garnish Payable … Debit Credit 545. 00

Requirements for XBRL GL A Standard Format for: • 3 rd party software to create journal entries to pull into client GL system • To move unposted and posted GL information from divisions to consolidating systems, budgeting , forecasting, reporting tools, and back • To upload general ledger information, payables, receivable files and open balances for system migration or interfacing with Internet ASP

Requirements for XBRL GL Standard Format to move information • From client's systems to CPA • From one CPA system (eg, write-up) to another (eg, tax) in an international context. Standard Format to Represent • Open receivables, open payables, inventory balances, and other asset-based measures for sharing with banks • Detail drill-down for performance measurement reporting items

Requirements for XBRL GL • Extensible for any type of mandatory audit trail • Extensible for meeting any "sub-ledger" need • Designed as XBRL spec-compliant but for easy translation to other uses • Cannot assume that XBRL period, entity, unit and other context (numeric, nonnumeric) will automatically be there.

Accounting: Bridging e. Business and Financial Reporting On e wa y Tax Regulators Investors Creditors Lende Website rs Aggregators XBRL BUSINESS REPORTING ERP 2 way Detail Suppliers G/L Packages CRM XBRL GL Ledger Taxonomy Transaction Creation. Accounting Recognition (e-)Business • Orders • A/P • A/R • Delivery x. 12, EDIFACT, XML INITIATIVES On e wa y Customers 2 -way

XBRL-GL: From Business Transactions to Financial Statements XBRL For Financial Statements XBRL GL Core Recommended status 3/15/02 XBRL GL Custom Unique to each organization Business Transactions Not XBRL; function of other consortiums

“General Ledger” Holds More Valuable Information

Overview of the Structure of the GL Taxonomy Three Primary Levels accounting. Entries GL Journal Batches entry. Header Target and Source Application Creator Organization GL Journal Header entry. Detail Journal Identifiers Entered by Entry Date Posting Date Hash Totals GL Journal Detail Lines Detail Identifiers Line Number Amount Account XBRL Reference

XBRL-GL • Files and more information can be found at: www. xbrl. org/gl/gl. htm

Government XBRL Applications

2001 report")

XBRL – US Federal Agencies • Joint Financial Management Improvement Program (JFMIP) 2001 report • JFMIP includes Department of Treasury, General Accounting Office, Office of Management and Budget, and the Office of Personnel Management. • “Core Financial System Requirements” states: ”To meet JFMIP interoperability requirements, the Core Financial system should: support emerging XML-based specifications for the exchange of financial data such as Extensible Business Reporting Language (XBRL). ” • http: //www. jfmip. gov/jfmip/.

Commercial Financial Information Supply Chain XBRL for G/L Journal Entry Reporting Processes Business Operations XBRL for Business Event Reporting XBRL for Financial Statements Internal Financial Reporting External Financial Reporting XBRL for Audit Schedules XBRL for Tax Filings Trading Partners Investment and Lending Analysis Financial Publishers and Data Aggregators Companies Participants XBRL for EDGAR Filings Management Accountants Auditors Software Vendors Regulators Investors

Government Financial Information Supply Chain XBRL for G/L Journal Entry Reporting Processes Business Operations XBRL for Business Event Reporting XBRL for Financial Statements Internal Financial Reporting External Financial Reporting XBRL for Audit Schedules XBRL for Tax Filings Trading Partners Investment and Lending Analysis Higher Echelons Organizations Participants XBRL for EDGAR Filings Management Accountants Auditors Software Vendors Public Policy Setting Organizations

Federal Generally Accepted Accounting Principles Hierarchy • Department of Agriculture • Department of Commerce • Department of Defense • Department of Education • Department of Energy • Department of Health and Human Services • Department of Housing and Urban Development • Department of the Interior • Department of Justice • Department of Labor • Department of State • Department of Transportation • Department of the Treasury • Department of Veterans Affairs Individual standards agreed to by the Director of OMB, the Comptroller General, and the Secretary of the Treasury • • • Agency for International Development Environmental Protection Agency Federal Emergency Management Agency General Services Administration National Aeronautics and Space Administration National Science Foundation Nuclear Regulatory Commission Office of Personnel Management Small Business Administration Social Security Administration Interpretations related to the SFFASs issued by OMB in accordance with the procedures outlined in OMB Circular A-134, Financial Accounting Principles and Standards. Requirements contained in OMB's Form and Content Bulletin in effect for the period covered by the financial statements. Accounting principles published by authoritative standard setting bodies and other authoritative sources (a) in the absence of other guidance in the first three parts of this hierarchy, and (b) if the use of such accounting principles improves the meaningfulness of the financial statements.

