Working Capital Management Accounts Receivables Accounts Payables Samantha

Working Capital Management Accounts Receivables & Accounts Payables Samantha Karandagoda

ACCOUNTS RECEIVABLES

Accounts Receivable • Refers to the Money that Still Has to be Collected from the Customers who Bought on Credit • Selling on Credit Helps to Increase Sales Volumes & Profits • Consider the Cost of Allowing Credit

Credit Policy • Firms Must have a Clearly Outlined Policy when Selling on Credit – What’s the Maximum Amount of $ or Currency Allowed in Credit – What’s the Duration to Pay – What are the Penalties

Credit Policy • • • Demand for Products Competitor’s Terms Risk of Irrecoverable Debts Cost of Finance Costs of Credit Control

Receivables Management • Assessing Creditworthiness • Settling Credit Limits • Involving Promptly & Collecting Overdue Debts • Monitoring the Credit System

Assessing Creditworthiness Bank Reference Trade Reference Competitors Published Information Credit Reference/Rating Agencies • Legal Information • Sales Data • • •

Setting Credit Limits • Limits are Twofold – Amount of Credit Available – Duration for which the Credit is Allowed • Ideally Firm Should have an Internal Policy • Customers Should be Well Informed

Debt Collection • • • Reminding Letter Telephone Call Withholding Supplies Debt Collectors Legal Action

Illustration • A Firm at the end of March has Following to be Collected from the Customers of each Month: – March: (100% of sales): $ 1, 200, 000 – Feb: (70% of sales): $ 700, 000 – Jan: (30% of sales): $270, 000 – Total: $2, 170, 000

: 31")

Illustration • Convert this to Receivables Days: – March: (100% of 31 Days): 31 Days – Feb: (70% of 28 Days): 20 Days – Jan: (30% of Days): 9 Days – Total: 60 Days

Illustration • Trying to Make it 50 Days • Collect More from March Sales • Jan Sales 9 Days + Feb Sales 20 Days = 29 Days • 50 – 29 = 11 • Therefore Collect March Sales Belonging to First 11 Days of March – $1, 200, 000 x (11/31) = 425, 806

Monitoring the Receivables Collection • Age Analysis – How many days before of sales paid up by the customer • Ratios – As Calculated in the Previous Lesson • Statistical Data

Accounts Receivables Calculations • Cost of Financing the Receivables • Finance Cost = Receivable Balance X Interest Rate • Receivable Balance = Sales x Receivable Days 365

Cost of Settlement Discount • Giving Discount Means a Loss in the Total Collection • However, avoids Losses Caused by the Interest Charges

Illustration • Sales: $20 Million • Receivables at Year End: $4 Million • Over Draft Interest Rate: 12% • Cash Discount of 2% is Proposed for Settlements within 10 Days

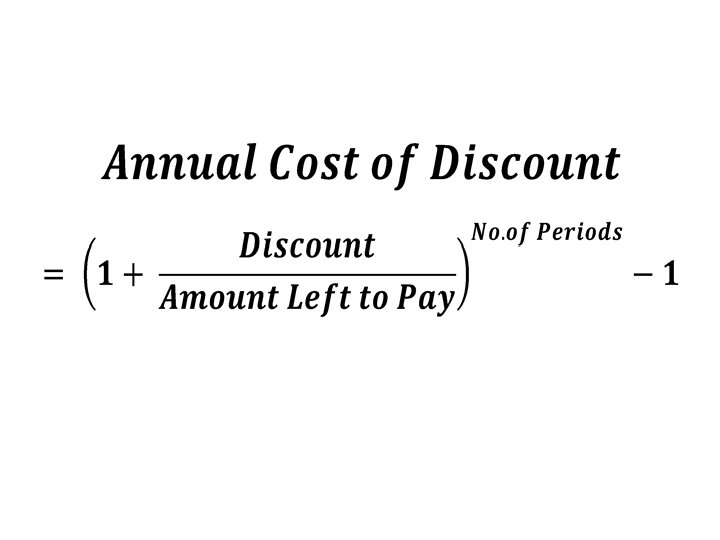

Illustration • Discount as a Percentage of the Amount Left to Pay: = 2/98 = 2. 04% • Receivables Days are Currently: = (4 / 20)x 365 = 73 • Shortening the Receivable Days from 73 Days to 10 Days is the Target (63 Days Down!) • 63 Days -> 5. 794 Periods Per Yr.

5. 794 -1 = 12. 41%")

Illustration • Cost of the Discount = (1+0. 0204)5. 794 -1 = 12. 41% But Cost of the OD Is: 12% Therefore, Borrowing from the Bank is Cheaper than Giving Discount to Collect Debt!

Factoring the Receivables • Selling Debts to a 3 rd Party at a Discount in Return for Prompt Cash • Services offered by Factor – Debt Collection & Administration – Credit Insurance • Useful for – Small Firms – Faster Growing Firms

Advantages • Saves Admin Cost • Reduced Need for Management Control • Useful for Small & Medium Businesses where a Credit Control Department is Not Feasible to Be Set Up

Disadvantages • More Costly than an Efficient Internal Credit Control Department • Using a Factor Indicates Lack of Liquidity -> Bad Reputation • Customers May not Wish to Deal with a Factor • Difficult to Reverse • Loss of Control on Credit Decisions

Invoice Discounting • A Method of Raising Finance Against the Security of Receivable without Using a Factoring Service • However Some Factoring Companies Carry Out this Service • Customer Doesn’t Know • Confidential

ACCOUNTS PAYABLES

Accounts Payables • Refers to the Payments to be Made to the Suppliers • Have to Be Paid Back on Time – Maintain Supplier Relationship – Avoid Loss of Reputation – Avoid Price Increases in the Future • Considered as a Free Source of Finance but there’s a Discount Foregone!

Settlement Discounts • When the Businesses Purchase on Credit, a Period is Given to Pay Back • However if the Payment is Made Earlier, the Supplier Might Give a Settlement Discount

Age Analysis of Payables • Similar to Receivables, We Can Analyse How much is Falling Due within the Next 30 days, 60 days & 90 days etc.

Question • Entity is Offering a Cash Discount of 2. 5% to the Customers if they Pay within 1 month. Usual Credit Period is 3 months. Bank Loan Rate 18% p. a.

Answer Discount as a Percentage of Amount to be Paid: 2. 5/97. 5 = 2. 56% Saving: 2 months (since payment comes in 1 month instead of 3 months) = 6 periods (2/12) Calculate the Annualized Cost of Discount (1+0. 0256)6 – 1 = 16. 38% Loan Rate is 18% Hence it’s worth to give the discount!

Question • Allow 1. 75% discount for payment within 3 weeks or full payment within 8 weeks? (assume a 50 week year)

Answer • Assume a $100 invoice • Discount: 100 x 1. 75% = $1. 75 • Amount Due After Discount: 100 – 1. 75 = 98. 25 • Effective interest cost of NOT taking the discount: 1. 75/98. 25 = 0. 0178 (~0. 018) • 5 Week Period • Means there are 10 periods/yr

10 – 1")

Answer • Equivalent Annual Rate for 10 Periods (1 + 0. 018)10 – 1 = 0. 195 • Rate is 19. 5%

Working Capital Management Accounts Receivables & Accounts Payables Samantha Karandagoda

- Slides: 33