SFFAS Promulgation Process Treasury http: //www. treas. gov OMB http: //www. whitehouse. gov/omb Appoints GAO Federal Accounting Standards Advisory Board FASAB (9 Board Members) Appoints Draft Statements of Federal Financial Accounting Standard SFFAS http: //www. gao. gov Statements of Federal Financial Accounting Standards Amendments SFFAS 1 - Accounting for Selected Assets and Liabilities SFFAS 2 - Accounting for Direct Loans and Loan Guarantee SFFAS 18 SFFAS 3 - Accounting for Inventory and Related Property SFFAS 4 - Managerial Cost Accounting Concepts and Standards SFFAS 5 - Accounting for Liabilities of the Federal Government SFFAS 6 - Accounting for Property, Plant and Equipment SFFAS 11, 14 & 16 SFFAS 7 - Accounting for Revenue and Other Financing Sources SFFAS 13 SFFAS 8 - Supplementary Stewardship Reporting SFFAS 11, 14 & 16 SFFAS 9 - Deferral of Implementation Date for SFFAS 4 SFFAS 10 - Accounting for Internal Use Software SFFAS 15 - Management’s Discussion and Analysis SFFAS 17 - Accounting for Social Insurance http: //www. financenet. gov/fasab. htm Treasury SFFAS 12 http: //www. treas. gov Approves OMB http: //www. whitehouse. gov/omb GAO http: //www. gao. gov

Taxonomy Development and Resources Government Policy • • • GAP OMB Form and Content USSGL Crosswalk to OMB F&C USSGL TFM OMB Form and SFFAS/SFFAC Content ASSETS 1. Entity A. Intragovernmental 1. Fund Balance With Treasury 2. Investments 3. Accounts Receivable, Net 4. Other 5. Total Intragovernmental B. 1. Investments 2. Accounts Receivable, Net 4. Cash and Other Monetary Assets 5. Inventory and Related Property, Net 6. General Property, Plant and Equipment, Net 7. Other C. Total Entity Treasury USSGL Crosswalk to OMB Form and Content GLA Attributes 1340 1349 1610 X, Y, Z A, B, C X, Y, Z

Potential Financial Statement Submission Process Post close T/B Proprietary COA Mapping to US Standard General Ledger Post close T/B US Standard General Ledger Convert to Treasury Crosswalk elements USSGL PCTB & Crosswalk elements Federal Taxonomy Custom Taxonomy Consolidated Federal Financial Statements Aggregation and/or Consolidation Other consolidated Financial Statements Consolidated Federal Financial Statements Aggregation and/or Consolidation Other entities’ Financial Statements Instance Document Build Entity A Federal Financial Statements Blue = required tool

How will XBRL impact content based businesses? – – – Less data preparation Less data re-keying More direct communication among processes More emphasis on analytics Dashboards Expansion of non-financial information content Rapid transformation of products Semantic analysis Information agents Reduced data tailoring costs and revenues Reduced application tailoring costs and revenues Source: Liv Watson, Edgar Online

Why XBRL instead of our own Schemas? • Don’t reinvent the features of XBRL – – Information Producer Item types – financial parameters Predefined concepts (labels, references) Entities, periods, segments, scenarios Extensibility using XLink € 2. 5 m 9, 000 57% EPS Business Information that is • Financial in nature • Enhances standard definitions • Refers to multiple entities • Refers to multiple periods Information Consumer

XBRL uses XLink to represent all relationships between data elements <element id=“ast. cur”> Definition: more general <Label>Current Assets</Label> label <element id=“ast. inv”> <Label>Inventory</Label> Presentation: before reference <element id=“ast. fixed”> <P>A formal explanation of Inventory in the Accounting Literature</P>

XLink allows customization and explicit, modular changes to reusable material <element id=“ast. cur”> Definition: more general <Label> </Label> label <element id=“ast. inv”> <Label> </Label> Presentation: before <element id=“ast. fixed”> reference <P>A formal explanation of Inventory in the Accounting Literature</P>

Example: XBRL for Web Site Reporting Insider trades Significant events Company Site Custom Taxonomy US Site Taxonomy Element Schema and Definition Linkbase Calculation and Other Linkbases Restrictions on redefining links GAAP C&I v 2 Taxonomy Element Schema and Definition Linkbase Calculation and Other Linkbases imports Element Schema and Definition Linkbase Calculation and Other Linkbases

Present And Near Future Uses of XBRL • B 2 G - Regulatory Applications – Australian Prudential Regulatory Authority (2001) – US Federal Depository Institution Corp. (2002) – UK Inland Revenue (2003) • B 2 L – Business to Lenders – Bank of America / Moody’s – Credit Analysis (2003) – Deutsche Bank – same • B 2 M – Business to Markets – Traditional financial reporting (2002) – Business performance reporting (2003) • Internal applications

Questions!

Dr. Saeed Roohani Chair, Accounting Department Bryant College sroohani@bryant. edu Note: Pictures may not be current Neal J. Hannon, CMA Chair, Education Work Group, XBRL International nhannon@cox. net

- Slides: 67